Can the Fed survive Trump?

Corporate Earnings Calendar 24 July - 30 July 2025

Thursday: Valero Energy, Dow, Honeywell International, Keurig Dr Pepper, L3 Harris Technologies, Blackstone, Southwest Airlines, American Airlines, Union Pacific, Newmont, Digital Realty Trust, Intel, Edwards Lifesciences, Deckers Outdoor

Friday: Centene, Phillips 66, Aon, AutoNation, HCA Healthcare, Xerox Holdings, Charter Communications, Sensient Technologies

Monday: Nucor, Waste Management Inc., Whirlpool, Cadence Design Systems, Universal Health Services

Tuesday: Boeing, PayPal Holdings, Procter & Gamble, Spotify Technology, UnitedHealth Group, Ecolab, UPS, Merck & Co., Booking Holdings, MARA Holdings, Mondelez International, Starbucks, Teladoc Health, Visa, Polaris, Sysco, Caesars Entertainment, PPG Industries, Teradyne

Wednesday: Meta Platforms, Microsoft, Qualcomm, ADP, Albemarle, Fair Isaac, eBay, GE Healthcare Technologies, Etsy, Fiverr International, Kraft Heinz, Takeda Pharmaceutical, ARM Holdings, Ford Motor, Hershey, Humana, Evercore, MGM Resorts International, Cognizant Technology Solutions

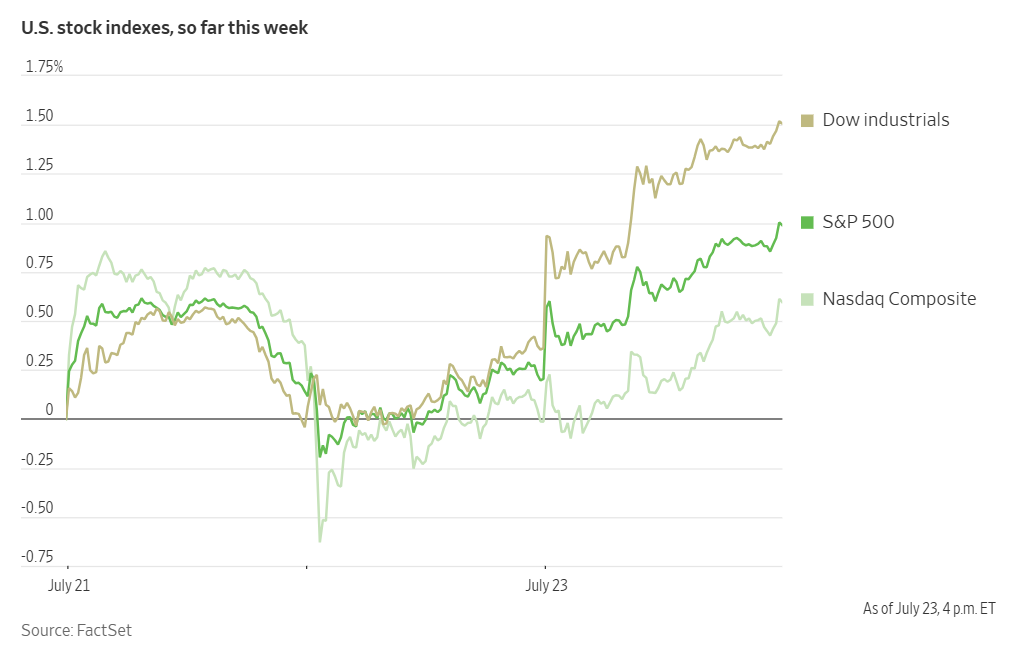

Global market indices

US Stock Indices Price Performance

Nasdaq 100 +2.13% MTD and +10.23% YTD

Dow Jones Industrial Average +0.92% MTD and +4.60% YTD

NYSE +2.41% MTD and +9.56% YTD

S&P 500 +2.48% MTD and +8.11% YTD

The S&P 500 is +1.52% over the past week, with 10 of the 11 sectors up MTD. The Equally Weighted version of the S&P 500 is +2.52% over this past week and +6.96% YTD.

