Are markets celebrating too early?

- EXANTE LinkedIn Poll Results

- Markets in November

- Global market indices

- Commodity sector news

- Currencies

- Cryptocurrencies

- Fixed Income

- Global Macro Updates

- Key events in December

Last week we asked on LinkedIn, “Ahead of COP28 and discussions on the clean energy transition, what do you think will impact a new commodity supercycle most?”

With the surge in energy prices over the past two years, it is not surprising that 36% of respondents said “energy security fears” would have the most impact. Energy security is one part of the trilemma facing markets along with sustainability and affordability. Geopolitical fragmentation and the high cost of capital are also likely to impact the green transition. You can read more in our upcoming report, out next week, on Renewables and the New Commodity Superpowers.

Markets in November

November has been a generally positive month for markets. Equities surged and bond markets rallied. The S&P 500 is up about 9% in November and on track for its biggest monthly gain since July 2022. It has even approached “overbought” levels. Yields continued to fall as traders held tight to the belief that the Fed is on course to meet its inflation target and is thinking of when it can begin to loosen policy. Fed swaps priced in a quarter-point rate cut by May. With the gain in Treasury yields reversing, the dollar showing more signs of weakness, and the VIX, the market’s most closely watched fear gauge, close to post-pandemic lows, investors are celebrating.

The US economy grew faster than initially thought in the third quarter, to 5.2%. The growth pace, which was the quickest in nearly two years, is the latest sign of the country’s economic resilience despite high interest rates. US consumer confidence rose in November after three straight monthly declines, though households continued to anticipate a recession over the next year. The Conference Board said its consumer confidence index increased to 102.0 this month from a downwardly revised 99.1 in October. However, as noted by the Fed’s Beige book, US economic activity has slowed as consumers are still feeling the pinch and cutting back on discretionary spending. Continuing labour market tightness and rising business activity levels, with the S&P Global Flash Composite PMI remaining in expansionary territory coming in at 50.7, unchanged from October. The Flash Services PMI was up at 50.8 from October’s 50.6, a 4-month high. However, the Flash Manufacturing PMI returned to contractionary territory and hit a 3 month-low, coming in at 49.4, lower than October’s 50.0. Although inflation is on a path to see the highest drop in 71 years, the strength of the US economy may also help solidify the “higher for longer” case as the Fed will want to prevent the economy from overheating.

Stagnation in parts of the eurozone economy continued in November. Although eurozone headline inflation fell in November to 2.4%, there are still some possible headwinds for inflation including a rise in energy prices. Business activity appears to be slowing with the eurozone's HCOB flash Composite PMI in November remaining entrenched in contractionary territory despite rising to 47.1 from 46.5 in October. Manufacturing activity, which has contracted every month since July 2022, remained in contractionary territory in November with the HCOB Manufacturing PMI rising to 43.8 from 43.1.

Global Market Indices

US:

S&P 500 +8.61% MTD and +18.63% YTD

Nasdaq 100 +10.93% MTD and +46.11% YTD

Dow Jones Industrial Average +7.15% MTD and +6.85% YTD

NYSE Composite +7.0% MTD and +5.13% YTD

Europe:

Stoxx 600 +5.87% MTD and +8.05% YTD

DAX +9.16% MTD and +16.11% YTD

CAC 40 +5.55% MTD and +12.26% YTD

FTSE 100 +1.39% MTD and -0.38% YTD

IBEX 35 +11.59% MTD and +22.28% YTD

FTSE MIB +7.02% MTD and +25.23% YTD

Global:

MSCI World Index +8.71% MTD and +14.32% YTD

Hang Seng -0.70% MTD and -14.09% YTD

Mega cap stocks had a great November as investors flocked back into the super seven stocks on rising hopes that these interest sensitive stocks would benefit even further on expectations that the Fed will cut rates sooner rather than later. Alphabet, Amazon, Apple, Nvidia, Tesla, Meta Platforms, and Microsoft all up.

Energy stocks had a mixed and volatile month as investors weighed the risk of global oversupply in 2024 and potentially waning demand against rising geopolitical risks and threats of production cuts from OPEC+ countries. Phillips 66 and Energy Fuels are up, while Marathon Petroleum, Occidental Petroleum Corporation, BP, ExxonMobil, Chevron, Baker Hughes Company, Apa Corp (US), Shell, and Halliburton are all down on the month.

Materials and Mining stocks had a mixed November on a weaker dollar, but questions on oversupply of Lithium and low copper prices. Mining stocks Freeport-McMoRan, Nucor Corporation, and Newmont Mining are up, while Sibanye Stillwater is down. Materials stocks also had a very mixed month with Albemarle, CF Industries Holdings, and Yara International all down, while Mosaic and Celanese Corporation are up in November.

