Global market indices

Currencies

Cryptocurrencies

Fixed Income

Commodity sector news

Key data to move markets

Global macro updates

Global market indices

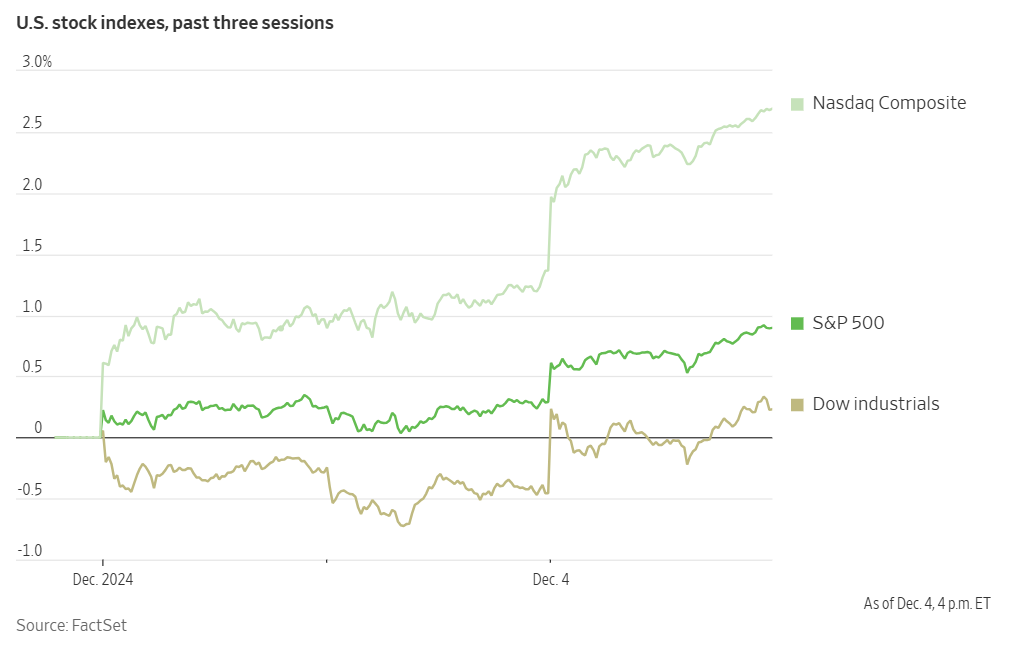

US Stock Indices Price Performance

Nasdaq 100 +1.43% MTD +26.17% YTD

Dow Jones Industrial Average -0.46% MTD +18.62% YTD

NYSE -0.41% MTD +19.79% YTD

S&P 500 +0.90% MTD +27.60% YTD

The S&P 500 is +1.46% over the past week, with 3 of the 11 sectors up MTD. The Equally Weighted version of the S&P 500 is -0.43% this week, its performance is -0.71% MTD and +17.70% YTD.

The S&P 500 Information Technology sector is the leading sector so far this month, up +3.39% MTD and +38.74% YTD, while Energy is the weakest at -3.35% MTD and +9.33% YTD.

This week, Information Technology outperformed within the S&P 500 at +4.43%, followed by Communication Services and Consumer Discretionary at +3.57% and +3.54%, respectively. Conversely, Energy underperformed at -3.03%, followed by Utilities and Real Estate, at -2.97% and -2.85%, respectively.

All three major US stock indices reached record highs on Wednesday. This achievement marked the seventh occasion this year that the Dow, S&P 500, and Nasdaq Composite have simultaneously reached all-time highs. The Dow Jones Industrial Average surpassed the 45,000 threshold for the first time in its history, a milestone that seemed improbable just over two years ago. The S&P 500 advanced +0.6% to close at 6,086.49, while the Dow Jones Industrial Average rose +0.7% to end at 45,014.04. The technology-focused Nasdaq Composite exhibited the strongest gains, climbing +1.3% to finish at 19,735.12.

This upward momentum in equity markets could potentially persist, as December has historically been a favourable month for seasonal market trends. An analysis of monthly returns since 1950 reveals that December frequently delivers the highest proportion of positive returns, at approximately 74%.

While investors are optimistic about the prospects for a "Santa Claus rally," a degree of caution may be warranted following November's robust market performance.