The S&P 500 Consumer Discretionary sector is the leading sector so far this month, +4.12% MTD and -0.28% YTD, while Consumer Staples is the weakest sector at -0.69% MTD and +4.37% YTD.

Over this past week, Consumer Discretionary outperformed within the S&P 500 at +3.01%, followed by Materials and Utilities at +2.89% and +2.88%, respectively. Conversely, Energy underperformed at +0.54%, followed by Information Technology and Consumer Staples at +0.57% and +0.69%, respectively.

The equal-weight version of the S&P 500 was +0.77% on Wednesday, underperforming its cap-weighted counterpart by 0.01 percentage points.

On Wednesday, global financial markets reacted positively to developments in international trade relations, notably the outline of a potential trade agreement between the EU and the Trump administration. This prospective deal, which reportedly involves the EU accepting 15% tariffs on most exports to the US, follows a similar agreement established on Tuesday between the US and Japan.

In response to these signs of de-escalating trade tensions, major stock indices saw significant gains. The S&P 500 advanced by +0.78%, achieving its third consecutive record close. The Nasdaq Composite also climbed, adding +0.61% to close above 21,000 for the first time, reaching 21,020.02. The Dow Jones Industrial Average rose by 508 points, or +1.14%, placing it within 0.10% of its all-time high set in December.

According to LSEG I/B/E/S data, y/o/y earnings growth for the S&P 500 in Q2 is projected to be +7.5%. This number jumps to 9.4% when excluding the Energy sector. Of the 117 companies in the S&P 500 that have reported earnings to date for Q2 2025, 84.6% have reported earnings above analyst estimates, with 80.3% of companies reporting revenues exceeding analyst expectations. The y/o/y revenue growth is projected to be 4.2% in Q1, increasing to 5.5% when excluding the Energy sector.

The Real Estate, Information Technology, Communication Services and Utilities sectors, at 100.0%, are the sectors with most companies reporting above estimates, while Financials with a surprise factor of 10.9%, is the sector that’s beaten earnings expectations by the highest surprise factor. Within Materials, 25.0% of companies have reported above estimates, and it’s also the sector with the lowest surprise factor at 0.2%. The S&P 500 surprise factor is 7.3%. The forward four-quarter price-to-earnings ratio (P/E) for the S&P 500 sits at 22.4x.

In corporate news, International Business Machines (IBM) reported weaker-than-expected Q2 sales in its critical software segment, a development that disappointed investors, who had grown increasingly optimistic about the business's trajectory.

T-Mobile US, the US’ second-largest wireless provider, exceeded analyst expectations for new subscriber additions in the second quarter, overcoming a slow start to the year.

Mattel introduced a revised forecast for its 2025 sales and profit, two months after retracting its previous outlook due to uncertainties related to President Donald Trump’s tariff policies.

Bank of America announced a $40 billion stock-buyback programme. The company’s board authorised the repurchases to begin when the current program is completed on 1 August according to a statement released on Wednesday. As of 30 June 2025, the current programme had approximately $9.1 billion in common stock repurchases remaining.

Mega caps: The Magnificent Seven had a mostly positive performance this week, as Alphabet +3.97%, Tesla +3.39%, Amazon +2.29%, Apple +1.90%, Meta Platforms +1.52%, and Microsoft +0.05%, while Nvidia is -0.34%.

Alphabet’s Q2 earnings. Google's parent company reported a 14% y/o/y increase in revenue, primarily propelled by growth in its cloud computing and search divisions. This positive performance was, however, partially tempered by significant investments in AI. For Q2, Alphabet achieved record sales of $96.4 billion. Concurrently, the company revised its CapEx expectations for the year upwards by 13%, projecting approximately $85 billion, a notable increase from $52.5 billion in 2024.

Alphabet's financial results present a unique dynamic: its cloud division, which provides computing power through data centers, is a direct beneficiary of the burgeoning AI market. In contrast, its foundational search business is navigating challenges as users increasingly gravitate towards AI-driven products like OpenAI's ChatGPT. Furthermore, other segments of the company are allocating substantial resources to integrate AI tools into widely used products such as Search and YouTube.

