Global market indices

US Stock Indices Price Performance

Nasdaq 100 +1.77% MTD and +3.37% YTD

Dow Jones Industrial Average -0.13% MTD and -0.77% YTD

NYSE +0.59% MTD and +4.21% YTD

S&P 500 +1.17% MTD and +1.69% YTD

The S&P 500 is -0.69% over the past week, with 5 of the 11 sectors up MTD. The Equally Weighted version of the S&P 500 is -1.01% over this past week and +0.93% YTD.

The S&P 500 Energy is the leading sector so far this month, +8.07% MTD and +2.21% YTD, while Consumer Staples is the weakest sector at -3.54% MTD and +3.66% YTD.

Over this past week, Energy outperformed within the S&P 500 at +2.19%, followed by Information Technology and Utilities at +0.65% and -0.44%, respectively. Conversely, Health Care underperformed at -1.94%, followed by Consumer Discretionary and Consumer Staples at -1.69% and -1.55%, respectively.

The equal-weight version of the S&P 500 was +0.04% on Wednesday, outperforming its cap-weighted counterpart by 0.07 percentage points.

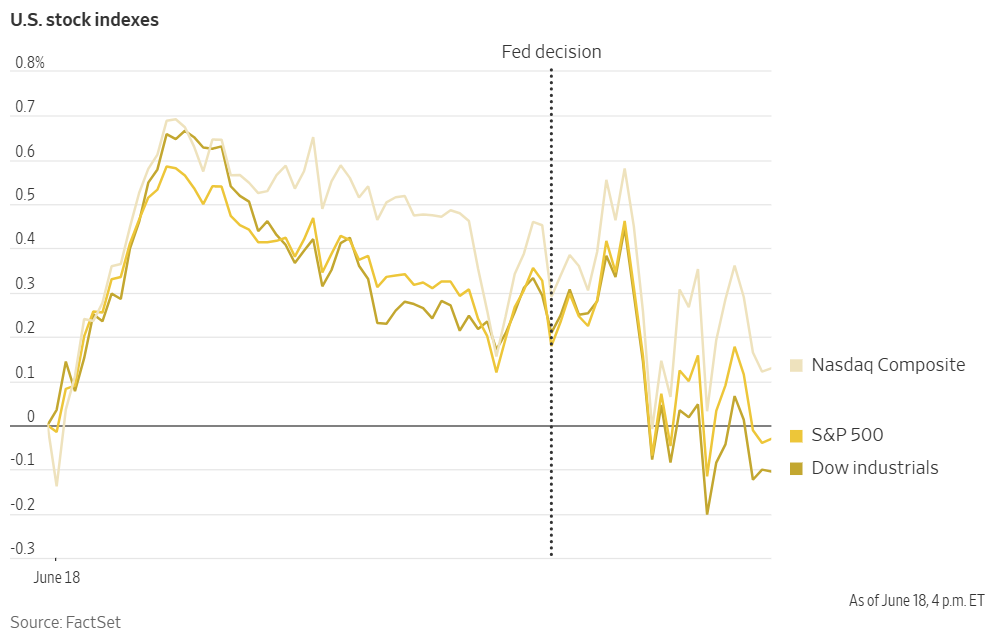

US equities closed slightly lower on Wednesday after paring earlier gains as remarks from Fed Chair Jerome Powell influenced market sentiment. The S&P 500 ended the session just below the 6,000 threshold after briefly surpassing it during trading. It declined by -0.03%, while the Dow Jones Industrial Average fell by 44 points or -0.10% and the Nasdaq 100 was unchanged from the previous day.

In corporate news, leading US bank regulators are reportedly planning to reduce a critical capital buffer by up to 1.5 percentage points for the nation's largest financial institutions. This prospective adjustment addresses concerns that the existing buffer has unduly constrained their trading activities within the Treasury market. Discussions among the Federal Reserve, Federal Deposit Insurance Corporation (FDIC), and the Office of the Comptroller of the Currency (OCC) are focused on the enhanced supplementary leverage ratio, a regulation pertinent to major US banks including JPMorgan Chase, Goldman Sachs, and Morgan Stanley.

