Corporate Earnings News

Global market indices

Currencies

Cryptocurrencies

Fixed Income

Commodity sector news

Key data to move markets

Global macro updates

Corporate Earnings News

Corporate earning calendar 14 November - 20 November 2024

Thursday: The Walt Disney Co., JD.com, Applied Materials

Friday: Alibaba

Monday: Symbotic, American Eagle Outfitters

Tuesday: Walmart, Lowe’s, Medtronic, XPeng, Keysight Technologies, Viking Holdings

Wednesday: Nvidia, Palo Alto Networks,Snowflake, Target

Global market indices

US Stock Indices Price Performance

Nasdaq 100 +5.93% MTD +25.23% YTD

Dow Jones Industrial Average +5.14% MTD +16.51% YTD

NYSE +3.15% MTD +17.76% YTD

S&P 500 +4.91% MTD +25.48% YTD

The S&P 500 is +0.95% over the past week, with 8 of the 11 sectors up MTD. The Equally Weighted version of the S&P 500 is +0.39% this week, its performance is +4.13% MTD and +16.19% YTD.

The S&P 500 Consumer Discretionary sector is the leading sector so far this month, up +12.18% MTD and +25.01% YTD, while Utilities is the weakest at -2.15% MTD and +23.38% YTD.

This week, Consumer Discretionary outperformed within the S&P 500 at +4.46%, followed by Consumer Staples and Communication Services at +1.66% and +1.64%, respectively. Conversely, Materials underperformed at -2.29%, followed by Health Care and Financials, at -0.90% and +0.28%, respectively.

US equities experienced a volatile session on Wednesday, as speculation that the market's post-election rally may have extended too far was offset by expectations of continued interest rate cuts by the Fed.

The major indices initially advanced, fueled in part by inflation data that aligned with forecasts. However, equities lost momentum in the final hours of trading in New York, with the S&P 500 nearly relinquishing its earlier gains. The Dow Jones Industrial Average ultimately closed with a modest gain of +0.1% at 43,958.19, while the S&P 500 eked out a marginal increase of less than +0.1% after experiencing its biggest five-day streak in a year. The technology-heavy Nasdaq Composite Index, however, was -0.3%.

According to Citigroup, options market activity suggests that investors are more focused on the potential for a significant move in the S&P 500 next week, following Nvidia’s Q3 earnings report, than they were on Wednesday's CPI data. Traders are pricing in a 0.9% move for the benchmark index in either direction on 21st November, the trading session following the chipmaker's earnings release after the closing bell next Wednesday.

Over the next month, Nvidia's earnings are now considered the most significant event for the stock market. This highlights a tendency for short-term concerns about macroeconomic data to take a backseat to developments in the technology sector, where the focus remains on breakthroughs in AI.

In corporate news, Advanced Micro Devices announced a reduction of approximately 1,000 jobs as part of a strategic shift towards newer markets, including artificial intelligence chips.

Spirit Airlines is reportedly nearing a deal with creditors to restructure its substantial debt load in bankruptcy court, following the collapse of discussions for a merger with rival Frontier Group Holdings.

Mastercard projected slower annual net revenue growth for the 2025 to 2027 period, as the company aims to capture a larger share of the digital payments market.

US stocks

Mega caps: A positive week for the ‘Magnificent Seven’ with 6 members in positive territory, 3 of them with double-digit gains. Alphabet +4.54%, Amazon +14.86%, Apple -0.35%, Meta Platforms +2.19%, Microsoft +4.64%, Nvidia +10.18%, and Tesla +32.18%.

Energy stocks had a mostly positive week, as the Energy sector itself was +0.86% due to Q3 earnings reports exceeding expectations by major oil companies, despite a fall in oil prices. Oil prices are down more than 4% this week. The Energy sector’s YTD performance is +13.03%. Over the week Energy Fuels +6.04%, Marathon Petroleum +2.49%, Phillips 66 +1.57%, Baker Hughes +0.77%, Chevron +0.63%, ExxonMobil +0.39%, while Occidental Petroleum -0.53%, Halliburton -1.02%, ConocoPhillips -1.59%, Shell -2.60%, and Apa -10.96%.

Materials and Mining stocks had a negative week, as the Materials sector underperformed every other sector at -2.29%, bringing the sector’s YTD performance to +7.92%. Albemarle +12.02%, CF Industries +2.56%, while Mosaic -5.33%, Yara International -7.14%, Newmont Corporation -7.31%, Freeport-McMoRan -8.00%, Sibanye Stillwater -8.19%, and Nucor -9.26%.