The cloud unit generated $13.6 billion in revenue during Q2, a 32% y/o/y increase, and an acceleration from Q1’s 28% y/o/y growth. Alphabet's total advertising sales reached $71.3 billion, representing a 10.4% rise compared to the same period last year, with Google's search division, integral to its advertising operations, specifically growing by 11.7%.

Looking ahead, the company anticipates continued strong demand for Google Cloud products, foreseeing a tight demand-supply environment for cloud services extending into 2026. Strong AI adoption across products is noted as a driver for enhancing organic user experiences and improving future monetisation efficiency.

Growth in YouTube subscriptions, encompassing TV, Music, and Premium, remains a key focus alongside advertising revenues. While paid clicks increased by 4% y/o/y, the company noted that product changes occasionally result in fewer clicks but ultimately lead to improved monetisation efficiency.

Tesla Q2 earnings. Tesla’s Q2 net income decreased by 16% y/o/y, from $1.40 billion to $1.17 billion. This marks another quarter of steep declines for the company, primarily driven by a continued reduction in automotive sales. Revenue for Q2 fell by 12% to $22.5 billion, with the automotive segment experiencing a 16% decline and the energy business a 7% reduction.

The company attributed these declines in revenue and profitability to a combination of decreased sales volume and a reduction in regulatory credit revenue. Tesla reported receiving $439 million in revenue from other automakers purchasing carbon credits to offset their conventional vehicle sales, which is less than half the amount reported in the previous year. Many of these credits are anticipated to diminish further in the autumn due to recent changes in federal tax law that have eliminated numerous subsidies for EVs. In Q2, Tesla sold 384,122 vehicles, a decrease from 443,956 units in the corresponding period of the previous year.

Looking ahead, during its earnings call, Tesla anticipates the rollout of Unsupervised Full Self-Driving (FSD) capabilities by the end of 2025 in select US cities, with a prioritisation of safety and regulatory compliance. Production of the Optimus robot is slated to commence in early 2026, with an ambitious target of achieving 100,000 units monthly within five years.

Furthermore, management noted that the company is ramping up production of its more affordable Tesla models, with North American manufacturing having begun in June 2025 and global availability expected in Q4. The topic of investment in X AI was not discussed; however, shareholder proposals are encouraged for decisions regarding the company's strategic direction.

Energy stocks had a positive performance this week, with the Energy sector itself +0.54%. WTI and Brent prices are -1.48% and -0.04%, respectively, this week. Over this past week, Baker Hughes +15.51%, Energy Fuels +14.10%, APA +5.84%, Occidental Petroleum +4.25%, ConocoPhillips +3.86%, Halliburton +3.44%, Phillips 66 +3.38%, Marathon Petroleum +3.00%, BP +2.16%, Chevron +2.13%, and Shell +1.74%, while ExxonMobil -2.05%.

Materials and Mining stocks also had a largely positive performance this week, with the Materials sector +2.89%. Over the past seven days, Sibanye Stillwater +12.66%, CF Industries +1.20%, Albemarle +11.90%, Nucor +5.23%, Newmont Corporation +5.08%, Celanese Corporation +4.97%, Mosaic +4.67%, Freeport-McMoRan +1.96%, and Yara International +1.09%.

European Stock Indices Price Performance

Stoxx 600 +1.63% MTD and +8.39% YTD

DAX +1.39% MTD and +21.76% YTD

CAC 40 +2.41% MTD and +6.36% YTD

IBEX 35 +0.54% MTD and +21.33% YTD

FTSE MIB +0.94% MTD and +17.49% YTD

FTSE 100 +3.43% MTD and +10.87% YTD

This week, the pan-European Stoxx Europe 600 index is +1.55%. It was +1.08% on Wednesday, closing at 550.22.

So far this month in the STOXX Europe 600, Basic Resources is the leading sector, +8.51% MTD and -0.48% YTD, while Technology is the weakest at -2.31% MTD and +1.72% YTD.

