Will there be fireworks at the Senate?

What to look out for today

Companies reporting on Tuesday, 21 April: 3M, Capital One Financial, Equifax, GE Aerospace, Halliburton, Northrop Grumman, Quest Diagnostics, RTX, United Airlines, UnitedHealth Group

Key data to move markets today

EU: German Current Situation and Economic Sentiment surveys and Eurozone Economic Sentiment survey

UK: Average Earnings, Claimant Count Change, Claimant Count Rate, Employment Change and ILO Unemployment Rate

US: ADP Employment Change 4-week Average, Retail Sales, Retail Sales Control Group and Pending Home Sales

JAPAN: Adjusted Merchandise Trade Balance, Imports, Exports and Merchandise Trade Balance Total

Global Macro Updates

Preview: Kevin Warsh confirmation hearing. The US Senate Banking Committee is scheduled to hold a confirmation hearing for Fed Chair nominee Kevin Warsh today at 10:00 am EDT. The market anticipates a comprehensive discussion of Warsh’s policy perspectives and their development over time, as well as his views on Fed’s independence, especially given the ongoing dispute between the US President and current Fed Chair Jerome Powell.

Warsh has consistently advocated for lower interest rates, contending that inflation has been aggravated by policy missteps and mission creep within the Fed. He highlighted this in his public remarks at the G30 lecture at the IMF Spring Meetings of last year. He has called for a ‘regime change’ to enhance the Fed’s credibility and emphasised the necessity for a renewed Treasury-Fed accord, a point he reiterated during a CNBC interview. Furthermore, Warsh supports a more forward-looking monetary policy that accounts for ongoing productivity gains from AI, reinforcing his preference for a lower-rate outlook. He has also described the Fed’s balance sheet as ‘bloated’ due to trillions of dollars in assets. It is important to note that Treasury Secretary Bessent has indicated that reducing these holdings may require significant time.

Regardless of Warsh’s performance at today’s hearing, the committee is not expected to advance his nomination to the full Senate due to opposition from Senator Thom Tillis. Tillis, who is set to depart the Senate in January 2027, has described Warsh as the ‘perfect candidate’, but has stated he will not vote to confirm any Fed nominees until the Trump administration ends its investigation into Fed Chair Powell. If Tillis votes against and all Democratic members do likewise, the committee would likely deadlock at 12-12. Some Republican legislators have expressed the desire for the Powell investigation to be resolved in order to proceed with Warsh’s seating, according to reporting by Politico.

Expectations for Warsh’s confirmation prior to the expiration of Powell’s term as chair on 15 May remain subdued, with prediction markets estimating the probability in a range of 30% to 40%. Fed Chair Powell has stated that he would continue serving as Chairman until a successor is confirmed, following legal requirements and established precedent, as noted during the 18 March FOMC press conference. Powell’s term as a Fed governor does not conclude until 2028, although it has historically been uncommon for replaced Fed Chairs to remain in their positions. Last week, President Trump announced that the Fed investigation would persist and threatened to dismiss Powell if he does not vacate the position ‘on time.’