European Stock Indices Price Performance

Stoxx 600 -0.75% MTD +4.72% YTD

DAX -0.39% MTD +13.44% YTD

CAC 40 -1.82% MTD -4.33% YTD

IBEX 35 -2.53% MTD +12.62% YTD

FTSE MIB -1.67% MTD +11.06% YTD

FTSE 100 -0.98% MTD +3.84% YTD

This week, the pan-European Stoxx Europe 600 index was -1.02%. It was -0.54% on Wednesday, closing at 501.59.

This month so far in the STOXX Europe 600, Travel & Leisure is the leading sector, +3.53% MTD and +10.19% YTD, while Autos & Parts is the weakest at -4.66% MTD and -16.11% YTD.

This week Technology outperformed within the STOXX Europe 600 with a +1.29% gain, followed by Travel & Leisure and Construction Materials at +0.89% and +0.16%, respectively. Conversely, Basic Resources underperformed at -5.25%, followed by Personal & Household Goods and Chemicals, -2.81% and -2.73%, respectively.

Germany's DAX index was -0.16% on Wednesday and closed at 19,003.11. It was -0.19% for the week. France's CAC 40 index was -0.14% on Wednesday, closing at 7,216.83. It was -2.07% for the week.

The UK's FTSE 100 index was -1.67% this week to 8,030.33. It was +0.06% on Wednesday.

On Wednesday, the Stoxx Europe 600 Real Estate sector experienced the sharpest decline as traders increased their bets on further Treasury yield declines. This stems from the belief that the suggested policies of the incoming Trump administration will stimulate inflation, leaving the Fed little choice but to keep rates high. Real Estate, due to its interest rate sensitivity, is perceived as a bond proxy, making it susceptible to fluctuations, particularly due to the prevalence of leveraged landlords.

The Autos & Parts sector also suffered significant losses, largely attributed to the risks associated with potential trade tariffs. Within this sector, attention focused on Volkswagen increasing its JV investment in Rivian Automotive to $5.8 billion.

Technology stocks faced downward pressure as well, with reports from Bloomberg highlighting challenges faced by major technology companies like OpenAI, Google, and Anthropic in developing more advanced AI models. These reports have fueled concerns that the growth of new AI models may have plateaued.

In contrast, the Energy sector emerged as the top performer, driven by strong 3Q results from Siemens Energy. These results included a positive surprise in FCF, and the company's guidance for 2024 surpassed consensus estimates.

The Basic Resources sector received a boost from news of China implementing tax cuts for home buyers to stimulate its property market.

Utilities attracted attention as RWE AG announced a share buyback program worth up to €1.6 billion and slightly raised its full-year outlook.

The Insurance sector also advanced, with Allianz SE reporting better-than-expected results across most lines in Q3 and raising its FY 2024 guidance.

Other Global Stock Indices Price Performance

MSCI World Index +3.29% MTD +18.87% YTD

Hang Seng -2.31% MTD +6.83% YTD

This week, the Hang Seng Index was -3.37%, while the MSCI World Index was +0.40%.

Currencies

EUR -2.96% MTD -4.31% YTD to $1.0563.

GBP -1.53% MTD -0.25% YTD to $1.2710.

The euro was -1.55% against the USD over the past week, while the British pound was -1.26%. The Dollar Index was +1.22% this week, +2.47% MTD, and +5.14% YTD, settling at 106.48.

The US dollar surged to a one-year high against major currencies on Wednesday due to ongoing concerns over the proposed economic policies under the new US administration. The October inflation figures met expectations at +0.2% for the month. It took the 12-month inflation rate to +2.6%, up 0.2% from September. This has reinforced the likelihood of continued interest rate reductions by the Fed.

The dollar index climbed +0.41% to 106.48, after peaking at 106.53.

The British pound struggled near three-month lows against the dollar. This followed a significant decline in the previous session triggered by data indicating easing inflation in the UK. Sterling was -0.30% to $1.2710 after data revealed the slowest growth in regular pay for British workers in two years during the third quarter and a cooling labour market, with unemployment rising from 4% in August to 4.3% in September. However, wage stickiness, with pay growth excluding bonuses slowing only marginally to 4.8% in the three months through September, does have the Bank of England (BoE) worried, with BoE Chief Economist Huw Pill saying that the “elevated levels” are “hard to reconcile with the UK inflation target.” Currently, market expectations reflect a 15% probability of a 25 bps rate cut by the BoE in December. The pound remained stable at 83.31 pence per euro.