This week, Basic Resources outperformed within the STOXX Europe 600, at +5.41%, followed by Travel & Leisure and Construction & Materials at +3.88% and +3.23%, respectively. Conversely, Technology underperformed at -1.49%, followed by Personal & Household Goods and Utilities at -0.22% and +0.13%, respectively.

Germany's DAX index was +0.83% on Wednesday, closing at 24,240.82. It was +0.96% for the week. France's CAC 40 index was +1.37% on Wednesday, closing at 7,850.43. It was +1.66% over the past week.

The UK's FTSE 100 index was +1.51% over the past week to 9,061.49. It was +0.42% on Wednesday.

In Wednesday's trading session, the STOXX Europe 600 index was +1.08%. The Autos & Parts sector emerged as the strongest performer, fuelled by optimism surrounding reduced US tariffs on Japanese automobiles. This move has sparked hopes for similar trade deals with the EU. Analysts highlighted the significance of tariff reductions for a major auto-exporting nation without shipment caps, suggesting potential implications for ongoing negotiations with both the EU and South Korea.

Health Care also outperformed, primarily driven by the sustained strength of major pharmaceutical companies. This despite the US President's pledge to use import restrictions to lower drug prices and other trade barriers. AstraZeneca extended its gains on the back of its US expansion plans, while Lonza Group’s shares surged after exceeding its H1 profit forecasts. Roche Holding drew attention after it halted shipments of Elevidys following actions taken by a US biotech firm.

In the Banks sector, share prices were higher, with UniCredit in the spotlight due to an earnings beat and upgraded full-year guidance. However, UniCredit did withdraw its offer for Banco BPM. Commerzbank shares also gained amid speculation that UniCredit was increasing its stake.

On the downside, Technology shares declined. SAP reported slightly disappointing cloud sales, attributed to tariff concerns, and Texas Instruments' sales guidance underwhelmed as order levels normalised after an early-quarter surge. ASM International saw its Q2 orders fall short of expectations, citing lower bookings from its logic/foundry business. Nokia shares declined after lowering its 2025 profit guidance by up to €310 million, citing the impact of a weaker dollar and tariffs. Other sectors that underperformed included defensive sectors such as Utilities, Telecommunications, and Real Estate.

Other Global Stock Indices Price Performance

MSCI World Index +2.34% MTD and +11.65% YTD

Hang Seng +6.09% MTD and +27.31% YTD

The MSCI World Index is +1.98% over the past 7 days while the Hang Seng Index is +4.16% over the past 7 days.

Currencies

EUR -0.04% MTD and +13.72% YTD to $1.1773.

GBP -1.08% MTD and +8.57% YTD to $1.3581.

The dollar index declined by -0.16% on Wednesday to 97.23. It is -1.09% this week and +0.54% so far MTD. It is -10.40% year-to-date.

On Wednesday, the US dollar exhibited a mixed performance against major currencies. It strengthened against the Swiss franc and the euro, but depreciated against the Japanese yen. This variation may be attributed to the positive market sentiment generated by a new US trade agreement, which was subsequently offset by political uncertainty surrounding the future of Japanese Prime Minister Shigeru Ishiba.

On Tuesday, the US President announced a trade deal with Japan designed to reduce tariffs on Japanese auto imports to 15%. In return, Japan committed to a substantial $550 billion package of US-bound investments and loans. This agreement contributed to the dollar's appreciation against the Swiss franc, positioning it to break a three-session losing streak. The dollar advanced by +0.24%, reaching 0.7942 against the Swiss franc.

Conversely, the dollar weakened against the yen, reaching its lowest level since 11th July, trading at ¥146.20 per dollar. This decline followed reports indicating that Prime Minister Ishiba intended to resign next month after a significant defeat in the upper house election. Ishiba subsequently denied these reports as ‘completely unfounded.’ The yen increased +0.14%, trading at ¥146.40. This week, the dollar has depreciated by -1.01% against the Japanese yen. However, it has gained +1.69% MTD, though it is -6.63% YTD.

