Corporate Earnings News

Corporate earning calendar 6 February - 12 February 2025

Thursday: Amazon, Eli Lilly, AstraZeneca, Philip Morris International, L’Oreal, Hilton Worldwide, Suncor Energy, Equifax, Hershey, Kellanova, Expedia, Ralph Lauren, Blue Owl Capital.

Friday: Ubiquiti, CBOE Global, Kimco Realty.

Monday: McDonald’s, Vertex, ON Semiconductor, Loews, Credicorp.

Tuesday:Coca-Cola, Shopify, S&P Global, Gilead Sciences, BP, Marriott International, AIG, Humana, Zillow, Carlyle Group, Super Micro Computer.

Wednesday: Cisco, CME Group, CVS Health, Dominion Energy, Crown Castle, Heineken, Reddit, Kraft Heinz, Sun Life Financial, Martin Marietta Materials, Global Payments, Smurfit Westrock, Paramount Global, Albemarle.

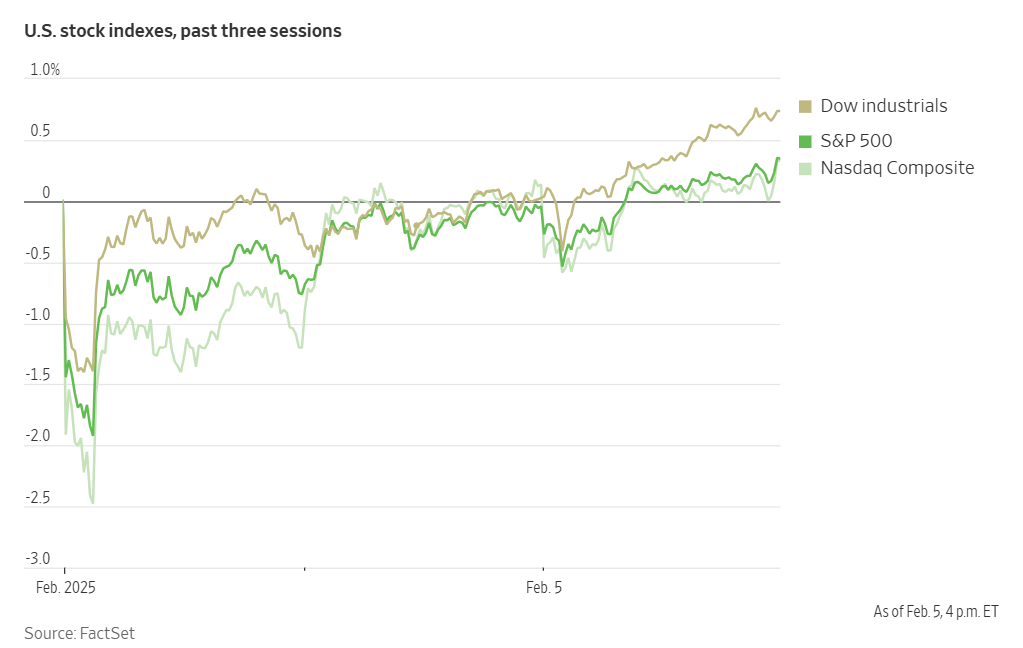

Global market indices

US Stock Indices Price Performance

Nasdaq 100 +0.27% MTD and +2.64% YTD

Dow Jones Industrial Average +0.03% MTD and +4.73% YTD

NYSE +0.65% MTD and +5.40% YTD

S&P 500 +0.35% MTD and +3.06% YTD

The S&P 500 is +0.37% over the past week, with 8 of the 11 sectors up MTD. The Equally Weighted version of the S&P 500 is +0.25% this week. Its performance is flat MTD and +3.40% YTD.

The S&P 500 Energy sector is the leading sector so far this month, up +2.71% MTD and +4.77% YTD, while Consumer Discretionary is the weakest at -1.52% MTD and +2.80% YTD.

This week, Real Estate outperformed within the S&P 500 at +2.53%, followed by Utilities and Health Care at +2.12% and +1.96%, respectively. Conversely, Consumer Discretionary underperformed at -0.83%, followed by Industrials and Consumer Staples, at -0.46% and +0.25%, respectively.

Overall market performance was up on Wednesday. The S&P 500 was +0.4%, while the Nasdaq Composite was +0.2%. The Dow Jones Industrial Average +0.7% and the Russell 2000 was +1.2%.