The euro extended its decline amidst concerns over potential US tariffs. Further pressure on the currency stems from political instability in Germany, the eurozone's largest economy. The collapse of Chancellor Olaf Scholz's governing coalition last week and the upcoming snap elections scheduled for 23rd February have contributed to the euro's weakness. The euro was -0.52% to $1.0563, having touched $1.0555, its lowest point since November 2023.

In Japan, nominal inflation accelerated in October, reaching its highest annual rate in over a year. This surge complicates the BoJ's decision regarding the timing of interest rate increases. The yen weakened past ¥155 per dollar, marking its lowest level since late July, before recovering slightly to ¥155.44, a +0.59% increase.

Note: As of 5:15 pm EST 13 November 2024

Cryptocurrencies

Bitcoin +28.34% MTD +115.02% YTD to $89,822.59.

Ethereum +26.97% MTD +39.15% YTD to $3,183.06

Cryptocurrencies have continued to surge this week, with Bitcoin up over 30% since the US election. It reached a record high on Wednesday, peaking just north of $93,400 before falling back. According to CoinGecko data, the value of the global cryptocurrency market topped $3.2 trillion on Wednesday as investors have piled into Bitcoin and Ethererum following the election of Donald Trump. The Bitcoin Dominance Index, which measures bitcoin's share of the overall crypto market, reached 61.39%, a level not seen since March 2021. Although Ethereum has gained in value post election, it has lost nearly all of the gains it made against Bitcoin dominance since Election day. It appears that investors are counting on Trump’s pre-election promises of making the US the “crypto capital” of the world. They expect to see a friendlier regulatory environment for crypto if Trump does fire SEC Chair Gary Gensler as promised. The likelihood of friendlier crypto regulation has also been boosted by the election of South Dakota Republican John Thune as Senate Majority Leader as he is a known crypto-friendly politician.They also see the value of cryptocurrencies increasing with the suggested creation of a "strategic national bitcoin stockpile.”

Note: As of 5:15 pm EST 13 November 2024

Fixed Income

US 10-year yield +17.8 bps MTD +58.7 bps YTD to 4.468%.

German 10-year yield +0.5 bps MTD +38.6 bps YTD to 2.395%.

UK 10-year yield +9.2 bps MTD +98.4 bps YTD to 4.523%.

US Treasury 10-year bond yields are +3.3 bps this week as uncertainty around where the neutral rate, the level where rates neither fuel or dampen economic growth, should be appears to be rising. Several Fed speakers have suggested that it has risen since the pandemic and that structural changes in the US economy are stil not fully understood.