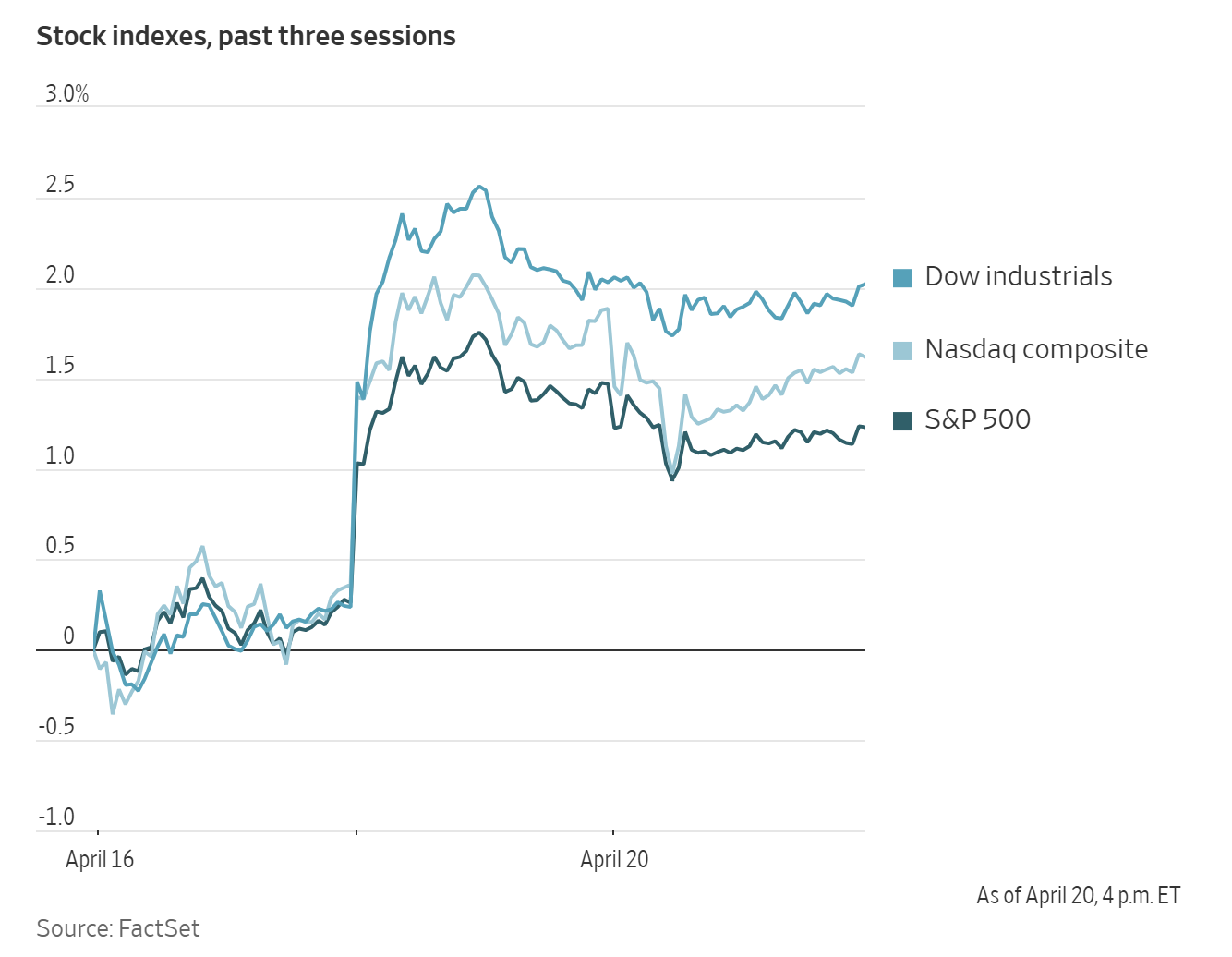

US Stock Indices

Dow Jones Industrial Average -0.01%

Nasdaq 100 -0.31%

S&P 500 -0.24%, with 5 of the 11 sectors of the S&P 500 down

Equity markets retreated from record highs, as the S&P 500 paused its five-day rally amid notable declines in several leading technology companies.

The Nasdaq Composite decreased -0.26%. The S&P 500 dropped -0.24%, while the Dow Jones Industrial Average slipped by 4.87 points, a decline of -0.01%. These losses remained relatively modest compared to the more pronounced selloffs observed earlier during the conflict.

In contrast, the Russell 2000 index, which tracks smaller companies, advanced +0.58%, marking its third consecutive record close at 2,792.96, and its strongest performance over a 14-session period since 2020.

In corporate news, shares of AST SpaceMobile declined following an incident in which Blue Origin’s flagship New Glenn rocket failed to deliver a payload for the Texas-based satellite networking company to its designated orbit.

Caesars Entertainment has prolonged its exclusive negotiations regarding an $18 billion acquisition by Tilman Fertitta, as further details concerning the potential transaction are disclosed, according to Bloomberg news.

Spirit Aviation Holdings is reportedly considering offering the US government an equity stake in the discount airline as part of its efforts to prevent possible liquidation, according to sources familiar with the situation, as reported by Bloomberg news.