Texas Instruments announced plans to spend more than $60 billion on semiconductor plants in the US. It will build seven semiconductor fabrication plants across Texas and Utah, resulting in more than 60,000 jobs, the company said in a press release.

Hasbro initiated a 3% workforce reduction, equating to approximately 150 employees, as part of a multi-year restructuring programme. The company had previously indicated in April that tariffs could necessitate such layoffs. Shares closed marginally higher at $67.93 but experienced a slight decline in after-hours trading.

Shares of Circle Internet Group increased substantially, closing up +33.82%, following the Senate's passage of the Genius Act, legislation aimed at cryptocurrency regulation. The recently listed firm has actively advocated for regulatory guidelines to legitimise the industry.

Scholar Rock's shares advanced +16.60%, with gains extending into after-hours trading, subsequent to reporting positive results from a Stage 2 trial of its weight-loss drug.

American Depositary Receipts for Nintendo rallied after its Tokyo-listed shares reached an all-time high. Last week, the company reported record sales figures for its Switch 2 console.

A subsidiary of Prudential Financial is set to acquire up to $500 million in loans from Affirm. This transaction exemplifies a growing trend of collaborations between large private-credit investors and financial technology (fintech) firms.

Mega caps: The Magnificent Seven had a mostly negative performance this week, with Nvidia +1.86%, Microsoft +1.61%, and Meta Platforms +0.23%, while Amazon -0.32%, Apple -1.11%, Tesla -1.34%, and Alphabet -2.27%.

Energy stocks had a positive performance this week, with the Energy sector itself +2.19%. WTI and Brent prices are +9.62% and +9.04%, respectively, over the past seven days. Over this past week Energy Fuels +6.47%, APA +3.57%, ExxonMobil +3.55%, BP +3.45%, Shell +3.31%, Phillips 66 +3.20%, Chevron +2.36%, Hess +2.19%, Marathon Petroleum +1.68%, Occidental Petroleum +1.14%, ConocoPhillips +0.48%, and Halliburton +0.41%, while Baker Hughes -0.13%.

Materials and Mining stocks had a mixed performance this week, with the Materials sector -1.25%. Over the past seven days, Newmont Corporation +9.29%, Nucor +7.73%, Yara International +6.07%, CF Industries +5.32%, Mosaic +5.17%, Sibanye Stillwater +0.58%, and Freeport-McMoRan +0.41%, while Albemarle -8.73%.

European Stock Indices Price Performance

Stoxx 600 -1.52% MTD and +6.44% YTD

DAX -2.83% MTD and +17.12% YTD

CAC 40 -1.24% MTD and +3.73% YTD

IBEX 35 -1.62% MTD and +20.08% YTD

FTSE MIB -1.75% MTD and +15.21% YTD

FTSE 100 +0.81% MTD and +8.20% YTD

This week, the pan-European Stoxx Europe 600 index is -2.05%%. It was -0.36% on Wednesday, closing at 540.33.

So far this month in the STOXX Europe 600, Oil &Gas is the leading sector, +6.61% MTD and +10.48% YTD, while Autos & Parts is the weakest at -6.34% MTD and -8.54% YTD.

This week, Oil & Gas outperformed within the STOXX Europe 600, at +2.73%, followed by Utilities and Banks at -0.09% and -0.67%, respectively. Conversely, Autos & Parts underperformed at -5.44%, followed by Health Care and Financial Services, at -4.23% and -3.65%, respectively.

Germany's DAX index was -0.50% on Wednesday, closing at 23,317.81. It was -2.64% for the week. France's CAC 40 index was -0.36% on Wednesday, closing at 7,656.12. It was -1.54% over the past week.

The UK's FTSE 100 index was -0.24% over the past week to 8,843.47 . It was +0.11% on Wednesday as UK inflation came in at 3.4% y/o/y. This was in line with expectations. It was roughly the same as April’s data which had shown an error due to a car tax data miscalculation. May core inflation, which excludes more volatile energy, food, alcohol and tobacco prices, was 3.5%, down from 3.8% in the twelve months to April. The Bank of England is widely expected to keep interest rates on hold given that inflation remains above target and there is ongoing uncertainty around tariffs and the risk of energy prices rising due to the Israeli-Iran war.