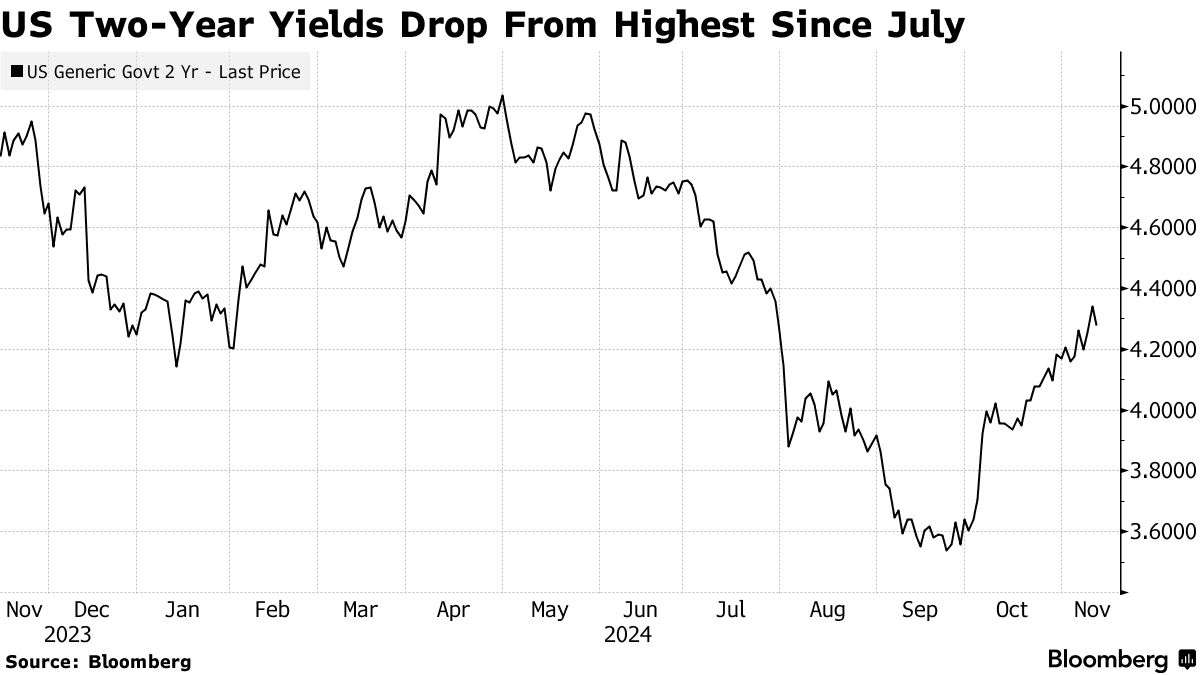

US Treasury yields presented a mixed picture on Wednesday. Shorter-term yields declined following the release of inflation data that aligned with expectations, reinforcing the view that the Federal Reserve remains on track to implement another 25 bps interest rate cut next month. The yield on the 2-year Treasury note, a key indicator of interest rate expectations, was -6.9 bps to 4.275%.

Conversely, yields on longer-term maturities, led by the 10-year Treasury note, rose in response to a wave of corporate bond issuances on Wednesday, which followed approximately $30 billion in offerings on Tuesday. The yield on the 10-year note edged up +2.8 bps to 4.468%, while the yield on the 30-year Treasury bond was +6.3 bps to 4.632%.

Following the release of the Consumer Price Index (CPI) data, federal funds futures now reflect an 83.0% probability of a 25 bps rate cut at the FOMC monetary policy meeting next month, with a 17% probability that the central bank will maintain its current policy stance, according to the CME Group's FedWatch Tool. This represents a shift from late Tuesday, when the probability of a rate cut was priced at 58.7%.

Looking further ahead, futures markets now imply 52 bps in cumulative rate reductions for 2025, compared to 45 bps implied in the previous session.

The release of the CPI data also impacted inflation expectations. The break-even inflation rate on 5-year US TIPS dipped to 2.413% from 2.433% on Tuesday. This rate, which had surged more than 50 bps since reaching a four-year low on 10th September, suggests that traders expect US inflation to average approximately 2.41% over the next five years.

The German 10-year yield was -1.3 bps this week, while the UK 10-year yield was -4.1 bps this week. The spread between US 10-year Treasuries and German Bunds currently stands at 207.3 bps, 4.6 bps higher than last week.

Italian bond yields, a benchmark for the eurozone periphery, were -9.6 bps this week to 3.628%. Consequently, the spread between Italian and German 10-year yields is 123.3 bps, 8.3 bps lower than last week.

Eurozone government bond yields retreated from their intraday highs on Wednesday following the release of US inflation data, which met market expectations for October. The data had a limited impact on expectations for ECB monetary policy, with traders now anticipating the deposit rate to reach 1.95% by July 2025, down slightly from around 1.96% earlier.

Germany's 2-year government bond yield, which is highly sensitive to changes in ECB rate expectations, was +1.3 bps at 2.142%, after having reached a session high of 2.191%. The yield on the 10-year German government bond rose +2.7 bps to 2.395%, retreating from an earlier high of 2.401%.

The eurozone is grappling with a combination of structural challenges, such as elevated energy costs and diminished productivity, alongside weak cyclical economic data. These factors are expected to lead to lower inflation expectations, a lower terminal rate for the ECB, and a weaker euro.

Additionally, Friedrich Merz, leader of Germany's conservative Christian Democratic Union (CDU) and a leading contender to become the country's next chancellor, indicated a potential openness to reforming Germany's debt brake under certain circumstances. The debt brake, a constitutional rule, limits the federal government's structural budget deficit to 0.35% of GDP.

Commodities

Gold spot -5.75% MTD +25.14% YTD to $2,572.66 per ounce.

Silver spot -7.43% MTD +26.03% YTD to $30.34 per ounce.

West Texas Intermediate crude -2.08% MTD -5.23% YTD to $68.09 a barrel.

Brent crude -0.84% MTD -6.27% YTD to $72.03 a barrel.

Gold prices are -3.26% down this week, nearing a two-month low. Gold prices continued their decline for a fourth consecutive session on Wednesday, pressured by a strengthening US dollar, despite US inflation data reinforcing expectations of a further Federal Reserve rate cut next month.