Diplomatic sources indicate that the EU and the US are progressing towards a trade agreement that would establish a broad 15% tariff on EU goods imported into the US. The euro, initially experiencing losses on Wednesday, but pared them to advance +0.20% against the dollar, reaching $1.1773. The euro registered a weekly +1.13% rise against the dollar.

Sterling strengthened against both the dollar and the euro on Wednesday. This was primarily attributed to the overall optimism in global markets following the trade deal between the US and Japan. The pound gained +0.42% against the dollar, reaching $1.3581, its highest in nearly two weeks, and is nearing its early July peak of $1.3787. Sterling also showed greater strength against the euro, which depreciated by -0.24% to 86.62 pence. Upcoming economic indicators, including today's business activity data and Friday's retail sales figures, are expected to provide further insights into the health of the British economy.

Note: As of 5:00 pm EDT 23 July 2025

Fixed Income

US 10-year yield +16.0 bps MTD and -18.8 bps YTD to 4.388%.

German 10-year yield +3.2 bps MTD and +27.0 bps YTD to 2.639%.

UK 10-year yield bps +16.0 MTD and +8.0 bps YTD to 4.648%.

On Wednesday, US Treasury prices declined as global markets shifted to a ‘risk-on’ sentiment. This shift was primarily attributed to a trade deal between the US and Japan, alongside the anticipation of a potential agreement with the EU.

The trade agreement with Japan, following similar accords with the Philippines and Indonesia, significantly bolstered Japan's Nikkei index, with automaker shares particularly benefitting. This positive development injected optimism across financial markets, fostering expectations that a trade deal with the EU could be announced prior to the 1st August tariff deadline.

Data released indicated that US existing home sales in June fell more substantially than anticipated. Following this data release, bond yields exhibited a marginal decline.

The 10-year Treasury yield was +3.8 bps to 4.388%. The two-year yield settled at 3.886%, a +3.4 bps increase for the day. On the long end of the maturity spectrum, the 30-year yield was +2.2 bps to 4.986%

A US government debt sale of $13 billion in 20-year bonds on Wednesday was met with strong demand. These bonds were issued with a high yield of 4.935%, which was nearly 2 bps below the market rate at the bidding deadline. This indicated investors' willingness to pay a premium to acquire the new issuance.

Over the past seven days, the yield on the 10-year Treasury note is -3.5 bps. The yield on the 30-year Treasury bond is -4.5 bps. On the shorter end, the two-year Treasury yield is +0.6 bps.

Fed funds futures traders are now pricing in a 2.6% probability of a July cut next week, down from 4.1% last week, according to CME Group's FedWatch Tool. A rate cut at September’s Fed meeting now is seen as the next most likely, with a 62.8% probability. Traders are currently pricing in 44.4 bps of cuts by year-end, lower than last week’s 46.5 bps.

Across the Atlantic, in the UK, on Wednesday the 10-year gilt was +7.3 bps to 4.648%. The UK 10-year yield is +0.7 bps over the past 7 days. On Tuesday it was reported that the UK experienced a surge in debt-interest payments which made the budget deficit rise to £20.7 billion, £6.6 billion more than a year earlier.

Eurozone government bond yields exhibited a mixed performance on Wednesday as investors assessed the implications of the trade deal between Japan and the US and its potential impact on future US trade agreements. Over the prior two sessions, euro area borrowing costs had declined as investor attention shifted towards the potential deflationary effects of prospective US trade duty increases and an appreciating euro.

Germany's 10-year government bond yield was +4.7 bps to 2.639%, following a reduction of over 10 bps in the prior two sessions. Similarly, Germany's 2-year government bond yield, which is more sensitive to expectations regarding ECB monetary policy, rose by +3.8 bps to 1.857%. The 30-year yield was +5.6 bps to 3.174%. The German yield curve had flattened on Monday and Tuesday, indicating a pause in the month-long steepening trend that reflected a widening spread between short- and long-term yields.

