What will happen to the US dollar?

Global Macro Updates

The Dollar at an inflection point: petrodollar tailwinds and fiscal headwinds. The US dollar finds itself navigating a rare confluence of forces in April 2026, one pulling it higher through an energy-driven revival of petrodollar mechanics, and another pressing it lower through a structural deterioration in the safe-haven premium that has long underpinned Treasury demand. The net trajectory, while temporarily supported by geopolitical developments, points toward a more fragile reserve currency standing over the medium term.

The US naval blockade of the Strait of Hormuz, enacted this week, has materially altered global oil supply dynamics and, in turn, provided the dollar with a near-term boost consistent with its petrodollar heritage. With Iran's roughly 1.7 million barrels per day (bpd) of crude exports under direct interdiction threat, and the strait effectively closed to Iranian commerce, global energy prices have soared. The resulting demand shock for US dollar-denominated energy transactions reinforces the petrodollar system as does the US security response: when global oil prices rise and supply disruptions force importers to scramble for alternative sources, the need for dollars intensifies across emerging and developed markets alike.

As the US emerges as the world's dominant exporter of both crude oil and liquefied natural gas, the geopolitical leverage inherent in that position translates, at least in the near term, into structural dollar demand. Nations scrambling to secure energy supplies are, by definition, seeking dollars to do so, a dynamic that temporarily reinforces the currency's reserve-status mechanics.

Yet this near-term energy-driven dollar strength sits uncomfortably atop a deepening structural fissure that the IMF has now formally identified. In its April 2026 Fiscal Monitor, the Fund warned that the escalating scale of US Treasury issuance is actively compressing the safety premium that Treasuries have historically commanded, an erosion that is pushing up borrowing costs globally. The spread between AAA-rated corporate bonds and Treasury securities, once a clear expression of the US government's unrivalled creditworthiness, has narrowed from 55 bps in early 2019 to approximately 35 bps, a quantitative signal that the market is gradually re-rating the risk profile of US sovereign debt. The IMF noted that the US budget deficit has averaged 6% of GDP over the past three years and is expected to remain at that level for the coming decade, a historically anomalous fiscal trajectory that is fundamentally inconsistent with the discipline typically associated with reserve currency issuers.

The implications for the dollar extend well beyond the bond market. As the safety premium on Treasuries erodes, the dollar's role as the world's preferred reserve asset, a status long reinforced by the unmatched liquidity and security of US government securities, faces a slow but meaningful challenge. The IMF's Global Financial Stability Report further cautioned that structural shifts in sovereign debt markets, including the growing role of leveraged non-bank intermediaries absorbing Treasury issuance, are amplifying vulnerability to repricing episodes.

The dollar's trajectory is therefore best understood as bifurcated. In the near term, the petrodollar dynamic provides genuine and observable support, rooted in the mechanical reality that energy-importing nations must acquire dollars to pay for US and US-priced energy exports. This is not merely a sentiment-driven safe-haven flow, but a structural demand impulse tied to the physical economics of the energy trade. For as long as the Hormuz blockade remains in place and US export volumes continue their record ascent, the dollar can reasonably be expected to remain elevated relative to the currencies of major energy importers.

However, the medium-term outlook is materially less constructive. Goldman Sachs has characterised its 2026 dollar view as one of differentiated decline, projecting a gradual weakening as the structural advantage of US growth narrows and global capital reallocates more broadly. Franklin Templeton's Institute has framed dollar weakness as one of its three macro conviction themes for 2026, viewing a softening greenback as a tailwind for emerging debt and equity markets in particular.

The risk is that the petrodollar relief rally, while real, delays rather than reverses this structural adjustment. The same energy-driven inflation that bolsters short-term dollar demand also constrains the Fed's ability to cut rates aggressively, a dynamic that, while supportive for yields, compounds the stagflationary risk profile that weighs on long-duration Treasuries and, ultimately, on the dollar's appeal as a reserve asset. The dollar might have ridden the wave for now - but the tide beneath it is shifting.