S&P 500 Best performing sector

Materials +0.56%, with Steel Dynamics +4.51%, LyondellBasell Industries +3.49% and Dow +3.29%

S&P 500 Worst performing sector

Communication Services -1.41%, with Meta Platforms -2.56%, Netflix -2.55% and Alphabet -1.18%

Mega Caps

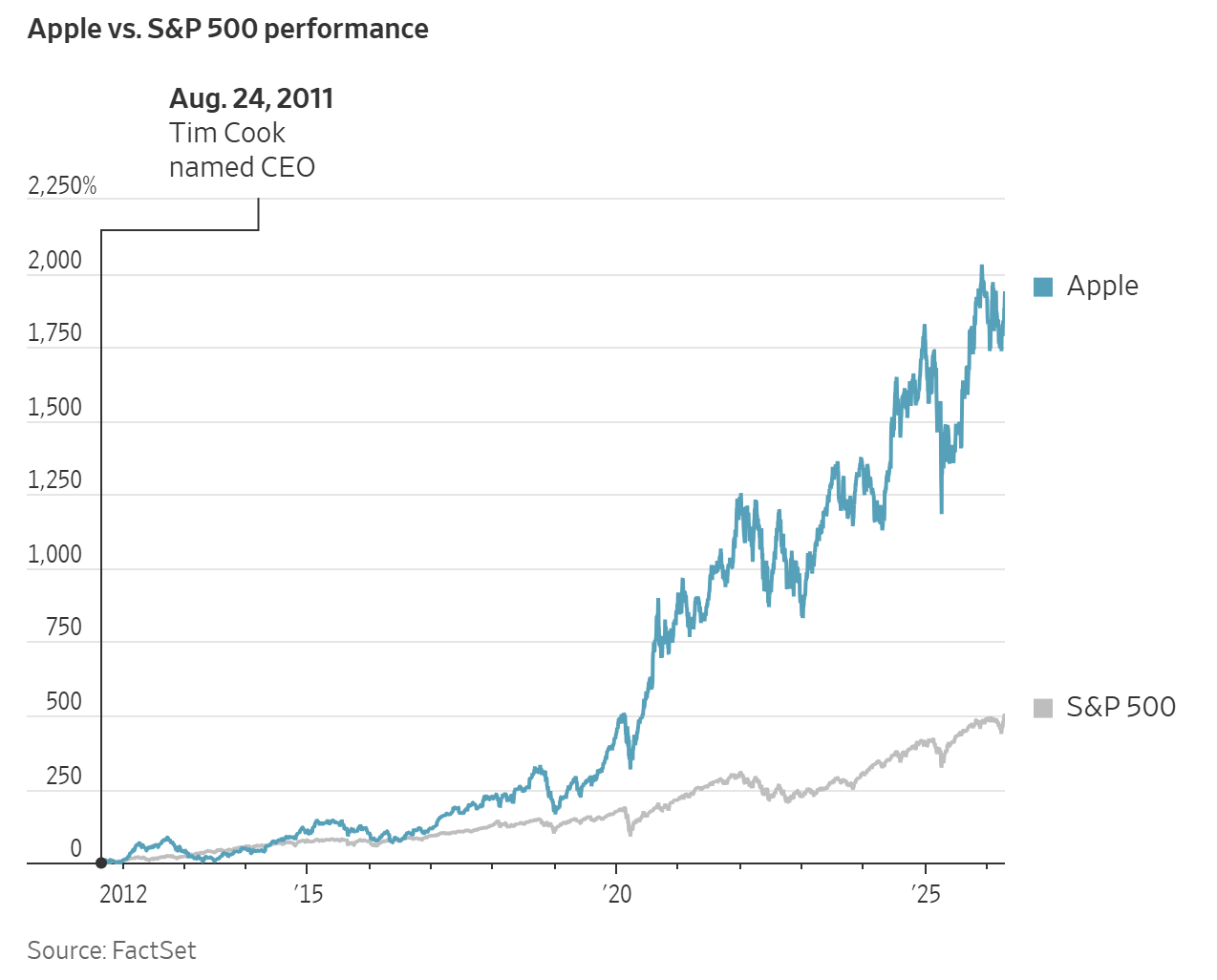

Alphabet -1.18%, Amazon -0.91%, Apple +1.04%, Meta Platforms -2.56%, Microsoft -1.12%, Nvidia +0.19% and Tesla -2.03%

Apple appoints new CEO as Tim Cook steps down. John Ternus will lead Apple as it strives to reignite its culture of innovation and pursue a hardware-focussed strategy in the era of artificial intelligence. Ternus, Apple’s head of its hardware division, follows in the footsteps of Steve Jobs, who pioneered the world’s most successful consumer product, and Tim Cook, who transformed Apple into the world’s most valuable company through operational excellence and exceptional profitability.

Ternus’s appointment will take effect on 1 September, at which point Cook will succeed longtime chair Art Levinson as Executive Chairman.