Spot gold retreated -0.98% to $2,572.66 per ounce. This decline coincided with the US dollar approaching a one-year high against major currencies and a rise in the yield on the US 10-year Treasury note.

Traders will be closely monitoring upcoming economic indicators, including the US PPI and weekly jobless claims data due today, followed by retail sales figures on Friday. Furthermore, remarks from Federal Reserve Chair Jerome Powell and other central bank officials will be closely scrutinised for insights into future monetary policy.

This week, WTI and Brent, both registered significant losses, -5.07% and -4.16%, respectively.

Oil prices experienced a modest recovery on Wednesday, driven by short-covering following a decline to a near two-week low the previous day. This decline was triggered by OPEC's downward revision of its global oil demand growth forecasts for 2024 and 2025, attributed to weaker demand in key regions such as China and India. Notably, this marked the organisation's fourth consecutive downward adjustment for 2024. However, gains were limited as the US dollar reached a one-year high, exerting downward pressure on oil prices.

However, the US Energy Information Administration (EIA) reported that both US and global oil production are projected to reach new record highs this year, surpassing earlier forecasts. US oil output is now expected to average 13.23 million barrels per day (bpd) in 2024, while global production is anticipated to reach 102.6 million bpd.

The International Energy Agency (IEA), which has presented a more conservative demand growth forecast than OPEC, is scheduled to release its updated estimates today.

Geopolitical factors are also playing a role in shaping market sentiment. Iran's oil minister, as reported by the ministry's news website Shana, announced that Tehran has formulated plans to maintain its oil production and exports, indicating preparedness for potential US oil sanctions.

Preliminary data from the American Petroleum Institute (API) indicated a decline in US crude stocks by 777,000 barrels last week. Official government data on US crude inventories, which was delayed by one day due to the Veterans Day holiday on Monday, is scheduled for release today at 11:00 am ET.

EIA outlook: Oil supply outpaces demand growth.

The US Energy Information Administration (EIA) announced on Wednesday that both US and global oil production are projected to reach new record highs this year. This surge in oil supply, coupled with weakening demand growth, has driven oil prices to their lowest point since 2021, despite significant production cuts implemented by OPEC+.

US oil output is now anticipated to average 13.23 million barrels per day (bpd) in 2024, surpassing last year's record of 12.93 million bpd by approximately 300,000 bpd. This represents a slight upward revision from the EIA's earlier forecast of 13.22 million bpd. Looking ahead to 2025, the EIA's November Short-Term Energy Outlook (STEO) projects US oil production to reach 13.53 million bpd, a minor downward adjustment from the 13.54 million bpd forecast in the October STEO.

Globally, the EIA has increased its 2024 oil output forecast to 102.6 million bpd, up from its previous estimate of 102.5 million bpd. For 2025, world oil production is expected to reach 104.7 million bpd, a slight increase from the previous projection of 104.5 million bpd.

Forecasting oil demand growth has been a point of contention among leading energy analysts, primarily due to differing perspectives on China's consumption patterns and the pace of transition towards alternative energy sources. The EIA now anticipates global oil demand to grow by approximately 1 million bpd in 2024, an upward revision from its previous forecast of 900,000 bpd. This contrasts with OPEC's latest forecast, which still anticipates a considerably higher growth rate of 1.82 million bpd. The International Energy Agency, headquartered in Paris, predicts a more moderate growth of 860,000 bpd.

While the EIA acknowledges that OPEC+ production cuts are likely to support global oil prices through the first quarter of 2025, it cautions that continued adherence to these cuts, which have been in effect for over two years, may be waning among members of the group. The EIA notes, "Although we assess that OPEC+ producers will likely continue to limit production below recently announced targets in 2025, the potential for weakening commitment among OPEC+ producers to continue cutting production adds downside risk to oil prices."

Note: As of 5:15 pm EST 13 November 2024

Key data to move markets

EUROPE

Thursday: Spanish CPI and Harmonized Index of Consumer Prices, Eurozone GDP, Industrial Production, Employment Change, ECB Monetary Policy Meeting Accounts, and speeches by ECB’s President Christine Lagarde, Vice President Luis De Guindos, and Executive Board Member Isabel Schnabel.

Friday: French CPI, Italian CPI, and speeches by ECB Chief Economist Philip Lane, and Executive Board Member Piero Cipollone.

Monday: German Buba Monthly Report and G20 Meeting.

Tuesday: Eurozone Harmonized Index of Consumer Prices and Core Harmonized Index of Consumer Prices.

Wednesday: German PPI and EU Financial Stability Review.