According to LSEG I/B/E/S data, 2024 Q4 y/o/y earnings are expected to be 12.2%. Excluding the Energy sector, the y/o/ earnings estimate is 15.5%. Of the 244 companies in the S&P 500 that have reported earnings to date for 2024 Q4, 77.0% reported above analyst expectations. This compares to a long-term average of 67%. The 2024 Q4 y/o/y blended revenue growth estimate is 4.7%. If the Energy sector is excluded, the growth rate for the index is 5.3%.

Mega caps: The Magnificent Seven had mostly negative performance this week with Meta Platforms +4.20%, and Nvidia +0.14%, in positive territory, while Amazon -0.38%, Alphabet -2.09%, Tesla -2.81%, Apple -2.88%, and Microsoft -6.57%.

Energy stocks were mixed this week, although the Energy sector itself was +0.43% due to fears of a renewed China-US trade war stirred concerns over slower economic growth. WTI and Brent prices are down this week, -2.36% and -2.92%, respectively. Over the week Baker Hughes +13.42%, Marathon Petroleum +3.91%, Shell +1.93%, BP +1.81%, ExxonMobil +1.11%, Phillips 66 +0.95%, while Halliburton -0.30%, ConocoPhillips -1.23%, Hess -1.67%, Chevron -1.73%, Occidental Petroleum -3.01%, Apa -4.27%, and Energy Fuels -5.59%.

Materials and Mining stocks had an uneven performance this week, with the Materials sector +0.57%. Sibanye Stillwater +11.22%, Newmont Corporation +8.10%, Nucor +5.01%, and Freeport-McMoRan +1.10%, while Yara International -1.12%, CF Industries -2.73%, Mosaic -3.07%, and Albemarle -7.42%.

European Stock Indices Price Performance

Stoxx 600 -0.18% MTD and +6.10% YTD

DAX -0.67% MTD and +8.42% YTD

CAC 40 -0.74% MTD and +6.92% YTD

IBEX 35 +1.36% MTD and +8.12% YTD

FTSE MIB +0.68% MTD and +7.41% YTD

FTSE 100 -0.58% MTD and +5.51% YTD

This week, the pan-European Stoxx Europe 600 index was +0.80%. It was +0.47% on Wednesday, closing at 538.56.

So far this month in the STOXX Europe 600, Health Care is the leading sector, +1.14% MTD and +7.45% YTD, while Food & Beverages is the weakest at -2.30% MTD and -1.48% YTD.

This week, Technology outperformed within the STOXX Europe 600 with a +3.15% gain, followed by Oil & Gas and Utilities at +2.59% and +2.44%, respectively. Conversely, Food & Beverages underperformed at -2.26%, followed by Chemicals and Autos & Parts, at -1.27% and -0.62%, respectively.

Germany's DAX index was +0.37% on Wednesday, closing at 21,585.93. It was -0.24% for the week. France's CAC 40 index was -0.19% on Wednesday, closing at 7,891.68. It was +0.24% for the week.

The UK's FTSE 100 index was +0.77% this week to 8,623.29. It was +0.61% on Wednesday.

On Wednesday, the Healthcare sector in the Stoxx Europe 600 index emerged as the top performer, fueled by robust earnings from major pharmaceutical companies. GSK exceeded Q4 EPS expectations, announced a £2 billion share buyback program, and raised its 2031 sales target. Novo Nordisk also surpassed Q4 EPS estimates and increased dividends by 21%, driven by doubling sales for its blockbuster obesity drug Wegovy.

Banks also experienced gains, bolstered by strong financial results from Banco Santander, whose Q4 net income beat forecasts, and DNB Bank, which reported much stronger Q4 net income. Credit Agricole increased dividends after its Q4 earnings topped estimates, propelled by growth in asset gathering and its corporate centre, despite underperformance in Retail banking.

In contrast, the Autos and Parts sector faced the steepest declines due to ongoing concerns about potential tariffs on trading partners, even with a temporary pause in place. Renault came under pressure following reports that Japan's Nissan would abandon merger talks with rival Honda. It is being reported that early this morning in Asia, Nissan chief executive Makoto Uchida told his Honda counterpart, Toshihiro Mibe, of the board’s intention to disband merger talks that would have created the world’s fourth-largest carmaker.

The Industrial Goods and Services sector lagged behind as Alfa Laval missed Q4 EPS estimates despite raising dividends, while Wartsila Oyj exceeded Q4 EPS expectations. In the Technology sector, Nordic Semiconductor reported Q4 sales above expectations and projected Q1 sales ahead of consensus, citing orders from individual customers offsetting seasonal slowdown.

Other Global Stock Indices Price Performance

MSCI World Index -0.27% MTD and +3.20% YTD

Hang Seng +1.84% MTD and +2.68% YTD

This week, the Hang Seng Index was +1.84%, while the MSCI World Index was -0.05%.