The ECB is widely anticipated to maintain its current interest rates today, reiterating its data-dependent policy stance while awaiting a potential trade agreement between Washington and Brussels. Money markets are currently fully pricing in an ECB deposit facility rate of 1.75% by December, a reduction from the current 2.00%, and assign a 48% probability to a 25 bps rate cut in September.

In contrast, Italy's 10-year government bond yields experienced a marginal decline of -0.1 bps, settling at 3.436%. The spread between Italian BTP and German Bund yields stood at 79.7 bps. This spread had reached 84.20 bps in June, its lowest level since March 2015.

Over the past seven days, the German 10-year yield was -5.5 bps. Germany's two-year bond yield was -0.8 bps, and on the longer end of the curve, Germany's 30-year yield was -4.7 bps.

The spread between US 10-year Treasuries and German Bunds is now 169.9 bps, about 6 bps less than last week’s 176 bps.

Similarly, Italy's 10-year yield, which serves as the benchmark for the eurozone's periphery, was -0.1 bps to 3.436%. This spread between Italian and German 10-year yields stood at 79.7 bps, contracting by 6.6 bps from 86.3 bps last week. The Italian 10-year yield is -12.1 bps over the past 7 days.

Commodities

Gold spot +2.57% MTD and +29.10% YTD to $3,387.42 per ounce.

Silver spot +8.85% MTD and +35.98% YTD to $39.28 per ounce.

West Texas Intermediate crude +0.82% MTD and -8.73% YTD to $65.42 a barrel.

Brent crude +1.54% MTD and -8.00% YTD to $68.67 a barrel.

Gold prices are +1.04% this week and +29.10% YTD. On Wednesday, gold prices declined by -1.28% to $3,387.42 per ounce, retreating from a session peak that had marked its highest level since 16th June.

On Wednesday, two diplomats reported that the US and the EU are nearing a trade agreement that would establish a broad 15% tariff on EU goods imported into the US. This news came as the US President also finalised a trade deal with Japan the day before to reduce tariffs on auto imports, offering a sign of progress in broader trade negotiations.

Oil prices were largely unchanged on Wednesday as investors weighed evolving trade developments against potential geopolitical supply risks.

Brent crude futures concluded the session down 8 cents, or -0.12%, at $68.67 a barrel. Similarly, WTI crude futures fell by the same margin to settle at $65.42 per barrel. The market's stability came as traders assessed ongoing trade negotiations between the EU and the US, following the US tariff deal with Japan.

Prices found a floor due to potential supply-side pressures, averting a sharper decline. This was supported by the US Energy Secretary's comments on Tuesday, suggesting Washington would consider sanctioning Russian oil to help conclude the conflict in Ukraine. This potential action follows the EU's move last Friday to approve its 18th sanctions package against Russia, which included lowering the price cap on the country's crude exports.

This week, WTI and Brent are -1.48% and -0.04%, respectively.

EIA weekly report. US crude oil and gasoline inventories dropped last week, driven by robust demand and increased exports, according to data released Wednesday by the US Energy Information Administration (EIA). Conversely, distillate stockpiles saw a rise.

For the week ending 18th July, crude inventories decreased by 3.2 million barrels, settling at 419 million barrels. While overall crude stocks fell, those at the Cushing, Oklahoma, delivery hub experienced a modest increase of 455,000 barrels. The decline in inventories was further influenced by a jump in US crude exports, which rose by 337,000 barrels per day (bpd) to 3.86 million bpd. Simultaneously, net US crude imports declined by 740,000 bpd.

Refinery crude runs also increased by 87,000 bpd, with utilisation rates in the vital Gulf Coast refinery hub reaching a one-year peak of 96.1%.

Gasoline stocks mirrored the trend in crude, falling by 1.7 million barrels last week to 231.1 million barrels. This drop aligns with a significant rise in gasoline product supplied (a key indicator of demand), which climbed by 478,000 bpd to 8.97 million bpd. The four-week average for product supplied stood at 8.81 million bpd, though this was lower than the 9.27 million bpd recorded during the same period last year.