In corporate news, Dollar Tree reported improved sales for Q3, indicating that the discount retailer is effectively navigating competitive pressures and attracting increased customer traffic.

Conversely, Foot Locker lowered its full-year sales and profit projections, citing heightened promotional activity and a deceleration in consumer spending in advance of the critical holiday shopping season.

JetBlue Airways raised its earnings guidance for Q4, attributing the upward revision to stronger-than-expected bookings in November and December, coupled with reduced operating costs, partially driven by declining fuel prices.

US stocks

Mega caps: The Magnificent Seven had a strong performance this week, with all members in positive territory. Alphabet +3.04%, Amazon +6.04%, Apple +3.44%, Meta Platforms +7.83%, Microsoft +3.41%, Nvidia +7.24%, and Tesla +7.52%.

Energy stocks faltered this week, as the Energy sector itself was -3.03% due to easing concerns regarding oil supply. WTI and Brent prices are slightly up this week, +1.26% and +0.24%, respectively. The Energy sector’s YTD performance is +9.33%. Over the week Energy Fuels +0.84%, BP +0.05%, while Shell -0.30%, Apa -1.42%, Hess -1.91%, Phillips 66 -2.06%, Chevron -2.34%, Baker Hughes -2.41%, Occidental Petroleum -2.82%, ExxonMobil -2.87%, Marathon Petroleum -3.19%, ConocoPhillips -3.61%, and Halliburton -4.02%.

Materials and Mining stocks had mixed performance this week, the Materials sector itself was -0.93%, bringing the sector’s YTD performance to +8.64%. Mosaic +3.85%, Yara International +3.26%, CF Industries +3.20%, Sibanye Stillwater +1.97%, while Newmont Corporation -1.50%, Freeport-McMoRan -1.65%, Nucor -3.53%, and Albemarle -4.97%.

European Stock Indices Price Performance

Stoxx 600 +1.41% MTD +8.03% YTD

DAX +3.09% MTD +20.78% YTD

CAC 40 +0.94% MTD -3.18% YTD

IBEX 35 +2.49% MTD +18.11% YTD

FTSE MIB +2.00% MTD +12.30% YTD

FTSE 100 +0.59% MTD +7.79% YTD

This week, the pan-European Stoxx Europe 600 index was +2.47%. It was +0.37% on Wednesday, closing at 517.45.

This month so far in the STOXX Europe 600, Travel & Leisure is the leading sector, +3.10% MTD and +9.74% YTD, while Autos & Parts is the weakest at -5.46% MTD and -16.81% YTD.

This week, Technology outperformed within the STOXX Europe 600 with a +6.62% gain, followed by Retail and Industrial Goods and Services at +6.49% and +4.50%, respectively. Conversely, Telecom underperformed at -0.11 %, followed by Utilities and Food and Beverages, -0.08% and -0.05%, respectively.

Germany's DAX index was +1.08% on Wednesday and closed at 20,232.14. It was +5.04% for the week. France's CAC 40 index was +0.66% on Wednesday, closing at 7,303.28. It was +2.24% for the week.

The UK's FTSE 100 index was +0.74% this week to 8,335.81. It was -0.28 % on Wednesday.

The European Retail sector demonstrated strong performance in Wednesday's trading. This positive momentum follows press reports indicating that the European Commission is considering the implementation of a new tax aimed at curbing the surge of goods sold on Chinese e-commerce platforms that circumvent customs duties and regulatory checks.

The Automotive and Parts sector also exhibited robust performance on Wednesday despite the surprise resignation of Stellantis CEO Carlos Tavares on Monday. Stellantis, the world’s fourth-largest carmaker, refuted a report published in the Corriere della Sera newspaper suggesting that the company planned to appoint outgoing Apple CFO Luca Maestri as its new Chief Executive Officer. In Germany, Volkswagen's CEO stated that a recent proposal put forth by labour unions falls significantly short of addressing the company's long-term strategic needs.

Technology sector stocks also trended higher. ASML confirmed that new US export regulations are consistent with the company's previous assumptions.