Currencies

The euro was -0.17% against the USD over the past week, while the British pound was +0.43% against the dollar. The Dollar Index is -0.21% so far this week, -0.69% MTD and -0.80% YTD.

The US dollar weakened to a more than one-week low on Wednesday as investor concerns regarding a global trade war subsided. Concurrently, the Japanese yen strengthened following robust wage data.

The dollar index was -0.35%, reaching 107.62, after earlier touching its lowest point since 27th January at 107.29. Following the US President's indication of potential 25% import tariffs on Mexico and Canada, the dollar index surged by +1.3% to 109.88 on Monday. However, after Mexico and Canada secured a one-month reprieve by enhancing border security measures (despite increased US levies on China), the dollar index subsequently fell by approximately 2%.

The euro was +0.24% to $1.0403 on Wednesday, having previously fallen by as much as 2.3% on Monday due to anxieties about the global ramifications of tariffs and the possibility of their extension to the EU.

The dollar experienced its most significant decline on Wednesday against the yen, which was bolstered by positive Japanese wage data and remarks from a BoJ official suggesting the potential for further interest rate increases. The US currency was -1.16% to ¥152.57, its lowest level since December.

Data revealed that Japan's December inflation-adjusted real wages increased by 0.6% y/o/y, driven by a winter bonus surge. This data led traders to increase their bets on additional BoJ rate hikes this year, with just over 30 bps priced in by year-end.

The dollar's decline against the yen was further amplified by data indicating an unexpected slowdown in US services sector activity during January, attributed to moderating demand. The Institute for Supply Management (ISM) reported that its non-manufacturing purchasing managers index (PMI) decreased to 52.8 last month from 54.0 in December.

Sterling strengthened during afternoon trading on Wednesday as the dollar continued its retreat following its surge earlier in the week due to the threat of broad US tariffs. The focus in UK markets shifted to the BoE's interest rate decision today. Sterling rose to $1.2532 in London morning trade, its highest point since 7th January, and subsequently traded up +0.18% at $1.2502. The euro remained stable at 83.11 pence.

The BoE has cut rates by an additional 25 bp today as expected to 4.5%. It was the third cut in just over half a year. The Bank lowered its growth forecast to just 0.75% this year. It struck a cautious note about the pace of future rate reductions, as it projects that inflation will reaccelerate in the coming months.

The pound has lost ground against the dollar and euro this year, as markets have priced in further BoE rate cuts due to slowing growth. Money market pricing indicated that traders expect around 84 bps of easing from the BoE this year. The Bank began reducing its main rate from 5.25% in August.

Note: As of 5:00 pm EST 5 February 2025

Cryptocurrencies

Bitcoin is -6.89% and Ethereum -11.97% over the past week. Crypto prices have been hit not only by expectations that the Fed will keep rates on hold for longer. However, institutional investor interest continues to remain solid with BlackRock's iShares Bitcoin Trust and Fidelity Wise Origin Bitcoin Fund seeing another week of inflows, as investors doubled the amount of money they are putting into Spot Bitcoin ETFs. These collectively saw $1.1 billion in the five trading days ending Tuesday, soaring from the previous five-day period's $515.9 million, according to etf.com data. This surge came in the run up to BlackRock, the world’s largest asset manager, announcing on Wednesday that it’s preparing to list a Bitcoin ETF in Europe following on from the success of its $58 billion US ETF tracking the cryptocurrency. As noted by Bloomberg news, the European market for cryptocurrency ETPs is hotly contested, with more than 160 products available tracking the price of Bitcoin, Ether and other tokens. However, its $17.3 billion size pales in comparison to that of the US.

Note: As of 5:00 pm EST 5 February 2025

Fixed Income

US 10-year yield -12.02 bps MTD and -14.4 bps YTD to 4.428%

German 10-year yield -11.60 bps MTD and -0.70 bps YTD to 2.347%.

UK 10-year yield -11 bps MTD and -14 bps YTD to 4.423%.

US Treasury 10-year bond yields are -12.25 bps over the past week.

On Wednesday yields retreated with the 10-year Treasury note -8 bps to 4.428% on news that the US Treasury was not going to be increasing its debt issuance. Yields on the 30-year Treasury bond rose +1.4 bps to 4.817%. At the shorter end of the yield curve, the two-year yield, sensitive to Fed policy expectations, fell -2 bps to 4.291%.

The US Treasury stated on Wednesday that it expects to keep its coupon and floating rate note auction sizes steady, but will continue to incrementally increase the size of its Treasury Inflation-Protected Securities (TIPS) auctions. The Treasury said it will increase the 10-year TIPS reopening in March by $1 billion to $18 billion and increase the five-year TIPS new issue auction in April to $25 billion.