Cook leaves a legacy of extraordinary value creation, as he skillfully navigated Apple through significant geopolitical and economic challenges, including the imposition of tariffs by US President Trump and the disruptions caused by the COVID-19 pandemic. Under his leadership, Apple’s market capitalisation increased by nearly $3.7 trillion, reaching approximately $4 trillion, an achievement surpassed only by Nvidia’s Jensen Huang in terms of total value created by an American CEO.

A key challenge for Ternus will be to sustain Apple’s industry leadership as competitors invest heavily in advanced computing infrastructure and the integration of AI technologies into their products and daily operations.

Information Technology

Best performer: Hewlett Packard Enterprise +5.18%

Worst performer: Intel -4.09%

Materials and Mining

Best performer: Steel Dynamics +4.51%

Worst performer: International Flavors & Fragrances -1.90%

Corporate Earnings Reports

Posted on Monday, 20 April

Steel Dynamics quarterly revenue +19.1% to $5.205 bn vs $5.024 bn estimate

EPS at $2.78 vs $2.78 estimate

Mark D. Millett, Chairman and CEO, said, “The teams executed well, delivering a strong first quarter 2026 performance across all of our platforms, with operating income increasing $228 million, or 73 percent. The improvement in earnings was driven by record steel shipments combined with higher steel prices. Our three-year after-tax return-on-invested capital of 13 percent is a testament to our ongoing high-return capital allocation execution. We are growing, returning capital to shareholders, and maintaining strong returns with best-in-class performance compared to domestic manufacturers.” — see report.

European Stock Indices

CAC 40 -1.12%

DAX -1.15%

FTSE 100 -0.55%

Commodities

Gold spot -0.18% to $4,819.62 an ounce

Silver spot -1.45% to $79.62 an ounce

West Texas Intermediate +3.06% to $88.19 a barrel

Brent crude +2.47% to $94.26 a barrel

On Monday, gold prices declined to their lowest level in a week before experiencing a modest rebound.

Spot gold ended the day -0.18% to $4,819.62 per ounce, reaching its lowest point since 13 April.

Spot silver declined -1.45% to $79.62 per ounce.

Oil prices advanced on Monday as market participants awaited further clarity regarding the direction of diplomatic negotiations between the United States and Iran.

Brent crude futures increased by $2.27, or +2.47%, to $94.26 per barrel. US WTI crude futures for May rose $2.62, or +3.06%, to $88.19 per barrel. The May WTI contract is set to expire today, with June futures ending trading at $87.42 per barrel.

Investors are closely monitoring ongoing discussions, focusing on whether this week's talks will lead to an extension of the current ceasefire or a comprehensive agreement. Nevertheless, the risk of renewed conflict and potential disruptions to oil flows persists.

A US delegation led by Vice-president JD Vance is travelling to Pakistan for discussions with Iran as the ceasefire deadline approaches. According to a senior Iranian official cited by Reuters, Tehran is positively considering participation in peace talks with the US, though no final decision has been reached. Iranian Foreign Minister Abbas Araghchi informed his Pakistani counterpart, Ishaq Dar, during a Monday phone call that Iran is evaluating all aspects before determining its next steps.

The Iranian Foreign Ministry expressed gratitude for Pakistan's mediation, but highlighted US ‘provocative actions,’ ongoing ceasefire violations, ‘threats and aggression against Iranian commercial ships’ and inconsistent US rhetoric as major obstacles to diplomatic progress. Additionally, a Tehran-based diplomat involved in the negotiations stated that the Iranian delegation, led by Mohamad Ghalibaf and Araghchi, will travel to Islamabad on Tuesday only if Vice-President Vance is present.

President Donald Trump, in a series of posts on Truth Social, asserted that any Iran deal negotiated under his administration would be far better than the JCPOA. He dismissed media reports suggesting he is under pressure to reach an agreement and emphasised that he will not allow Democrats to hasten him into an unfavourable deal. Trump further claimed that the US is decisively winning the conflict, referencing the destruction of Iran's naval and air defences, a de facto regime change, and a blockade imposing costs of $500 million per day on Iran, which will remain in effect until an agreement is reached.

Elsewhere, Iraq reopened the Rabia border crossing with Syria for the first time in over a decade to expedite overland exports of fuel oil, as Gulf shipping remains disrupted. State oil marketer SOMO has awarded contracts to transport approximately 650,000 metric tons of fuel oil per month from April through June via Syria. Most convoys are currently backed up at al-Waleed in western Iraq, previously the only functioning overland route. Historically, Iraq exported the bulk of its fuel oil through the Khor al-Zubair terminal in the Gulf.