In Wednesday's trading session, in the STOXX Europe 600 index, Health Care experienced the most significant decline, primarily due to pressure on large-cap companies and ongoing valuation concerns. While Gerresheimer outperformed amidst takeover speculation, the sector was dragged lower by losses in names like Sanofi and AstraZeneca due to concerns about potential pharmaceutical tariffs from the White House, along with a downturn in Fresenius Medical Care.

The Autos & Parts sector faced pressure due to anxieties over a lack of progress on trade deals from the G7 summit. This comes despite a looming 9th July deadline for reciprocal tariffs. Reports indicate that the US Commerce Department will announce findings on national security sectors, which could lead to tariffs on foreign imports, heightening the complexity of future outlooks, especially given the US President's focus on tariffs as a revenue source.

Chemicals underperformed following cautious broker initiations and downgrades. Financial Services declined, with UBS Group downgraded by Morgan Stanley, attributed to stricter Swiss capital rules. Conversely, Banks were the best performers ahead of the Fed's rate decision. Southern European banks saw modest gains amid M&A speculation, particularly around Banco de Sabadell. Nordic and UK banks also edged higher on corporate actions.

Oil & Gas names slightly outperformed, supported by positive contract and license updates and higher crude prices driven by Middle East tensions. However, Tullow Oil shares declined after merger talks with Meren Energy collapsed. Industrial Goods & Services was down overall but found some support from Aerospace names like Airbus, which gained on dividend policy changes and momentum from the Paris Air Show.

Telecom and Utilities were relative outperformers compared to the broader market, driven by their appeal as safer assets and their bond proxy profiles.

According to LSEG I/B/E/S data, Q1 earnings are expected to increase 2.3% from Q1 2024. Q1 revenue is expected to increase 2.4% from Q1 2024. Excluding the Energy sector, revenues are expected to increase 4.3%. Of the 287 companies in the STOXX 600 have reported earnings to date for Q1 2025, 58.5% reported results exceeding analyst estimates. In a typical quarter 54% beat analyst EPS estimates. Of the 349 companies in the STOXX 600 have reported revenue to date for Q1 2025, 54.7% reported revenue exceeding analyst estimates. In a typical quarter 58% beat analyst revenue estimates.

During the week of 23 June two companies are expected to report quarterly earnings.

Financials is the sector with most companies reporting above estimates at 76%. Financials and Utilities, with surprise factors of 10% and 9% respectively, are the sectors that beat earnings expectations by the highest surprise factor. In the Energy sector, 59% of companies have reported below estimates. Consumer Cyclicals’ earnings surprise factor was the lowest at -9%. The STOXX 600 surprise factor is 6.3%, which is above the long-term (since 2012) average surprise factor of 5.8%. The estimated earnings growth rate for the STOXX 600 for Q1 2025 is 2.3%. The forward four-quarter price-to-earnings ratio (P/E) for the STOXX 600 sits at 14.2x, slightly below the 10-year average of 14.3x.

Other Global Stock Indices Price Performance

MSCI World Index +1.16% MTD and +5.75% YTD

Hang Seng +1.81% MTD and +18.20% YTD

This week, the Hang Seng Index was -2.69%. The MSCI World Index was -0.50%.

Currencies

EUR +1.18% MTD and +10.95% YTD to $1.1481.

GBP -0.27% MTD and +7.30% YTD to $1.3422.

The dollar index was +0.04% on Wednesday to 98.85. The Dollar Index is +0.22% this week and -0.59% so far MTD. It has fallen -8.88% YTD as rising concerns over US debt and fiscal policies along with continuing trade uncertainty hit sentiment.

On Wednesday, the US dollar traded mostly against major currencies. This movement occurred as escalating conflict between Israel and Iran prompted investors to seek safe-haven assets.

Despite data indicating a decrease in new unemployment benefit applications in the US (though figures remained elevated), the dollar largely maintained weaker trading ranges. On Wednesday the euro was unfazed against the dollar, settling at $1.1481, however, the euro registered a weekly -0.05% against the US dollar.