In contrast, the Healthcare sector emerged as the primary laggard in Wednesday's trading. Scancell Holdings announced that Genmab has exercised its option for a second commercial license agreement. Grifols shareholders, collectively representing 5.65% of Class A shares and 3.88% of Class B shares, expressed strong support for the company's decision to reject a takeover offer from Brookfield Asset Management. Novavax disclosed its intention to divest its manufacturing facility in the Czech Republic to Novo Nordisk for a total consideration of $200 million.

The Basic Resources sector underperformed on Wednesday, weighed down by declining base metals prices. The Food, Beverage, and Tobacco sector also experienced weakness. Davide Campari-Milano appointed industry veteran Simon Hunt as its new CEO. Equity analysts have characterised this appointment as a positive development for the company, given his extensive experience in the US market.

Other Global Stock Indices Price Performance

MSCI World Index +1.04% MTD +21.47% YTD

Hang Seng +1.64% MTD +15.81% YTD

This week, the Hang Seng Index was +0.71%, while the MSCI World Index was +1.68%.

Currencies

EUR -0.61% MTD -4.73% YTD to $1.0510.

GBP -0.30% MTD -0.27% YTD to $1.2703.

The euro was -0.54% against the USD over the past week, while the British pound was +0.19%. The Dollar Index was +0.13% this week, +0.54% MTD, and +4.91% YTD, settling at 106.36.

The euro edged slightly higher against the dollar on Wednesday, +0.02%, reaching $1.0510, after a coalition of far-right and left-wing lawmakers united to support a no-confidence motion against Prime Minister Michel Barnier and his government. The motion passed with a decisive majority of 331 votes.

The removal of Prime Minister Barnier is likely to exacerbate the ongoing political crisis within the eurozone's second-largest economy, potentially exerting further downward pressure on the euro. France is still facing budget uncertainty with the rejection of Barnier’s 2025 budget that included €60bn in tax increases and spending cuts to reduce France’s deficit, which will reach 6% of GDP this year, double the EU deficit ratio of 3%.

The US dollar index remained relatively flat at +0.01% on Wednesday to 106.36. Economic data released on Wednesday was slightly softer and so did not significantly alter market expectations for an interest rate cut later this month.

A report from ADP revealed that US private payrolls expanded at a moderate pace in November, albeit falling short of consensus forecasts. However, annual wages for employees who remained in their positions edged higher for the first time in 25 months. The ADP report indicated an increase of 146,000 private sector jobs in November, following a downwardly revised gain of 184,000 jobs in October.

Meanwhile, data from the Institute for Supply Management (ISM) indicated a deceleration in US services sector activity during November, following robust growth in the preceding months. The ISM's non-manufacturing purchasing managers' index declined to 52.1 last month, after reaching a peak of 56.0 in October, its highest level since August 2022.

The British pound experienced a slight appreciation against the US dollar on Wednesday, following remarks by BoE Governor Andrew Bailey, who indicated the likelihood of gradual interest rate reductions over the coming year. Governor Bailey also emphasised that the disinflationary trend was firmly established.

Initially, the pound weakened by as much as -0.33% to $1.2630 following Governor Bailey's comments at the Financial Times Global Boardroom event. However, it quickly recovered those losses and ultimately closed +0.24% higher at $1.2703.

The Financial Times reported that Governor Bailey anticipates four interest rate cuts by the BoE next year. He clarified that this projection aligned with market expectations at the time the BoE integrated them into its most recent economic forecasts.

When questioned about the likelihood of four rate cuts next year, Governor Bailey stated, "We always condition what we publish in terms of the projection on market rates, and so as you rightly say, that was effectively the view the market had - we emphasised in that report the word 'gradual'."

Currently, financial markets are pricing in three interest rate cuts by the BoE next year. The pound also strengthened modestly against the euro, with one euro trading at 82.82 pence.

In contrast, the US dollar appreciated against the Japanese yen, rising +0.61% to ¥150.52. This gain followed media reports that cast doubt on market expectations for an interest rate hike by the BoJ this month, leading to a decline in Japanese government bond yields.

Note: As of 5:15 pm EST 4 December 2024

Cryptocurrencies

Bitcoin +1.06% MTD +134.62% YTD to $98,336.00.

Ethereum +5.61% MTD +65.38% YTD to $3,846.75.