Corporate Earnings Calendar

Thursday: Abbott Laboratories, Netflix, Pepsico, Prologis, Taiwan Semiconductor Manufacturing

Friday: Fifth Third Bancorp, State Street, Truist Financial

Monday: Steel Dynamics

Tuesday: 3M, Capital One Financial, Equifax, GE Aerospace, Halliburton, Northrop Grumman, Quest Diagnostics, RTX, United Airlines, UnitedHealth Group

Wednesday: AT&T, Boeing, Crown Castle, GE Vernova, IBM, Lam Research, Moody’s, Philip Morris International, ServiceNow, Southwest Airlines, Teledyne Technologies, Tesla, Texas Instruments

Global market indices

US Stock Indices Price Performance

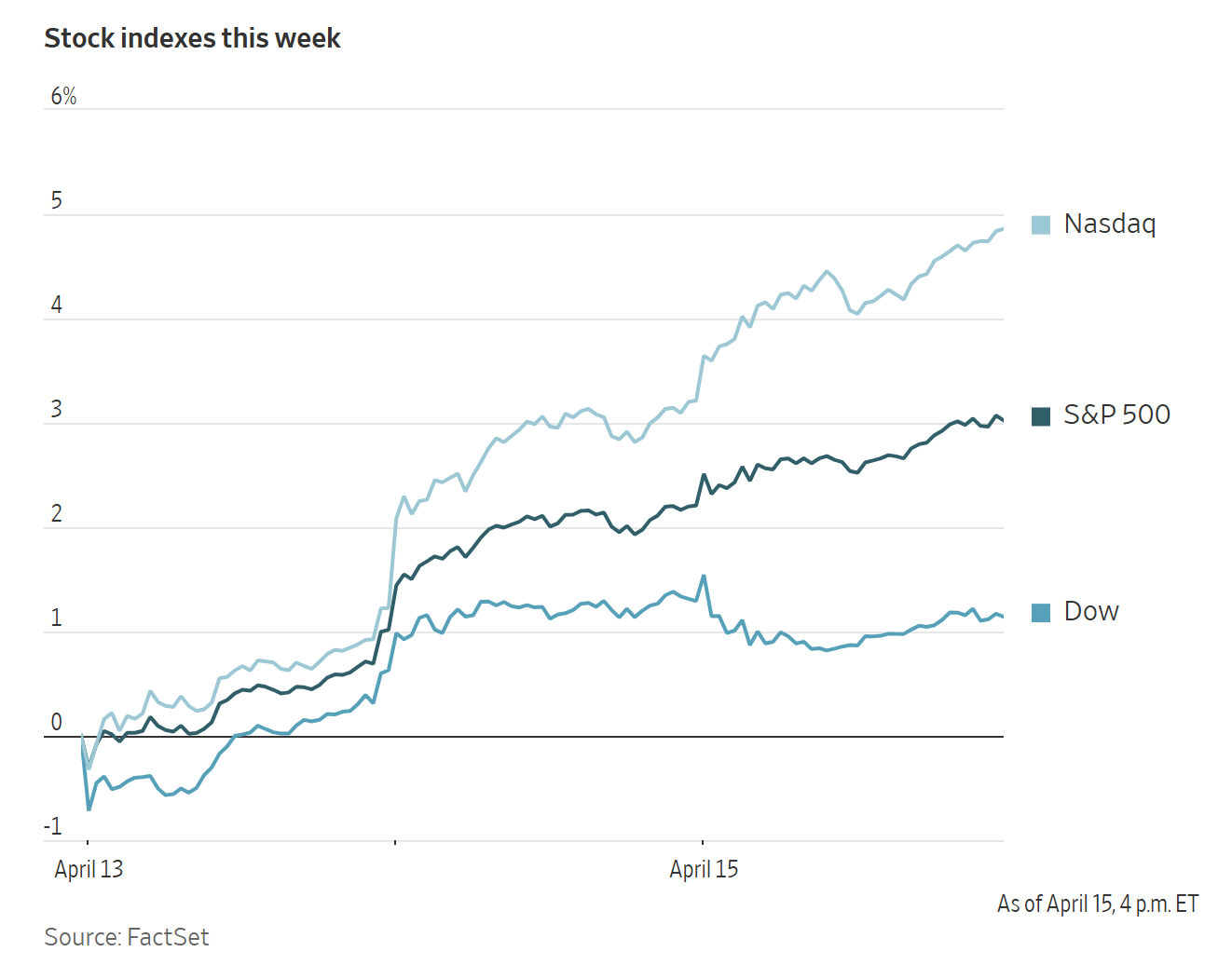

Nasdaq 100 +10.38% MTD and +3.78% YTD

Dow Jones Industrial Average +4.74% MTD and +0.98% YTD

NYSE +3.92% MTD and +4.32% YTD

S&P 500 +7.57% MTD and +2.59% YTD

The S&P 500 is +3.54% over the past seven days, with 9 of the 11 sectors up MTD. The Equally Weighted version of the S&P 500 is +0.85% over this past week and +4.23% YTD.