The British pound saw a modest increase of +0.03% to $1.3422. This came as the Office for National Statistics reported that UK CPI rose by 3.4% y/o/y in May, aligning with forecasts ahead of today's BoE decision. For the week, the British pound is -0.91% lower versus the US dollar.

Money markets suggest that traders do not anticipate the BoE will cut UK interest rates until at least September, with an additional quarter-point cut possible by December.

In Sweden, the central bank proceeded with an anticipated rate cut, resulting in a slight weakening of the krona against the euro, which rose +0.57% to 11.0300 kronor.

Since last Thursday, the dollar has gained approximately one percentage point against both the Japanese yen and the Swiss franc. However, on Wednesday, the US currency experienced a slight pullback, declining fractionally against both the yen and the franc. The Japanese yen fell slightly against the dollar by -0.12% to ¥145.05 the day after the BoJ kept rates on hold. The Japanese currency is +0.70% MTD and -7.59% YTD.

Later today, the Swiss National Bank, the BoE, and Norges Bank are all scheduled to announce their respective monetary policy decisions.

Note: As of 5:00 pm EDT 18 June 2025

Cryptocurrencies

Bitcoin +0.45% MTD and +11.98% YTD to $105,116.61.

Ethereum -1.52% MTD and -24.51% YTD to $2,530.26.

Bitcoin is -3.37% and Ethereum -9.67% over the past 7 days. On Wednesday Bitcoin was +0.49% to $105,116.61 and Ethereum +0.36% to $2,530.26.

Bitcoin and Ether are down over the past week as markets have focussed on rising global instability following the outbreak of war between Israel and Iran. As noted by crypto.news, data from Deribit shows that the put-to-call volume ratio rose to 2.17, indicating that more traders are buying put options as a hedge. This suggests that they are expecting a further decline in the price of Bitcoin.

However, cryptocurrencies could be set to benefit from the passage, in a 68 to 30 vote, of the GENIUS ACT stablecoin bill on Wednesday by the US Senate. This bill establishes federal guardrails for US dollar-pegged stablecoins and creates a regulated pathway for private companies to issue digital dollars. Yet, although crypto supporters have hailed this as encouraging for wider crypto usage, the Republican-controlled House of Representatives must pass its version of the Stable Act bill or adopt the Senate's GENIUS Act before it heads to President Donald Trump's desk for approval.

Note: As of 5:00 pm EDT 18 June 2025

Fixed Income

US 10-year yield -0.7 bps MTD and -18.0 bps YTD to 4.396%.

German 10-year yield -4.0 bps MTD and +13.1 bps YTD to 2.500%.

UK 10-year yield -15.3 bps MTD and -7.0 bps YTD to 4.498%.

US Treasury yields recovered some earlier losses on Wednesday after Fed Chair Jerome Powell indicated that inflation in goods prices is expected to accelerate over the summer. This expectation stems from the ongoing impact of the US President's tariffs as they are passed on to consumers.

Powell also cautioned against placing excessive emphasis on the central bank's interest rate forecasts, noting that these projections are subject to change based on incoming economic data.

At the close of trading, the yield on US 10-year notes was down -0.8 bps, settling at 4.396%. The interest-rate-sensitive 2-year note yield also declined by -0.8 bps to 3.954%. Conversely, the 30-year yield on the longer end of the curve remained unchanged at 4.893%.

For the week, the yield on the 10-year Treasury note was -3.1 bps. The yield on the 30-year Treasury bond was -2.7 bps. On the shorter end, the two-year Treasury yield is -0.2 bps this week.

Government figures revealed that foreign entities reduced their overall Treasury holdings in April to $9.013 trillion, a decrease from $9.050 trillion in March. However, Japan and the UK, which are the two largest foreign holders of US debt, both increased their holdings during the month. In contrast, China, the third-largest holder, reduced its position by $8.2 billion, and Canada cut its holdings by $57.8 billion.

The bond market will be closed today in observance of the federal Juneteenth holiday.

Fed funds futures traders are now pricing in a 9.3% probability of a July cut, according to CME Group's FedWatch Tool. A rate cut at the Fed’s September meeting is still seen as the next most likely, with a 57.9% probability. Traders are currently pricing in 47 bps of cuts by the end of the year, less than last week’s 49.3 bps.