Crypto prices soared over 6.1% to over $100,000 late on Wednesday after President-elect Donald Trump selected the pro-crypto Paul Atkins to replace Gary Gensler at the US Securities and Exchange Commission.Bitcoin. Bitcoin has been surging since November on expectations that Donald Trump's election victory would create a more welcoming regulatory environment for cryptocurrencies. Bitcoin rose to an all-time high of $103,619 in early Asian trading today, up about 5% on the day and taking its year-to-date gains to almost 145%. Overall, the cryptocurrency market overall has jumped by about $1.3 trillion since Trump’s election victory or over 40%. The market cap for Bitcoin is now about $2 Trillion. Speaking yesterday at The New York Times DealBook Summit, Federal Reserve Chair Jerome Powell publicly called Bitcoin a competitor for gold due to the aspect of preserving the value of money rather than using it as a currency.

As noted by Bloomberg news, US Spot Bitcoin ETFs have attracted a net inflow of about $32 billion this year, including over $8 billion since Trump became president-elect, data compiled by Bloomberg show.

Note: As of 5:15 pm EST 4 December 2024

Fixed Income

US 10-year yield +0.6 bps MTD +30.0 bps YTD to 4.181%.

German 10-year yield -3.0 bps MTD +5.2 bps YTD to 2.061%.

UK 10-year yield +0.3 bps MTD +71.1 bps YTD to 4.250%.

US Treasury 10-year bond yields are -8.3 bps this week. US Treasury yields declined on Wednesday, reversing earlier gains. This shift was driven by softer economic data that counterbalanced recent comments from Fed officials. Market participants continue to anticipate a 25 bps interest rate cut at the Fed's December monetary policy meeting.

Initially, yields rose following remarks by St. Louis Fed President Alberto Musalem, who suggested that it could take up to two years for inflation to reach the central bank's target and that the pace of future policy actions has become less certain.

Fed Chair Jerome Powell also stated earlier on Wednesday that the US economy is demonstrating greater strength than initially assessed in September. This assessment may lead policymakers to adopt a more cautious approach to further interest rate reductions. Chair Powell's remarks are likely his final public comments before the commencement of the FOMC pre-meeting quiet period on Saturday, ahead of the 17th - 18th December policy meeting.

While Fed Governor Christopher Waller indicated on Monday that he was ‘leaning toward’ a rate cut, other FOMC members have refrained from expressing a definitive view on the outcome of the December meeting.

The yield on the 10-year US Treasury note decreased by -4.7 basis points to 4.181%. Similarly, the yield on the 2-year Treasury note, which is typically closely correlated with interest rate expectations, fell by -3.9 bps to 4.132%.

Treasury yields extended their declines following news that a coalition of far-right and left-wing lawmakers in France had successfully passed a no-confidence motion against Prime Minister Michel Barnier and his government. This political development has plunged the European Union's second-largest economy deeper into a political crisis.

Market focus is now directed toward the release of the November nonfarm payrolls report on Friday, followed by the consumer price index data next Wednesday.

According to CME's FedWatch tool, the probability of a 25 bps interest rate cut at the December FOMC meeting currently stands at 74.0%, from 66.5% a week ago.

Across the Atlantic, the German 10-year yield was -10.3 bps this week, while the UK 10-year yield was -4.7 bps this week. The spread between US 10-year Treasuries and German Bunds currently stands at 212.0 bps, 2 bps lower than last week.

Italian bond yields, a benchmark for the eurozone periphery, were -19.6 bps this week to 3.216%. Consequently, the spread between Italian and German 10-year yields is 115.5 bps, 9.3 bps narrower than last week.

French sovereign bonds experienced a period of relative calm on Wednesday as investors awaited the outcome of the no-confidence vote in the French parliament.

The broader fixed-income market relinquished some of the safe-haven gains accrued after South Korea briefly declared martial law on Tuesday, only to lift it within hours.

Market participants fully anticipate a 25 bps interest rate cut from the ECB at its upcoming meeting, with a roughly 27% probability assigned to a larger 50 bps reduction.

French 10-year government bond yields edged slightly lower by -1.2 bps to 2.890% on Wednesday. The yield premium over German 10-year debt also narrowed slightly to 82.9 basis points, representing a 1.3 bps decrease from the previous trading session, and 3.2 bps decrease from last week. This risk premium reached its highest level since the 2012 eurozone crisis last week, peaking at 90 bps.