The US Treasury stated that it plans to sell $125 billion in its quarterly refunding next week, which will raise $18.8 billion in new cash and refund $106.2 billion in securities. This will include $58 billion in three-year notes, $42 billion in 10-year notes and $25 billion in 30-year bonds.

Across the Atlantic, the German 10-year yield was -15.90bps over the past week, while the UK 10-year yield was -11.80 bps over the past 7 days. The spread between US 10-year Treasuries and German Bunds currently stands at 206.7 bps, 10.6 bps wider than last week.

Italian bond yields, a benchmark for the eurozone periphery, were -20.4 bps this week to 3.450%. Consequently, the spread between Italian and German 10-year yields is 108.5 bps, 1.4bps wider than last week.

French 10-year government bond yields are down -13.0 bps to 3.082%. The yield premium over German 10-year yields is 71.7 bps.

Germany's 10-year bond yield -6 bps to 2.347% on Wednesday. The yield on Germany's two-year bond, which is particularly sensitive to ECB rate expectations, -5 bps to 2.06%.

ECB Chief Economist Philip Lane said on Wednesday that the ECB should ease policy at a measured pace to balance the risk of needlessly depressing growth and fuelling excessive inflation. He said inflation risks are in both directions. Speaking in Washington at the Peterson Institute for International Economics, he said that “a robust monetary-policy approach should balance the risks of moving too slowly against the risks of moving too quickly.” He stated “that a middle path is appropriate, which neither over-weighs upside risk nor over-weighs downside risk.” The ECB cut rates by 25 bps last week and is expected to cut them again in March despite inflation rising to 2.5% in January from December’s 2.4%.

Commodities

Gold spot +2.10% MTD and +9.22% YTD to $2,867.49 per ounce.

Silver spot +1.57% MTD and +12.06% YTD to $32.32 per ounce.

West Texas Intermediate crude -0.19% MTD and +0.36% YTD to $71.19 a barrel.

Brent crude -1.30% MTD and +0.07% YTD to $74.69 a barrel.

Gold prices are +4.07% this week after hitting their highest level on Tuesday.

Gold prices extended their record-breaking rally on Wednesday, driven by investor demand for the safe-haven asset amidst growing anxieties surrounding the US-China trade dispute and its potential repercussions for economic expansion.

Spot gold advanced by +0.90% to $2,867.49 per ounce, having earlier reached a record peak of $2,882.16 during the trading session. US gold futures concluded the day with a 0.6% increase, settling at $2,893 per ounce.

Market participants are now focused on the US nonfarm payrolls report scheduled for release on Friday for insights into the future direction of interest rates.

This week, WTI and Brent are -2.36% and -2.92%, respectively. Oil prices experienced a decline of over 1% on Wednesday, influenced by a substantial increase in US crude oil and gasoline inventories, indicative of diminished demand. Furthermore, renewed apprehensions regarding a potential trade conflict between the US and China contributed to concerns about dampened economic growth.

Brent crude futures settled at $74.69 per barrel, a decrease of $1.36, or -1.79%. US West Texas Intermediate crude closed at $71.19 per barrel, down $1.40, or -1.93%.

The prospect of a renewed trade dispute between the US and China, the world's largest energy consumer, placed downward pressure on prices. China's recent announcement of tariffs on US oil, liquefied natural gas, and coal imports, in response to US levies on Chinese exports, had already driven WTI down 3% to its lowest point since 31st December during Tuesday's trading session.

Adding to market uncertainty, Iranian President Masoud Pezeshkian called for OPEC members to unite against potential US sanctions. This appeal followed the US President's stated intention to reinstate the ‘maximum pressure’ campaign on Iran, a policy implemented during his first term. That prior administration's actions under President Trump had effectively reduced Iran's oil exports to near zero through sanctions aimed at curbing the nation's nuclear programme.

The potential reimposition of these sanctions could create a supply constraint, potentially bolstering oil prices, especially given the slower-than-anticipated supply adjustments from OPEC+ producers. EIA estimates indicate that Tehran's oil exports generated $53 billion in revenue in 2023 and $54 billion the previous year. OPEC data shows Iran's 2024 oil output has reached its highest level since 2018.

The current oil market is therefore navigating a complex landscape, balancing the escalating risk of a trade war negatively impacting global oil demand growth against the possibility of a sudden disruption in Iranian oil exports.

Note: As of 5:15 pm EST 5 February 2025

Key data to move markets

EUROPE

Thursday: Eurozone Retail Sales, German Factory Orders, and a speech by Bundesbank President Joachim Nagel.