Across the Atlantic, eurozone bond yields saw a modest decline on Wednesday as traders anticipated the outcome of the Federal Reserve meeting scheduled for later in the day.

Markets are currently pricing in one final 25 bps rate cut from ECB this cycle, which would bring its terminal rate to 1.75%. These expectations have remained fairly consistent in recent weeks, leading to range-bound trading in government bonds.

In the UK, on Wednesday the 10-year gilt -6.1 bps to 4.498%. The UK 10-year yield is -5.3 bps over the past 7 days.

Germany's 10-year yield was -3.7 bps to 2.500% on Wednesday. Germany's policy-sensitive two-year yield was -1.8 bps to 1.850%, On the longer end of the maturity spectrum, Germany's 30-year yield was -3.9 bps on Wednesday, to 2.947%.

For the week, the German 10-year yield was -3.7 bps. Germany's two-year bond yield +0.2 bps, and on the longer end of the curve, Germany's 30-year yield was -5.4 bps.

The spread between US 10-year Treasuries and German Bunds is now 189.6 bps, 0.6 bps than last week’s 189.0 bps.

On Wednesday, Italy's 10-year yield -3.6 bps to 3.452%. The spread between Italy's 10-year yield compared to Germany's Bund yield stands at 95.2 bps, 3.9 bps higher than last week’s 91.3 bps spread. Italian 10-year yields -5.3 bps over the past 7 days.

Commodities

Gold spot +2.55% MTD and +28.61% YTD to $3,373.16 per ounce.

Silver spot +11.43% MTD and +27.14% YTD to $36.74 per ounce.

West Texas Intermediate crude +23.16% MTD and +4.46% YTD to $74.87 a barrel.

Brent crude +19.33% MTD and +1.93% YTD to $76.25 a barrel.

Gold prices are +0.59% this week and +28.61% YTD. Gold prices declined on Wednesday following the FOMC decision to maintain interest rates, accompanied by indications of a more gradual pace for future rate cuts. Fed Chair Jerome Powell further stated that the central bank anticipates a ‘meaningful amount of inflation’ in the coming months.

Spot gold was -0.48% on Wednesday to reach $3,373.16 per ounce. The US dollar index registered a gain of +0.04%, making gold slightly less affordable for international buyers holding other currencies.

This week, WTI and Brent are +9.62% and +9.04%, respectively. Oil prices concluded Wednesday's volatile trading session lower, as investors assessed the potential for supply disruptions stemming from the Iran-Israel conflict and the possibility of direct US involvement. Brent crude futures settled down 67 cents, or -0.87%, at $76.25 a barrel while WTI crude declined by 54 cents, or -0.72%, reaching $74.87. This followed a more than five percentage points increase in prices on Tuesday.

Iranian Supreme Leader Ayatollah Ali Khamenei stated, through a state television presenter, that his country would not accept the US President's call for an unconditional surrender. While the US President indicated his patience had expired, he did not disclose his next steps.

The US military is increasing its presence in the region, fuelling speculation about potential US intervention. Iran's ambassador to the UN in Geneva has communicated to Washington that Tehran will respond firmly if the US becomes directly involved in Israel's military campaign.Investors are concerned that such intervention could broaden the conflict in an area critical for global energy resources, supply chains, and infrastructure.

A significant concern for the oil market is the potential closure of the Strait of Hormuz, a vital chokepoint through which nearly one-third of global seaborne oil trade passes. Iran, as OPEC's third-largest producer, currently extracts approximately 3.3 million barrels per day (bpd) of crude oil.

EIA weekly report: US crude inventories fall by most in a year. US crude oil stockpiles saw a significant drop last week, marking their largest decline in a year, according to Wednesday's report from the Energy Information Administration (EIA). While crude inventories fell, gasoline and distillate inventories rose.

Crude inventories decreased by 11.5 million barrels, settling at 420.9 million barrels for the week ending 13th June. The Cushing, Oklahoma, delivery hub also saw crude stocks decline, falling by 995,000 barrels.