The S&P 500 Communication Services is the leading sector so far this month, +12.86% MTD and +4.85% YTD, while Energy is the weakest sector at -9.33% MTD and +24.44% YTD.

Over the past seven days, Consumer Discretionary outperformed within the S&P 500 at +8.00%, followed by Information Technology and Communication Services at +6.77% and +5.77%, respectively. Conversely, Energy underperformed at -4.02%, followed by Consumer Staples and Utilities at -2.23% and -1.54%, respectively.

The equal-weight version of the S&P 500 was +0.01% on Wednesday, underperforming its cap-weighted counterpart by 0.79 percentage points.

On Wednesday, the Dow Jones Industrial Average declined -0.15%, or 72.27, to close at 48,463.72. The S&P 500 advanced +0.80% to 7,022.95, a new record. The Nasdaq Composite posted a gain of +1.59% to 24,016.02, also a record high. Over the past seven days, the S&P 500 is +3.54%, the Dow Jones +1.31% and the Nasdaq Composite +6.10%.

In corporate news, Allbirds saw its share price surge 6x following the announcement that it had secured $50 million in financing. The company stated its intention to pivot toward AI compute infrastructure, with the long-term goal of becoming a fully integrated GPU-as-a-Service (GPUaaS) and AI-native cloud solutions provider.

Hermès, the manufacturer of Birkin bags, reported a slowdown in sales as the ongoing conflict in Iran dampened demand. Similarly, Kering, owner of the Gucci brand, disclosed a decline in sales. These updates followed earlier indications of industry weakness from LVMH, considered a bellwether for the luxury sector.

Snapchat announced plans to reduce its global workforce by approximately 16%.

Broadcom revealed an expansion of its partnership with Meta Platforms, agreeing to supply the Facebook parent company with additional custom artificial intelligence chips.

LIV Golf is reportedly on the verge of losing financial backing from the Saudi investment fund.

Mega caps: The Magnificent Seven had a positive performance over the past week. Over the last seven days, Tesla +14.19%, Amazon +12.32%, Microsoft +9.85%, Meta Platforms +9.66%, Nvidia +9.22%, Alphabet +6.24% and Apple +2.91%.

Energy stocks had a negative performance this week. The Energy sector itself was -9.33%. WTI and Brent prices are -5.10% and -1.31%, respectively, over the past week. Over the last seven days, Energy Fuels +13.13%, while BP -0.11%, Halliburton -0.69%, Shell -1.62%, Marathon Petroleum -3.86%, Phillips 66 -3.90%, Chevron -4.14%, ExxonMobil -4.62%, Baker Hughes -4.89%, ConocoPhillips -5.03%, APA -5.55% and Occidental Petroleum -6.59%.

Materials and Mining stocks had a mixed performance this week, with the Materials sector itself -0.67%. Over the past seven days, Freeport-McMoRan +5.53%, Albemarle +4.47%, Nucor +4.08%, Yara International +2.61%, Sibanye Stillwater +2.37% and Celanese Corporation +1.54%, while CF Industries -4.24%, Newmont Corporation -4.33% and Mosaic -10.86%.

European Stock Indices Price Performance

Stoxx 600 +5.85% MTD and +4.24% YTD

DAX +6.11% MTD and -1.73% YTD

CAC 40 +5.85% MTD and +1.53% YTD

IBEX 35 +6.66% MTD and +5.07% YTD

FTSE MIB +8.68% MTD and +7.14% YTD

FTSE 100 +3.76% MTD and +6.33% YTD

This week, the pan-European Stoxx Europe 600 index is up +0.61%. It declined -0.43% on Wednesday, closing at 617.27.

So far this month in the STOXX Europe 600, Banks is the leading sector +11.79% MTD and +3.84% YTD, while Oil & Gas is the weakest at -2.65% MTD and +32.31% YTD.