Commodities

Oil prices have fallen in November as the conflict in Gaza has not yet widened. Members of OPEC+ are due to hold a delayed policy meeting today where they are likely to focus on additional production cuts and quotas for African suppliers. Oil prices were hit in November by the larger-than-expected build-up in US crude inventories and concerns about global demand, particularly as China, the world’s largest oil importer, continues to see a slowdown in growth with its manufacturing activity contracting for a second straight month in November.

Gold prices climbed again in November, surpassing the $2,000 an ounce mark, boosted by hopes that the Federal Reserve would cut interest rates earlier in 2024 than previously expected. The biggest downside risk for gold now is that the drop in inflation starts to falter, meaning potential rate cuts get delayed.

Currencies

The dollar fell in November as bonds rallied. The US economy, although still very resilient, is expected to start to slow in Q4 thereby increasing the likelihood of the Fed either maintaining the current rate at its next meeting and likely a couple of meetings beyond. It was an extremely good month for Sterling as the BoE’s firm line on higher rates for longer seemed to be heard by market players. The GBP is +4.46% MTD and +4.94% YTD against the USD. The EUR +3.72% MTD and +2.49% YTD against the USD. With inflation falling in the Eurozone, the ECB appears to have reached its peak rate in its hiking cycle. According to Refinitiv data, markets are now pricing in a quarter-point decrease to the ECB’s deposit rate by April and an almost 50% chance is assigned for a cut as early as March, according to swaps tied to the central bank’s meeting dates.

Cryptocurrencies

Bitcoin +8.95% MTD and +127.70% YTD

Ethereum +11.85% MTD and +69.42% YTD

Bitcoin and Ethereum surged ahead in November. This was largely due to investor expectations that the SEC would soon approve a spot Bitcoin exchange-traded fund (ETF). Twelve applications for spot Bitcoin ETFs are awaiting approval from the SEC.

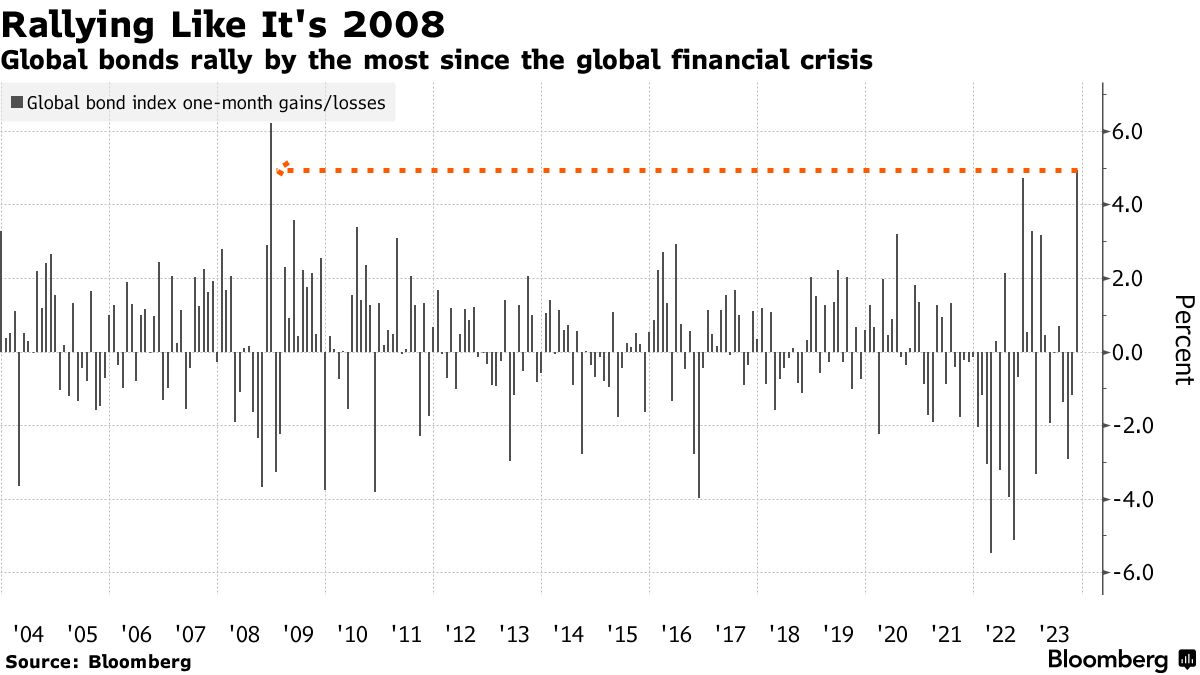

Fixed Income

US Treasuries 10 year yield to 4.27%.

German 10 year yield to 2.42%.

UK 10 year yield to 4.10%.