The Trump administration extended its waiver for sales of sanctioned Russian crude through 16 May. US oil exports via the Panama Canal have reached their highest levels since July 2022, as shippers reroute around disruptions in the Strait of Hormuz.

The head of independent oil trading house Gunvor, CEO Gary Pedersen, told the Financial Times that seasonally softer demand ahead of summer, combined with persistent turbulence in the Middle East, may continue to drive sharp swings in oil prices for months. He described the market environment as volatile, attributing recent futures fluctuations in part to President Trump's political messaging. Pedersen noted that physical crude supplies remain exceptionally tight, as buyers actively seek alternatives to Middle Eastern barrels. He also highlighted an unusually large number of empty supertankers currently sailing from Asia to the US via the Cape of Good Hope to load US crude.

According to shipping data, crude oil loadings from Saudi Arabia's Yanbu port declined by 17% to approximately 3.5 million barrels per day during the week beginning 13 April.

Note: As of 4 pm EDT 20 April 2026

Currencies

EUR +0.18% to $1.1783

GBP +0.07% to $1.3523

Bitcoin -1.96% to $75,978.38

Ethereum -4.44% to $2,322.30

On Tuesday, the dollar came under pressure as investors prepared to shift toward riskier currencies, anticipating the possibility of a US - Iran agreement that could restore Gulf shipping routes.

The euro advanced to $1.1745, an increase of +0.18%, while sterling traded higher at $1.3523, up +0.07%.

The dollar index declined by -0.18% to 98.05.

The yen weakened -0.04% to ¥158.68 per dollar, remaining close to the pivotal ¥160 mark, which market participants consider critical for potential intervention.

The BoJ is expected to refrain from raising interest rates next week, according to five sources familiar with its deliberations, as reported by Reuters. This cautious stance reflects the uncertainty surrounding a potential resolution in the Middle East, which continues to cloud the country's economic and inflation outlook.

Fixed Income

US 10-year Bond +0.3 basis points to 4.254%

German 10-year Bund +2.1 basis points to 2.985%

UK 10-year gilt +9.0 basis points to 4.776%

US Treasuries remained largely unchanged on Monday, as bond investors appeared to disregard the recent turbulence in the Middle East that heightened concerns about the fragile ceasefire between Washington and Tehran. Instead, market participants focused their attention on the upcoming negotiations between the two parties.

Treasury movements were modest amid subdued trading volumes, as investors refrained from making significant directional bets.

During afternoon trading, the 10-year yield edged up +0.3 bps to 4.251%, while the 30-year yield declined -2.9 bps to 4.883%.

On the shorter end of the curve, the two-year yield, sensitive to interest-rate expectations, rose +1.3 bps to 3.725%.

Bond market participants will be closely monitoring today's US Senate Banking Committee hearing regarding Kevin Warsh's nomination as Fed Chair. The proceedings may prove contentious, as a prominent Republican and Senate Democrats have pledged to block his confirmation unless the White House terminates its criminal investigation of current Fed Chair Jerome Powell.

According to CME Group's FedWatch Tool, Fed funds futures traders are pricing in 14.5 bps of rate cuts in 2026, higher than the 8.6 bps priced in a week ago. Fed funds futures traders are now pricing in a 0.0% probability of a 25 bps rate hike at the 29 April FOMC meeting, lower than last week’s 1.0% probability.

Eurozone bond yields climbed on Monday, reflecting heightened apprehension that the ceasefire between Washington and Tehran may not hold. Nonetheless, borrowing costs remained significantly below the late-March highs established prior to the ceasefire announcement.

Germany’s 10-year bond yield increased +2.1 bps to 2.985%, while rate-sensitive two-year yields rose +5.5 bps to 2.465%.

Money markets indicate a slight probability of an ECB rate hike later this month. However, a 25 bps increase is considered likely by June, and markets are nearly fully pricing in two such hikes by year-end.

Italian 10-year BTP yields rose +2.1 bps to 3.715%, maintaining the spread over Bunds at 73.0 bps.

French 10-year OATs lagged behind their Italian counterparts, with yields rising +3.1 bps during the day to 3.610%.

Note: As of 4 pm EDT 20 April 2026

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

本文提供給您僅供資訊參考之用,不應被視為認購或銷售此處提及任何投資或相關服務的優惠招攬或遊說。金融商品交易涉及重大損失風險,可能不適合所有投資者。過往績效不代表未來表現。

由專業人士建立。為專業人士打造。