Over the past seven days, Financial Services outperformed within the STOXX Europe 600, at +3.38%, followed by Banks and Technology at +2.52% and +1.92%, respectively. Conversely, Personal and Household Goods underperformed at -2.76%, followed by Telecom and Travel & Leisure at -2.72% and -1.01%, respectively.

Germany's DAX index was up +0.09% on Wednesday, closing at 24,066.70. It declined by -0.06% over the past seven days. France's CAC 40 index was down -0.64% Wednesday, closing at 8,274.57. It was +0.13% over the past week.

The UK's FTSE 100 index was down -0.46% over the past seven days to 10,559.58. It was -0.47% on Wednesday.

The Personal & Household Goods sector emerged as the underperformer, due to weakness in the Luxury segment. Q1 earnings reports confirmed disruptions stemming from the Middle East and a decline in tourism flows. Both Hermes and Kering experienced significant sell-offs following Q1 sales figures that fell short of expectations, particularly at Kering's Gucci. These results heightened concerns regarding stalled high-end demand and delayed brand recovery, raising uncertainty about the pace of Kering's turnaround ahead of its upcoming Capital Markets Day.

Banks also lagged, despite broadly resilient macroeconomic commentary from US peers. BBVA and Santander declined after updates on Minimum Requirement for Own Funds and Eligible Liabilities (MREL) requirements from the Bank of Spain. The ongoing UniCredit and Commerzbank M&A saga stalled over valuation differences, while separately, UniCredit appears poised to withdraw its appeal regarding the golden power intervention on its Banco BPM bid.

Construction & Materials and Industrial Goods & Services also declined. Strabag shares fell following an accelerated share placement, which increased the free float but negatively impacted performance for the day. Sentiment around real estate activity and input costs remains cautious, though UK housebuilder Barratt Redrow was supported by improved reservation trends despite ongoing macroeconomic challenges. Travel & Leisure edged lower as the sector continued to face uncertainty regarding fuel costs and volatile demand.

Health Care was the strongest performer Wednesday, driven by momentum in pharmaceuticals and ongoing clinical and news flow catalysts. Novo Nordisk rallied after SB1 Markets initiated coverage with a buy rating, while Cosmo Pharmaceuticals advanced on positive Phase III data for its hair loss treatment. Smaller-cap biotech companies also outperformed, including Isofol Medical, following German regulatory approval for a refined Phase Ib/II study design, and Evotec, which advanced after announcing management restructuring.

Financial Services traded higher, driven by exchanges and retail platforms rather than traditional asset managers. Deutsche Börse received a rating upgrade, and several companies reached new highs, reflecting increased trading activity, highlighted by record revenues from Wall Street banks’ trading desks in Q1. In consumer finance, Hypoport stood out due to strong mortgage volumes. Additionally, UBS Group CEO Ermotti is reportedly expected to remain in his role well into the second half of 2027 as no internal successor has emerged.

Technology remained well-supported by AI-driven CapEx, with ASML delivering a Q1 beat and raise, underscoring structural demand for semiconductor equipment. Aixtron surged on robust orders and an upgraded outlook, signalling improved visibility in optoelectronics. Basic Resources benefitted from favourable cost dynamics and generally higher base metal prices, with Antofagasta advancing after issuing better-than-expected cost guidance and reporting increased quarterly copper production.

Other Global Stock Indices Price Performance

MSCI World Index +7.74% MTD and +3.56% YTD

Hang Seng +4.68% MTD and +1.24% YTD

Over the past seven days, the MSCI World Index and Hang Seng Index are +2.91% and +0.21%, respectively.

Currencies

EUR +2.10% MTD and +0.45% YTD to $1.1798

GBP +2.50% MTD and +0.59% YTD to $1.3552

On Wednesday, the US dollar experienced a modest decline and remained fairly steady throughout the day.

The dollar index decreased by -0.03% to 98.08 after reaching an intraday high of 98.28 and a session low of 98.01. On Tuesday, the dollar index touched 97.96, marking its lowest point since 2 March, the first trading day following the onset of the US - Israeli conflict with Iran. This decline marks the eighth consecutive daily loss for the dollar index, constituting its longest losing streak since a nine-session drop that concluded on 3 December, when investors anticipated at least two 25 bps rate reductions from the Fed this year. Over the past week, the dollar index has fallen -0.93%.