The decline in crude stockpiles was influenced by a shift in trade: net US crude imports fell by 1.8 million barrels per day (bpd) to 1.1 million bpd, while exports climbed by 1.1 million bpd to 4.4 million bpd. This increase in exports is noteworthy given that the price difference between Brent and WTI crude futures has narrowed and this typically discourages exports.

Refinery crude runs decreased by 364,000 bpd, with utilisation rates falling 1.1 percentage points to 93.2% of total capacity.

On the product side, gasoline stocks rose 209,000 barrels to 230 million barrels for the week. Gasoline product supplied, an indicator of demand, rose 129,000 bpd to 9.3 million bpd. Distillate stocks, including diesel and heating oil, also grew by 514,000 barrels to 109.4 million barrels.

The four-week average for total product supplied stood at 20 million bpd, a slight decrease of 0.3% from year-ago levels.

Note: As of 5:00 pm EDT 18 June 2025

Key data to move markets

EUROPE

Thursday: Speeches by ECB President Christine Lagarde, Bundesbank President Joachim Nagel, and ECB Vice President Luis de Guindos.

Friday: German Producer Price Index (PPI), Eurogroup Meeting, Economic Bulletin, and Eurozone Consumer Confidence.

Monday: German HCOB Services, Manufacturing, and Composite PMIs, German Buba Monthly Report, French HCOB Services, Manufacturing, and Composite PMIs, and Eurozone HCOB Services, Manufacturing, and Composite PMIs.

Tuesday: German IFO Business Climate, Current Assessment and Expectations surveys, and a speech by ECB Executive Board Member Philip Lane.

Wednesday:. Spanish GDP, and EU Leaders Summit.

UK

Thursday: BoE Interest Rate Decision, Minutes, and Monetary Policy Summary, and GfK Consumer Confidence.

Friday: Retail Sales.

Monday: S&P Global Services, Manufacturing, and Composite PMIs.

Tuesday: Speeches by BoE External Member Megan Greene, Deputy Governor Dave Ramsden, Governor Andrew Bailey, and Deputy Governor of Financial Stability Sarah Breeden.

Wednesday: Speeches by BoE’s Deputy Governor Clare Lombardelli and Chief Economist Huw Pill.

USA

Thursday: Markets closed in observance of Juneteenth.

Friday: Philadelphia Fed Manufacturing Survey.

Sunday: A speech by San Francisco Fed President Mary Daly.

Monday: S&P Global Services, Manufacturing, and Composite PMIs, Existing Home Sales, and a speech by Chicago Fed President Austan Goolsbee.

Tuesday: Housing Price Index, Consumer Confidence, Richmond Fed Manufacturing Index, and speeches by Cleveland Fed President Beth Hammack and New York Fed President John Williams.

Wednesday: New Home Sales.

CHINA

Thursday: PBoC Interest Rate Decision.

JAPAN

Thursday: National CPI and Core CPI, and BoJ Monetary Policy Meeting Minutes.

Tuesday: BoJ Summary of Opinions.