Bonds rallied in November on speculation the Fed is done with its aggressive hiking cycle. However, as noted by BlackRock, the path to higher long-term yields is unlikely to be straight in the next five years. Although headline inflation is likely to continue to fall, in the longer run problems remain. There have been structural shifts in the labour market, geo-fragmentations with geopolitical risk rising across the globe and perhaps permanently affecting supply chains, and markets have not yet felt the full impact of the “green” transition including the price impact it is anticipated to have on certain commodities. Yields will likely stay volatile as investors start to demand more term premium.

In Europe, there has been conflicting discussions as to whether the ECB is at peak rates and when it will seek to cut them as inflation continues to fall. However, core inflation is only expected to slow to 3.9% in the euro area, according to a Bloomberg survey, which may mean that the ECB may be slower to cut than markets currently anticipate.

In the UK the Bank of England has repeatedly stressed that interest rates would not change any time soon.

Note: As of 5:00 pm EST 29 November 2023

Global macro updates

A mixed growth picture. The OECD latest economic outlook, released on Wednesday 29 November, has forecast an anaemic growth year ahead for many developed economies as growing global geopolitical risks and rising tensions, digitalisation and climate policy adjustments all disrupt these economies. It forecasts that the UK will continue to fall behind its peers and is on course for sluggish growth alongside sticky inflation in 2024 and 2025. GDP growth is projected to pick up slightly from 0.5% in 2023 to 0.7%t in 2024 and 1.2% in 2025. Germany is forecast to only post growth of 0.6% in 2024. The US, by contrast, is on track for growth of 1.5% in 2024 and 1.7% in 2025.

China’s worrying slowdown? China’s official manufacturing purchasing managers’ index came in at 49.4 this month, slightly below a reading of 49.5 in October. The non-manufacturing PMI came in at 50.2, down from October’s 50.6. It is still in positive territory but still the lowest reading since the height of China’s Covid closure last December. The services industry activity component of non-manufacturing PMI registered a contraction at 49.3 points compared with a reading of 50.1 the previous month. “Survey results show that more than 60% of manufacturing companies reported insufficient market demand. Insufficient market demand is still the primary difficulty affecting the current recovery and development of the manufacturing industry,” Zhao Qinghe, a senior statistician at the Service Industry Survey Center of the National Bureau of Statistics, said in a statement. While China’s Q3 annual GDP growth was 4.9% and quarter on quarter GDP was 1.3% in Q3, the country may not be out of the woods yet. The property market is still in the doldrums and, as noted by Bloomberg news, stocks in mainland China did not experience the broad November rally as happened across global markets, with the market extending its run of losses owing to persistent investor concerns about the economic recovery. Industrial profits increased only 2.7% year-on-year, according to data published by the National Bureau of Statistics. The pace eased significantly from September’s 11.9% gain and August’s 17.2% jump.

Key events in December

30 Nov-12 December 2023 Conference of the Parties to the UN Framework Convention on Climate Change (COP28). COP28 will take place in Dubai, UAE. As a result of disappointing progress at COP27, members will be under pressure to make significant progress in securing commitments to reducing carbon emissions.

12-13 December 2023 US Federal Reserve Monetary Policy meeting. The Fed has made it clear in a number of statements since its November meeting it is likely to maintain the higher for longer stance for the foreseeable future. Growth has remained resilient, coming in at 5.2% in Q3 and the labour market, although loosening, is still relatively tight. The Fed has kept its policy rate unchanged in the 5.25%-5.50% range since July. Fed Chair Jerome Powell has stated that he is not yet confident policy is restrictive enough. The main concern for the Fed will be the pace of core inflation and how sticky it is. Market focus is now on the US personal consumption expenditure data due later today, the Fed's preferred inflation gauge and Fed Chair Jerome Powell’s speech on Friday.

14 December 2023 ECB meeting and monetary policy decision. Inflation in the eurozone was lower than expected in November, dropping to 2.4% from 2.9% in October 2023, and a fraction of the 10.6% rate a year ago, as price pressures continued to ease faster than forecast across the eurozone. This has raised hopes that interest rates could be cut in early 2024.

14 December 2023 Bank of England Monetary Policy Summary and minutes. Various members of the Monetary Policy Committee including Megan Greene, Jonathan Haskell, and BoE Governor Andrew Bailey have stated over the past month that rates will need to stay higher for longer. Although inflation has dropped to 4.6% and there are signs of weakening wage growth, there are still concerns about services wage growth adding inflationary pressures.

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

本文提供給您僅供資訊參考之用,不應被視為認購或銷售此處提及任何投資或相關服務的優惠招攬或遊說。金融商品交易涉及重大損失風險,可能不適合所有投資者。過往績效不代表未來表現。

由專業人士建立。為專業人士打造。