UK

Thursday: Speeches by BoE Governor Bailey and Monetary Policy Committee member Catherine Mann.

Friday: GDP, Industrial Production, and Manufacturing Production.

Wednesday: CPI, Core CPI, PPI, Core PPI, Retail Price Index and BoE Deputy Governor Ramsden.

US

Thursday: Initial and Continuing Jobless Claims, PPI, and speeches by Fed Chair Powell, Board Member Adriana Kugler, and New York Fed President John Williams.

Friday: Retail Sales, NY Empire State Manufacturing Index, and speeches by Boston Fed President Susan Collins, and New York Fed President John Williams.

Monday: A speech by Chicago Fed President Austan Golsbee.

Tuesday: Building Permits and Housing Starts.

JAPAN

Thursday: GDP.

Tuesday: Exports, Imports and Trade Balance.

CHINA

Friday: Industrial Production, and Retail Sales.

Tuesday: PBoC Interest Rate Decision.

GLOBAL

Monday and Tuesday: G20 meeting, Rio de Janiero, Brazil.

Global Macro Updates

Steady as she goes: US inflation meets forecasts, disinflation continues. The October Consumer Price Index (CPI) report aligned with expectations for both headline and core inflation, with annualised rates also meeting forecasts. Core goods prices remained unchanged m/o/m, while core services prices rose by a moderate 0.3%, representing a deceleration from the 0.4% increase observed in the previous month.

However, shelter costs continued to exert upward pressure on inflation, with the shelter index rising 0.4% m/o/m and accounting for over half of the monthly increase in the all-items index. Airfares and used car prices also contributed to price firmness, with airfares climbing 3.2% m/o/m (matching the previous month's increase) and used car prices surging 2.7%. Analysts had previously indicated the possibility of higher used vehicle prices due to the impact of recent hurricanes. Conversely, apparel prices fell 1.5% m/o/m, offsetting September's 1.1% rise. However, analysts suggest this decline in apparel prices is unlikely to persist.

Ultimately, the October CPI report provided little evidence of inflation reaccelerating, although the pace of disinflation has slowed.

Fedspeak offers diverging perspectives, from patience to confidence. Federal Reserve officials expressed a cautious tone in their this week, emphasising the need for prudence in future monetary policy decisions.

Dallas Fed President Lorie Logan, in her remarks at the ninth joint energy conference hosted by the Federal Reserve Banks of Dallas and Kansas City, acknowledged the progress made in reducing inflation, but said that the Fed should proceed cautiously. While she indicated that further interest rate cuts are likely necessary, she emphasised that the number and timing of such cuts remain uncertain.

St. Louis Fed President Alberto Musalem, at an Economic Club of Memphis event in Tennessee, stated that monetary policy should remain moderately restrictive as long as inflation persists above the 2% target. He advocated for a "judicious and patient" approach to policy adjustments as the Fed evaluates incoming economic data and cautioned against the risks of re-accelerating inflation if interest rates decline too rapidly.

Kansas City Fed President Jeffrey Schmid echoed this sentiment. He noted that while policymakers have greater confidence in the downward trajectory of inflation, the extent of future interest rate reductions and the eventual equilibrium level of rates remain to be determined.

In contrast, Minneapolis Fed President Neel Kashkari expressed greater optimism, stating in an interview with Bloomberg that he is confident in the inflation outlook and does not believe inflation is entrenched above the 2% target.

Negative German Bund-swap spreads: growth concerns and rising supply weigh on market. A notable shift has occurred in the German bond market, with yields on German Bunds recently falling below corresponding swap rates. This has resulted in the unusual phenomenon of negative 10-year swap spreads, as reported by GlobalCapital. Analysts interpret this development as a potential signal of changing supply-demand dynamics for Bunds, likely reflecting growing market concerns about potential headwinds to economic growth and an anticipated increase in German government bond issuance.

Expectations of elevated government spending on defence, energy support measures, and fiscal stimulus aimed at bolstering the slowing German economy, combined with the ECB’s ongoing quantitative tightening, are anticipated to drive higher Bund issuance. This increase in supply is occurring against the backdrop of a shifting supply-demand balance already underway due to the ECB's withdrawal of liquidity from the market, as reported by Reuters.

While negative swap spreads are more frequently observed in other markets, such as the US, this occurrence is relatively uncommon in Germany.

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

This article is provided to you for informational purposes only and should not be regarded as an offer or solicitation of an offer to buy or sell any investments or related services that may be referenced here.