Global Macro Updates

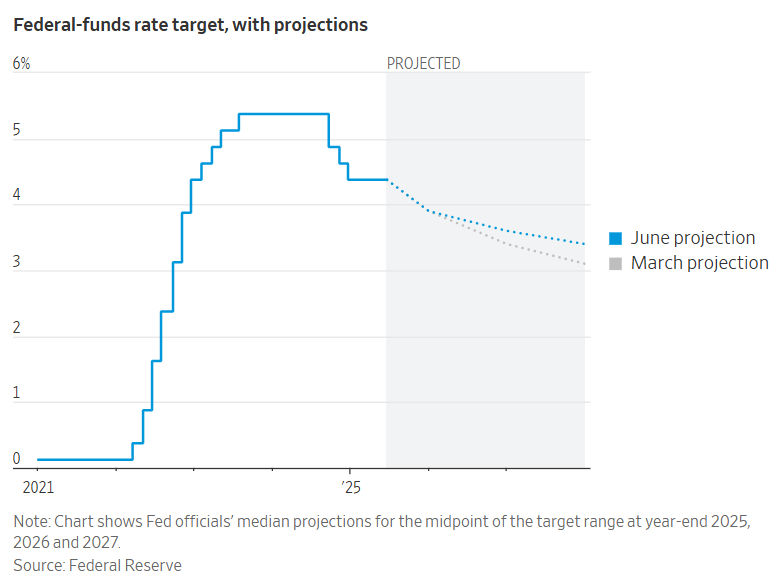

The Fed warns of uncertainty clouding the outlook. As widely expected, the US Federal Reserve’s FOMC, in a unanimous vote, left interest rates unchanged at 4.25-4.50% on Wednesday. The new dot plot projection, the SEP, was left unchanged from March and continued to show two rate cuts through the end of 2025 with a median fed funds rate of 3.875%. Yet there were signs of a difference of opinion among policymakers with 7 officials now foreseeing no rate cuts this year, compared with 4 in March, and 2 others expecting one cut this year. However,10 officials expect it will be appropriate to lower rates at least twice before the end of 2025. In addition, the Fed lowered its 2025 GDP estimate to 1.4% from March’s 1.7% estimate and raised its inflation forecast to 3.0% from 2.7%. The Fed also sees a 4.5% unemployment rate at the end of 2025 vs 4.4% in March projections. They also said uncertainty about the economic outlook had diminished, but remained elevated. Within the statement itself, the Fed removed the line from the previous meeting that said risks to both unemployment and inflation had risen. The statement now says "the unemployment rate remains low" whereas it had previously said that it ‘has stabilised at a low level in recent months’.

During the press conference, Chair Jerome Powell repeated that the central bank was “well positioned to wait to learn more about the likely course of the economy before considering any adjustments to our policy stance.” He also said that the Fed expects more inflation over the coming months and that projections have moved more toward slower growth. Although the impact from tariffs have yet to show in the data, Chair Powell said ‘Ultimately the cost of the tariff has to be paid and some of it will fall on the end consumer. We know that because that’s what businesses say, that’s what the data say from the past.’

The combination of slowing growth, sticky inflation and increasing geopolitical risk puts the Fed in a difficult position, especially as the US president continues to call for the Fed to cut rates immediately. The question is, which part of the Fed’ dual mandate will be hit the hardest first, ie., will tariffs increase inflation or will the jobs market start to significantly falter. The Fed seems intent on a “wait and see” approach and being data dependent. The risk is that data is backward looking and therefore, the Fed could, down the line, be forced into taking action very quickly and surprising markets, much as it did with its initial, ‘outsized’ cut last year.

US softening activity: jobless claims stable, but housing starts misses forecasts. Initial jobless claims for the latest week came in at 245,000, outperforming the consensus estimate of 250,000 and marking a decrease from the previous week's upwardly revised figure of 250,000. The four-week moving average for claims rose to 245,500, an increase of 4,750 from the prior week. Meanwhile, continuing claims registered at 1,945,000, slightly above the consensus of 1,940,000, but down from the previous week's downwardly revised 1,951,000.

In the housing market, May saw a significant decline, with US housing starts falling 9.3% m/o/m to 1.256 million units. This figure missed the consensus of 1.370 million and was considerably lower than April's upwardly revised 1.392 million, reaching its lowest point since May 2020. Single-family housing starts stood at an annualized rate of 924,000. Additionally, May building permits decreased by 2.0% m/o/m to 1.393 million, falling short of the 1.430 million consensus and April's 1.422 million. This follows yesterday's disappointing June NAHB housing market index, which also missed consensus and declined m/o/m. The report highlighted a monthly decline in both sales expectations for the next six months and the number of prospective buyers. Notably, 37% of builders reported cutting prices in June, the highest percentage since the NAHB began tracking this metric monthly in 2022.

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

Tento článek je poskytován pouze pro informační účely a neměl by být považován za nabídku nebo výzvu k nákupu nebo prodeji jakýchkoli investic nebo souvisejících služeb, jejichž odkazy se v něm můžou vyskytovat. Obchodování s finančními nástroji je spojeno se značným rizikem ztráty a nemusí být vhodné pro všechny investory. Dřívější produktivita není spolehlivým ukazatelem budoucí produktivity.