The euro advanced +0.45% to $1.1745 on Wednesday, registering a +1.14% gain over the past seven days.

Sterling paused on Wednesday after its longest rally in a year, declining -0.07% against the dollar to $1.3552. The British pound had nearly achieved a three percent recovery since reaching four-month lows at the end of March, with gains extending over seven consecutive sessions, the longest since last April’s ten-day advance. Over the past week, the pound has risen by +1.13% against the US dollar.

The dollar strengthened +0.11% against the Japanese yen to ¥158.94 on Wednesday, approaching the 160 threshold that has previously prompted currency market interventions by Japanese authorities. Over the past week, the yen has depreciated -0.28%. The yen is -0.16% MTD and -1.46% YTD.

Note: As of 5:00 pm EDT 15 April 2026

Cryptocurrencies

Bitcoin +9.45% MTD and -14.85% YTD to $74,669.70

Ethereum +12.04% MTD and -20.97% YTD to $2,353.89

Bitcoin was +4.36% over the last seven days and Ethereum was +6.29%. On Wednesday, Bitcoin +0.49% and Ethereum +1.26%. The crypto market experienced a strong push this week, with Bitcoin hitting above the $76,000 mark on Tuesday, its highest level since early February, before falling on some profit-taking pushed the price down. The move was supported by a temporary easing in the US-Iran conflict and dollar weakness. The total market cap sits around $2.6 trillion, according to CoinGecko data. Market cap has been boosted by improved sentiment following signs that the conflict with Iran may be ending soon, potentially relieving inflationary pressures and the need for central banks to raise interest rates. There has also been substantial institutional inflows into Spot crypto ETFs and generally increased risk appetite due to a more positive view surrounding potential US political shifts. In addition, short liquidations also played a role in pushing prices higher. This means traders who expected prices to fall were forced to buy back.

Note: As of 5:00 pm EDT 15 April 2026

Fixed Income

US 10-year yield -3.0 bps MTD and +5.0 bps YTD to 4.288%

German 10-year yield +4.0 bps MTD and +19.9 bps YTD to 3.046%

UK 10-year yield -9.8 bps MTD and +22.8 bps YTD to 4.758%

US Treasuries declined on Wednesday, relinquishing some of their recent gains yet remaining within tight trading ranges, as investors continued to monitor developments in the Middle East with caution.

During afternoon trading, the yield on the 10-year Treasury increased +3.4 bps to 4.288%, while the 30-year yield rose +3.5 bps to 4.900%. On the shorter end of the curve, the two-year yield, sensitive to Fed fund rates expectations, climbed +1.5 bps to 3.770%.

Over the past seven days, the US yield curve exhibited a modest steepening, with the spread between two-year and 10-year yields widening to 51.8 bps from 50.7 bps in the previous week.

At the front-end, the 2-year yield declined by -3.0 bps over the past week, the 10-year yield ended the week -1.3 bps lower, and at the longer end, the 30-year yield rose by +1.2 bps.

According to CME Group's FedWatch Tool, Fed funds futures traders are now pricing in a 1.6% probability of a 25 bps rate hike at April’s FOMC meeting, from 1.0% last week. Fed funds futures traders are pricing in 9.4 bps of rate cuts in 2026, higher than the 5.5 bps of rate cuts priced in a week ago.

Across the Atlantic, in the UK, on Wednesday the 10-year gilt rose +3.4 bps to 4.758%. Over the past seven days, it advanced +9.5 bps.

Eurozone bond yields edged higher on Wednesday. Germany’s 10-year government bond yield increased +2.3 bps to 3.046%, following a decline in the previous session. In late March, the yield reached 3.130%, marking its highest point since 2011. At the longer end, the 30-year yield rose +3.5 bps.

The yield on the German 2-year government bond, more responsive to ECB rate expectations, increased +0.6 bps to 2.551%. This followed a decline of -10.3 bps in the prior session.

During the past week, yields rose across the German government bond curve. The yield on the 10-year German bond advanced +9.5 bps, while the two-year Schatz yield was +4.8 bps higher. At the longer end of the spectrum, the 30-year German yield traded +13.5 bps higher.