German 10-year yields, which briefly touched a new two-month low on Tuesday, increased by +0.1 bps to 2.061%. On the shorter end of the curve, 2-year German yields rose by +1.0 bp to 1.955%.

French government bonds (OATs) have exhibited some stability this week, as market dynamics appear to be following a ‘buy the rumour, sell the fact’ pattern. French 5-year sovereign credit default swaps remained unchanged at 41 bps on Wednesday, according to data from S&P Global Market Intelligence. Data from LSEG indicates that this level represents the highest point since May 2020 and is double the level observed six months ago.

On the supply front, France is scheduled to conduct an auction of €5 billion in 2038, 2040, 2050, and 2072 OATs on Thursday. This auction could provide insights into investor appetite for French debt following Wednesday's no-confidence vote.

Italy's 10-year yield, a barometer for the eurozone periphery, declined by -3.4 bps to 3.216% on Wednesday.

Commodities

Gold spot -0.12% MTD +28.68% YTD to $2,649.68 per ounce.

Silver spot +2.59% MTD +32.50% YTD to $31.31 per ounce.

West Texas Intermediate crude +2.40% MTD -2.77% YTD to $68.76 a barrel.

Brent crude +0.79% MTD -6.01% YTD to $72.31 a barrel.

Gold prices are +0.44% this week. Gold prices experienced a modest increase on Wednesday following the release of data indicating moderate growth in US private payrolls for the previous month. Market participants also continued to assess recent remarks by Fed Chair Jerome Powell while anticipating the forthcoming non-farm payrolls report scheduled for release on Friday. Spot gold rose by +0.24%, reaching $2,649.68 per ounce on Wednesday.

The World Gold Council reported on Wednesday that central banks reported 60 tonnes of net purchases in October – the highest amount recorded YTD. The Reserve Bank of India (RBI) led the field, adding 27 tonnes of gold to its reserves, followed by Turkey and Poland, at 17 tonnes and 8 tonnes respectively. The National Bank of Kazakhstan recorded its first monthly net buying (4 tonnes) after five consecutive months of reducing gold holdings

Investor focus now turns to Friday's pivotal US employment report and next week's inflation data.

This week, WTI and Brent, +0.31% and -0.63%, respectively.

Oil prices experienced a decline exceeding 1.5 percentage points on Wednesday as market participants awaited the impending decision from OPEC+ regarding potential production cuts. However, the release of data from the Energy Information Administration (EIA) revealing a larger-than-anticipated drawdown in US crude oil inventories for the previous week provided some upward pressure on prices, mitigating the decline.

This downturn followed a significant rally in Brent crude on Tuesday, which registered its most substantial gain in two weeks with a 2.5% increase.

OPEC+ is expected to convene today to deliberate on production policy. It is widely anticipated that the group will elect to extend existing output cuts until the conclusion of Q1 2025. This decision aligns with OPEC+'s stated objective of gradually phasing out supply restrictions throughout the next year.

According to the EIA report, the decline in US crude oil inventories was driven by increased refinery activity. Conversely, gasoline and distillate stockpiles exhibited larger-than-expected builds during the same period.

EIA report: refinery activity drives decline in US crude inventories. In the week ending 29th November, the EIA reported a larger-than-anticipated decline in US crude oil inventories. This decrease, amounting to 5.1 million barrels, brought total stocks down to 423.4 million barrels. The drawdown was primarily attributed to increased refinery activity, which offset a concurrent rise in crude imports.

Despite the overall decline in crude stocks, inventories at the Cushing, Oklahoma delivery hub experienced a modest increase of 50,000 barrels. Notably, US crude oil production reached a new record high of 13.513 million barrels per day (bpd). This surge in production was accompanied by a significant increase in refinery crude runs, which rose by 615,000 bpd to reach their highest level since 12th July. Consequently, refinery utilization rates climbed 2.8 percentage points to 93.3%.

While net US crude imports increased by 1.64 million bpd, exports declined by 428,000 bpd to 4.24 million bpd. Of particular note was the increase in crude imports from Iraq, which reached 397,000 bpd, marking the highest level since June 2023.