In contrast to crude and gasoline, distillate stockpiles—which encompass diesel and heating oil—expanded by 2.9 million barrels during the week, reaching 109.9 million barrels.

Global gas demand: slow growth in 2025 paves way for record highs in 2026. According to the International Energy Agency’s Q3 Gas Market Report, global natural gas demand saw structural growth return in 2024 and continued to expand slowly in H1 2025. Preliminary data indicates a modest 1% y/o/y increase in global consumption, driven almost entirely by adverse weather in Europe and North America. European demand rose by 6.5% y/o/y, supported by gas-fired power generation amid low wind and hydro output. North American demand grew by an estimated 2.5%, spurred by a cold first quarter.

In contrast, demand in Asia was subdued due to macroeconomic uncertainty and high spot liquefied natural gas (LNG) prices. China’s demand fell by an estimated 1% y/o/y, with its LNG imports plummeting over 20%. India's consumption declined by 7% y/o/y, mainly from lower industrial use.

Market fundamentals remained tight in the first half of 2025. Global LNG supply grew by only 4% (12 billion cubic meters, or bcm), largely from the new Plaquemines LNG facility in the US. This was offset by a 45% (6.5 bcm) drop in Russian piped gas to the EU and a 4.5% (3 bcm) decline in Norwegian supplies due to maintenance. Europe’s need to refill storage, which started the season 42% (25 bcm) lower than the previous year, further tightened the market. Consequently, Europe's LNG imports surged by 25% to a record 92 bcm. This tightness pushed European hub prices up 40% and Asian spot LNG prices up 28% compared to the first half of 2024, curbing Asian demand.

For the full year 2025, global gas demand growth is forecast to slow to 1.3%, with the Asia-Pacific region expanding by less than 1%. Global LNG supply is expected to increase by 5.5% (30 bcm), mainly from North American projects. However, this will be partially offset by an anticipated 13 bcm drop in Russian piped gas deliveries to Europe for the year.

The outlook for 2026 is more robust. A significant increase in LNG supply, projected to grow by 7% (40 bcm) from new projects in the US, Canada, and Qatar, is expected to ease market fundamentals. This will likely drive global gas demand growth to accelerate to around 2%, reaching a new all-time high. Asia is forecast to lead this resurgence, with demand rising over 4% and accounting for half of the global increase. Conversely, European demand is set to decline by 2% due to expanding renewables.

Note: As of 5:00 pm EDT 23 July 2025

Key data to move markets

EUROPE

Thursday: German GfK Consumer Confidence Survey, French HCOB Composite, Services and Manufacturing PMIs, German HCOB Composite, Services and Manufacturing PMIs, Eurozone Composite, Services and Manufacturing PMIs, ECB Monetary Policy Statement, Main Refinancing Operations Rate, ECB Rate on Deposit Facility, and Press Conference.

Friday: German IFO Business Climate, Current Assessment and Expectations Surveys.

Tuesday: Spanish GDP.

Wednesday: German GDP and Retail Sales, Spanish Harmonised Index of Consumer Prices, Eurozone Business Climate, Consumer Confidence, and Economic Sentiment Indicator, and Eurozone GDP.

UK

Thursday: S&P Global Composite, Services and Manufacturing PMIs and GfK Consumer Confidence Survey.

Friday: Retail Sales.

USA

Thursday: Initial and Continuing Jobless Claims, S&P Global Composite, Services and Manufacturing PMIs, and New Home Sales Change.

Friday: Durable Goods and Non-Defence Capital Goods Orders.

Tuesday: Housing Price Index, Consumer Confidence and JOLT Job Openings.

Wednesday: GDP, Core Personal Consumption Expenditures, Persona Consumption Expenditures, Pending Home Sales, and Fed Interest Rate Decision, Monetary Policy Statement, and FOMC Press Conference.

JAPAN

Thursday: Tokyo CPI.

Wednesday: Large Retailer Sales and Retail Trade.