On Tuesday, ECB President Christine Lagarde stated that the central bank has not yet determined whether the current inflation shock, driven by oil prices, is temporary or if it necessitates an increase in interest rates.

Additionally, President Lagarde indicated that the eurozone economy currently stands between the ‘baseline’ and ‘adverse’ scenarios presented by the central bank. The adverse scenario projects inflation rising to 3.5% in 2026.

According to preliminary data, eurozone inflation surged to 2.5% in March, up from 1.9% in February, as increased oil and gas costs placed upward pressure on prices.

Money markets were most recently pricing in at least two 25 bps rate hikes from the ECB in 2026, with a slight possibility of a third. The probability of a rate increase at the central bank’s April meeting has declined, now standing at approximately 25%, down from 50% on Monday.

On Wednesday, Bundesbank President Joachim Nagel remarked that developments surrounding the Strait of Hormuz will be pivotal in shaping the central bank’s next policy decision. ECB Board Member José Luis Escrivá noted that the baseline scenario for the eurozone economy, which anticipates only a brief impact from the Iran conflict, is currently manifesting in the energy market.

Italy’s 10-year BTP yield edged +0.5 bps higher on Wednesday to 3.807%, with the spread over safe-haven Bunds widened slightly, by 0.3 bps, to 76.1 bps from 75.8 bps the previous week. The Italian 10-year yield advanced +9.8 bps throughout the week.

The yield spread between German Bunds and 10-year UK gilts reached 171.2 bps on Wednesday, an increase of 1.2 bps over the past seven days.

The spread between US 10-year Treasuries and German Bunds is now 124.2 bps, a decrease of 10.8 bps from last week’s 135.0 bps.

Over the course of the week, France’s 10-year OAT yield increased +10.6 bps. The spread between the French OAT 10-year yield and German Bund 10-year yield stood at 63.7 bps, 1.1 bps higher than last week’s 62.6 bps.

Commodities

Gold spot +1.92% MTD and +11.03% YTD to $4,789.94 per ounce

Silver spot +5.84% MTD and +10.94% YTD to $79.05 per ounce

West Texas Intermediate crude -10.01% MTD and +59.19% YTD to $91.39 a barrel

Brent crude -19.77% MTD and +55.84% YTD to $94.92 a barrel

Gold retreated on Wednesday following a brief surge to its highest level in one month. Spot gold declined -1.03% to $4,789.94 per ounce, having earlier reached its strongest value since 18 March. Despite this pullback, gold has risen +0.95% over the past week.

Spot silver decreased -0.60%, settling at $79.05 per ounce. Over the past week, silver prices advanced +6.65%.

Oil prices remained relatively stable on Wednesday, as persistent concerns regarding supply disruptions were counterbalanced by remarks from the US President suggesting that the conflict with Iran may soon end.

Brent crude futures declined by 23 cents, or -0.24%, settling at $94.92 per barrel, while US WTI crude fell by 68 cents, or -0.74%, to close at $91.39 per barrel. Over the past week, WTI declined by -5.30% and Brent by -1.31%.

Forty-five days after Iran's Revolutionary Guards declared the strait closed, effectively restricting approximately one-fifth of global oil and liquefied natural gas shipments, transit remains significantly reduced compared to the more than 130 daily crossings recorded prior to the conflict.

Trade intelligence firm Kpler reported that cumulative losses in Middle Eastern crude and condensate supplies have reached 496 million barrels to date.

US Treasury Secretary Scott Bessent announced on Wednesday that the US will not renew waivers that previously allowed the purchase of Iranian and Russian oil without incurring US sanctions.

During late morning, the Associated Press reported that the US and Iran had agreed to a two-week extension of the ceasefire. While both parties later denied that an agreement had been finalised, they acknowledged that discussions were ongoing via Pakistani mediators. In the afternoon, Reuters sources in Tehran indicated that Iran may allow ships safe passage through the Omani side of the Strait of Hormuz, provided a deal is reached to prevent further conflict.

Following the close of oil trading, MSNBC reported that US and Iranian officials are expected to return to Pakistan next week for further negotiations. The US blockade of Iranian vessels continues, despite Tehran's threats to target regional energy infrastructure and Red Sea exports.