In contrast to the decline in crude oil inventories, US gasoline stocks rose by 2.4 million barrels, reaching 214.6 million barrels. The EIA data also indicated an increase in gasoline supplied, a proxy for demand, which rose by 231,000 bpd to 8.74 million bpd. Furthermore, the four-week average for total product demand demonstrated robust growth, exceeding last year's levels by approximately 4% at 20.45 million bpd.

Finally, the EIA report showed a build in distillate stockpiles, which encompass diesel and heating oil. These inventories increased by 3.4 million barrels to 118.1 million barrels.

Note: As of 5:15 pm EST 4 December 2024

Key data to move markets

EUROPE

Thursday: Eurozone Retail Sales and German Factory Orders.

Friday: German Industrial Production, Eurozone GDP, and Employment Change.

Monday: Eurozone Sentix Investor Confidence.

Tuesday: German Harmonized Index of Consumer Prices and Eurogroup Meeting.

UK

Thursday: A speech by Monetary Policy Committee member Megan Greene.

Monday: A speech by BoE Deputy Governor Dave Ramsden.

US

Thursday: Initial and Continuing Jobless Claims.

Speeches by Chicago Fed President Austan Golsbee, Cleveland Fed President Beth Hammack, Kansas City Fed President Jeffrey Schmid, and Board Member Michael Barr.

Friday: Average Hourly Earnings, Nonfarm Payrolls, Unemployment Rate, Michigan Consumer Sentiment Index, UoM 5-year Consumer Inflation Expectation, speeches by Fed Board Member Michelle Bowman, Chicago Fed President Austan Golsbee, San Francisco Fed President Mary Daly, and Cleveland Fed President Beth Hammack.

Tuesday: Nonfarm Productivity and Unit Labor Costs.

Wednesday: CPI and Core CPI.

JAPAN

Sunday: GDP.

CHINA

Sunday: CPI.

Monday: Exports, Imports, and Trade Balance.

GLOBAL

Thursday: OPEC+ meeting.

Global Macro Updates

China retaliates against US chip restrictions and S&P revises growth projections. The Chinese Commerce Ministry has announced heightened export controls on dual-use products to the US, effectively prohibiting the shipment of key materials such as gallium, germanium, antimony, and superhard materials. The Financial Times (FT) notes that this action represents a swift retaliation by Beijing in response to recent export control measures imposed by Washington.

Several Chinese industry associations, including those representing the semiconductor and automotive sectors, have jointly expressed strong opposition to these restrictions and urged domestic firms to exercise caution when procuring US-manufactured chips, according to the Chinese news agency, Xinhua. The China Semiconductor Industry Association asserted that the US government's arbitrary control measures have disrupted supply chains and increased operating costs for American companies. These actions, the association argues, have compromised the stable supply of US chips, rendering them less secure and reliable.

The FT highlights that the embargoed materials are crucial components in the production of semiconductors, batteries, communications equipment, and military hardware. This latest ban signals that President Xi Jinping's administration is prepared to target Western economic interests, a departure from its previous restrained approach aimed at mitigating the pace of decoupling.

Although China's stimulus measures are expected to provide some support for economic growth, the US trade tariffs on Chinese exports are expected to have a negative impact. Consequently, S&P revised its GDP growth projections for China to 4.1% in 2025 and 3.8% in 2026. These forecasts represent a 0.2 percentage point and 0.7 percentage point reduction, respectively, compared to its previous estimates in September.

Economic growth in the Asia-Pacific region will be constrained by weaker global demand and the effects of US trade policy. However, lower interest rates and subdued inflationary pressures should help to mitigate the adverse impact on consumer spending power. In EM within the region, robust domestic demand growth is providing a key support for GDP growth.

Fluctuations in capital flows, driven by shifting expectations regarding US interest rates and trade policies, necessitate vigilance and caution from central banks in the Asia-Pacific region. S&P anticipates that these central banks will adopt a gradual approach to reducing policy interest rates.

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

Ця стаття надається вам лише для інформаційних цілей і не повинна розглядатися як пропозиція або запит на купівлю або продаж будь-яких інвестицій або пов'язаних послуг, які можуть бути згадані тут. Торгівля фінансовими інструментами пов'язана зі значним ризиком втрат і може підходити не всім інвесторам. Минулі результати не є надійним показником майбутньої ефективності.