Global Macro Updates

Tariffs and the President put the Fed under pressure. Since US President Donald Trump first announced his ‘liberation day’ tariffs on 2 April and then a ‘90 day reprieve’, followed by a new deadline of 1 August, the Fed has been waiting to see what effect these tariffs would actually have on growth, consumer confidence and inflation.

The tariff situation still remains in limbo: the latest ‘deal’ was with the Japanese government acquiescing to a 15% tariff on all goods exported to the US, reduced from the 25% tariff rate threatened in President Trump’s 7 July letter. Japanese automobile exports, which had already been subject to an additional 25% industry-specific tariff since April, will instead receive 15% tariffs, including a preexisting tariff of 2.5%. The 50% tariff on steel and aluminium were not included in the deal and remain.

According to the Financial Times, Washington and Brussels are nearing an outline trade agreement. This potential deal would entail the EU accepting a 15% tariff on most of its exports to the US, a concession seemingly influenced by the US' recent similar agreement with Japan. While this 15% rate is higher than the 10% temporary tariff in place since trade talks began in April, Brussels is reportedly considering it to avert a more severe 30% tariff threatened by the US for 1st August.

Under the proposed arrangement, both parties might agree to waive tariffs on specific products, including aircraft, spirits, and medical devices. Additionally, automotive tariffs are expected to decrease from the current 27.5% to 15%. However, this lower tariff on Japanese autos, now below those applied to vehicles from Canada or Mexico, which heavily supply the US domestic auto industry, has reportedly caused dissatisfaction among some US automakers. Conversely, imports of steel and aluminum could face significantly higher tariffs of 50% above a certain quota.

The US - Japan agreement on Tuesday appears to have grudgingly nudged European negotiators towards accepting this higher reciprocal tariff rate in an effort to avoid a full-blown trade war. Nevertheless, reports also suggest that the EU remains prepared to retaliate if the Trump administration attempts to impose further demands or follows through with its threat of a 30% tariff. The European Commission is reportedly poised to receive approval to trigger its strongest anti-coercion instrument measures, with preparations underway for potential retaliatory tariffs of 30% on €93 billion worth of US goods should no deal be finalised by 1st August.

The trade uncertainty is having a definite impact on Fed policy. President Trump has repeatedly criticised Fed chair Jerome Powell because the Fed has not cut rates again this year after cutting it three times last year. Powell says the Fed wants to see how the economy responds to Trump's sweeping tariffs on imports, which Powell says could push up inflation. However, President Trump and Treasury Secretary Scott Bessent have continued to apply pressure, demanding the Fed deliver an immediate 300 bps rate cut, and even suggested despite legal questions over President Trump’s authority to do so, that Powell could be fired before his term as Fed chair officially expires in May 2026. This suggestion last week caused an instant market reaction with bond yields rising and equity markets falling before President Trump quickly said he would not be firing Powell. However, rumours have continued to swirl as Bessent stated on Tuesday that he wanted a review of the Fed’s operations.

The Federal Reserve has not just had to worry about weighing the potential impact of tariffs, which essentially result in a sort of supply shock, causing inflation and employment to move in opposite directions as noted in the Financial Times by Kristin Forbes, a professor of global economics at the MIT-Sloan School of Management, thereby pulling the Fed to focus more on one of its mandates than the other. The Fed is also now having to worry about both the impact on its credibility caused by claims of political partiality from Treasury Secretary Scott Bessent, who said on Wednesday that "The Fed publishes something called a summary of economic projections, and it's pretty politically biased” as well as investor concerns around its independence given the political interference on its decisions by President Trump. The continuing criticism of Powell could further reduce the ability of the Fed to conduct policy and its transmission via financial markets. The Fed’s credibility is viewed by many as key to keeping inflation expectations anchored.

President Trump is scheduled to visit the Fed on Thursday — the first time in almost 20 years a US president has paid an official visit to the central bank. Investors will be watching closely.

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

本文提供給您僅供資訊參考之用,不應被視為認購或銷售此處提及任何投資或相關服務的優惠招攬或遊說。金融商品交易涉及重大損失風險,可能不適合所有投資者。過往績效不代表未來表現。

由專業人士建立。為專業人士打造。