India announced on Wednesday that it will continue to procure oil from diversified sources, which some interpret as an intention to persist with purchases of Russian oil despite the expiration of the US waiver. South Korea has secured 273 million barrels of crude oil from the Middle East and Kazakhstan for delivery through the end of the year, with supplies routed outside the Strait of Hormuz.

The Petroleum Association of Japan reported refinery utilisation at 67.8% last week, remaining largely unchanged w/o/w, as shortages of Middle Eastern crude persist.

Oil product stockpiles at the port of Fujairah reached record lows as of 13 April, with total stocks reported at 9.732 million barrels. This represents a net decrease of 2.823 million barrels w/o/w.

EIA report. The latest US Energy Information Agency (EIA) report, released on Wednesday, showed that US crude oil refinery inputs averaged 16.0 million barrels per day during the week ending 10 April 2026. This was 208 thousand barrels per day less than the previous week’s average. Refineries operated at 89.6% of their operable capacity last week. Gasoline production increased last week, averaging 9.8 million barrels per day. Distillate fuel production decreased, averaging 4.9 million barrels per day.

US crude oil imports averaged 5.3 million barrels per day last week, down by 1.0 million barrels per day from the previous week. Over the past four weeks, crude oil imports averaged about 6.1 million barrels per day, 1.3% less than the same four-week period last year. Total motor gasoline imports last week averaged 316 thousand barrels per day, and distillate fuel imports averaged 118 thousand barrels per day.

Commercial crude oil inventories decreased by 0.9 million barrels from the previous week. US crude inventories, at 463.8 million barrels, are about 1% above the five-year average for this time of year. Total motor gasoline inventories decreased by 6.3 million barrels from last week and are 1% above the five-year average for this time of year.

Distillate fuel inventories decreased by 3.1 million barrels last week and are about 6% below the five-year average for this time of year. Propane/propylene inventories increased by 0.3 million barrels from last week and are 68% above the five-year average for this time of year.

Total products supplied over the last four-week period averaged 20.6 million barrels per day, up by 5.6% from the same period last year. Over the past four weeks, motor gasoline product supplied averaged 8.8 million barrels per day, up by 3.6% from the same period last year. Distillate fuel product supplied averaged 3.9 million barrels per day over the past four weeks, up by 2.2% from the same period last year. However, jet fuel product supplied was down 0.2% compared with the same four-week period last year.

Note: As of 5:00 pm EDT 15 April 2026

Key data to move markets

EUROPE

Thursday: Italian CPI, Eurozone Harmonised Index of Consumer Prices and Core Harmonised Index of Consumer Prices, German Bundesbank ‘Buba’ Monthly Report, ECB Monetary Policy Meeting Accounts, and speeches by ECB Chief Economist Philip Lane, ECB Executive Board member Isabel Schnabel and German Bundesbank President Joachim Nagel

Monday: German PPI

Tuesday: German Current Situation and Economic Sentiment surveys and Eurozone Economic Sentiment survey

Wednesday: Eurozone Consumer Confidence

UK

Thursday: GDP, Industrial Production, Manufacturing Production and a speech by BoE External Member Alan Taylor

Friday: A speech by BoE Deputy Governor for Financial Stability Sarah Breeden

Tuesday: Average Earnings, Claimant Count Change, Claimant Count Rate, Employment Change and ILO Unemployment Rate

Wednesday: CPI, PPI, RPI, Retail PRice Index and a speech by BoE Deputy Governor for Financial Stability Sarah Breeden

USA

Thursday: Initial and Continuing Jobless Claims, Philadelphia Fed Manufacturing Survey and speeches by New York Fed President John Williams and Fed Governor Stephen Miran

Friday: Speeches by San Francisco Fed President Mary Daly and Fed Governor Christopher Waller

Tuesday: ADP Employment Change 4-week Average, Retail Sales, Retail Sales Control Group and Pending Home Sales

CHINA

Sunday: PBoC Interest Rate Decision

JAPAN

Tuesday: Adjusted Merchandise Trade Balance,Imports, Exports and Merchandise Trade Balance Total

GLOBAL

Thursday to Saturday IMF and World Bank spring meeting

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

本文提供給您僅供資訊參考之用,不應被視為認購或銷售此處提及任何投資或相關服務的優惠招攬或遊說。金融商品交易涉及重大損失風險,可能不適合所有投資者。過往績效不代表未來表現。

由專業人士建立。為專業人士打造。