Friday: German Industrial Production, and Trade Balance, and a speech by ECB’s Vice President Luis de Guindos.

Monday: Sentix Investor Confidence survey.

UK

Thursday: BoE Interest Rate Decision, BoE Minutes, BoE Monetary Policy Report, and a speech by BoE Governor Andrew Bailey.

Friday: A speech by Chief Economist Huw Pill.

Tuesday: Speeches by BoE Governor Andrew Bailey, and BoE External Member Catherine Mann.

Wednesday: A speech by BoE Monetary Policy Committee Member Megan Greene.

US

Thursday: Initial and Continuing Jobless Claims, Nonfarm Productivity, Unit Labor Costs, and speeches by Fed Governor Christopher Waller, and San Francisco Fed President Mary Daly.

Friday: Average Hourly Earnings, Average Weekly Hours, Nonfarm Payrolls, U6 Underemployment, Unemployment Rate, and speeches by Fed Governors Michelle Bowman and Adriana Kugler.

Tuesday: A speech by New York Fed President John Williams.

Wednesday: Consumer Price Index (CPI), Core CPI, and a speech by Atlanta Fed President Raphael Bostic.

JAPAN

Sunday: Current Account, and Trade Balance.

Monday: National Foundation Day.

CHINA

Saturday: CPI, and PPI.

Global Macro Updates

The tariff war begins with Trump’s first salvos. US President Donald Trump fired his opening trade salvos against Canada, Mexico and China earlier this week, creating 72 hours of market confusion. The 25% tariffs due to be imposed on Canada and Mexico are now under review for 30 days following the respective leaders, Canadian Prime Minister Justin Trudeau and Mexican President Claudia Sheinbaum, capitulating to some of President Trump’s demands. Each agreed to adding 10,000 border guards to cut down on illegal migration to the US and to clamp down on fentanyl trafficking. However, President Trump has yet to reach an agreement with China after imposing an additional 10% tariff on existing levies on Chinese products. Beijing announced it was imposing retaliatory tariffs on some American products, including 15% on coal and liquefied natural gas and 10% on crude oil and agricultural machinery. It also filed a complaint against the USA with the World Trade Organisation (WTO). Although Trump has suggested that he will be targeting the EU as well due to the large trade imbalance, there have been no announcements. Tariffs against the EU would put pressure on an already ailing euro area economy. Although Trump’s stated objective is to secure deals to halt the flow of drugs and unauthorised immigration, it now appears more that tariffs will now be an instrument to re-secure US global dominance. It is clear that the trade barriers suggested could destabilise global markets, drive up prices for American consumers, and potentially lower both US and global growth. However, as noted by Carla Norloff, a senior fellow at the Atlantic Council, this plan to tether countries to the US and re-assert US hegemony, could backfire, pushing them towards alternative suppliers and weakening the US’ long-term economic influence. This is a very long-term view and may prove to be extremely difficult to implement given the high degree of integration between US, Mexican, Canadian, and Chinese supply chains.

The service sector leads the eurozone PMI's January rebound into growth. Eurozone business activity rebounded into expansion territory in January 2025, the first growth since August 2024, driven primarily by the resilient services sector. The HCOB composite PMI edged up to 50.2 from 49.6, narrowly surpassing the critical 50-point threshold separating growth from contraction. While the services PMI, at 51.3, was slightly below the expected 51.4 and December's 51.6, it still demonstrated strength and helped counterbalance ongoing weakness in manufacturing. Service providers, responding to increased demand, accelerated hiring, and new orders saw modest but accelerating growth. However, headwinds remain, as business expectations dipped slightly, with the expectations index falling to 58.5 from 58.8. Political uncertainties, including upcoming German elections and French government instability, are reportedly weighing on sentiment. Cost pressures intensified across the Eurozone, with the composite input prices index reaching a near two-year high of 58.5. This persistent inflation within the services sector likely contributed to the ECB's cautious approach to monetary policy easing.

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

Dieser Artikel wird Ihnen lediglich zu Informationszwecken zur Verfügung gestellt und er sollte nicht als Angebot oder Aufforderung zur Abgabe eines Kauf- oder Verkaufsangebots eines Investments oder einer damit zusammenhängenden Dienstleistung betrachtet werden, auf die hier möglicherweise Bezug genommen wurde. Der Handel mit Finanzprodukten birgt erhebliche Verlustrisiken und ist möglicherweise nicht für alle Anleger geeignet. Die Wertentwicklung in der Vergangenheit ist kein verlässlicher Indikator für die künftige Wertentwicklung.