Will the dollar continue to drop?

Global market indices

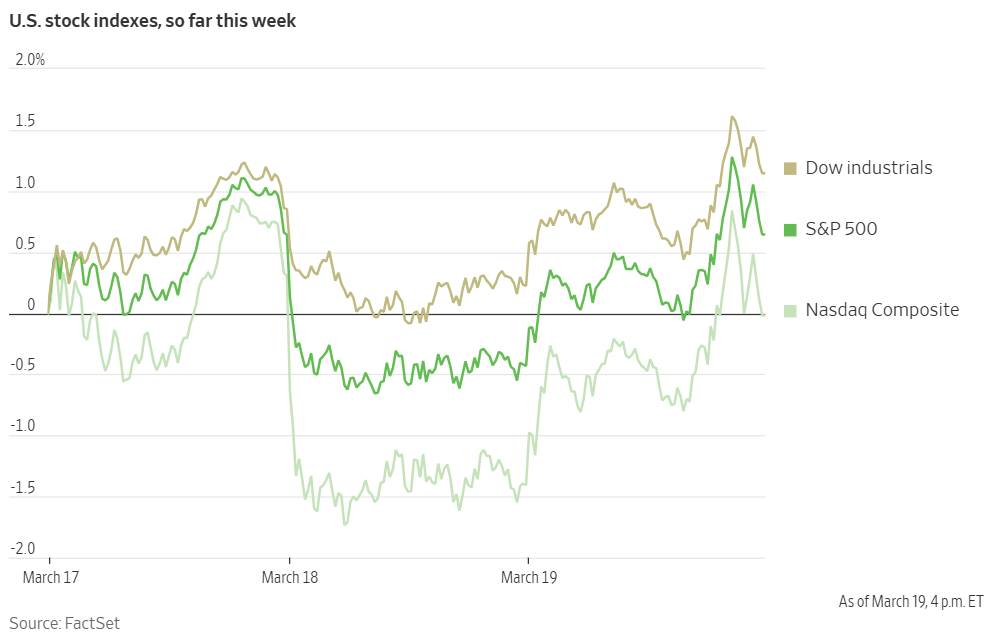

US Stock Indices Price Performance

Nasdaq 100 -5.50% MTD and -6.07% YTD

Dow Jones Industrial Average -4.28% MTD and -1.36% YTD

NYSE -2.23% MTD and -2.54% YTD

S&P 500 -4.69% MTD and -3.51% YTD

The S&P 500 is +2.78% over the past week, with 10 of the 11 sectors down MTD. The Equally Weighted version of the S&P 500 is +2.40% this week. Its performance is -2.83% MTD and -0.29% YTD.

The S&P 500 Energy sector is the leading sector so far this month, +2.07% MTD and +7.54% YTD, while Consumer Discretionary is the weakest sector at -9.29% MTD and -14.23% YTD.

This week, Energy outperformed within the S&P 500 at +5.63%, followed by Financials and Information Technology at +3.86% and +2.96%, respectively. Conversely, Consumer Discretionary underperformed at -0.96%, followed by Consumer Staples and Real Estate at +0.64% and +0.87%, respectively.

Following the FOMC's decision on Wednesday to maintain the benchmark interest rate, equity markets rose. Despite a downward revision of the Fed's economic growth projections for the current year, stocks rallied, marking the most significant single-day gain on a Fed announcement day since July. This positive market response occurred after a challenging four-week period that saw the S&P 500 enter into correction territory.

In a subsequent assessment of the economic outlook, Fed Chair Jerome Powell acknowledged the potential influence of the US President's policies, particularly the impact of tariffs on inflation, which he suggested was likely to be ‘transitory.’ The market's positive reaction appeared to stem from a perception that the Fed's stance was less hawkish than anticipated. This sentiment fuelled Wednesday's rally, even in the context of revised Fed forecasts that might typically be viewed as unfavourable for equities, including reduced growth expectations for 2025 and an increased inflation estimate.

This seemingly counterintuitive market behaviour, often referred to as a ‘bad news is good news’ reaction, indicates that investors may interpret the Summary of Economic Projections (SEP) not as a definitive prediction, but rather as a reflection of prevailing economic uncertainty with a slightly dovish inclination.

At the close of trading, the S&P 500 Index was +1.1%, while the Nasdaq 100 Index was +1.3%. The Dow Jones Industrial Average also rose, adding 383 points or +0.9%.

In corporate news, Boeing's shares rallied +6.84%, as the aerospace manufacturer's CFO informed investors that the company's performance in Q1 2025 was currently aligned with expectations.

Mega caps: The Magnificent Seven had a mixed performance this week with Microsoft +2.39%, Nvidia +1.68%, and Amazon +0.85%, while Apple -0.80%, Meta Platforms -1.11%, Alphabet -1.93%, and Tesla -4.93%.

Today, in an interview with the Financial Times, Jensen Huang, Nvidia’s chief executive and co-founder, said, “overall, we will procure, over the course of the next four years, probably half a trillion dollars worth of electronics in total. And I think we can easily see ourselves manufacturing several hundred billion of it here in the US.” He also noted that Nvidia was now able to manufacture its latest systems in the US through suppliers such as Taiwan Semiconductor Manufacturing Company and Foxconn, and that he saw a growing competitive threat from Huawei in China.

Energy stocks had a strong performance this week, with the Energy sector itself +5.63%. WTI and Brent prices are -0.74% and -0.11%, respectively, this week. Over this past week Marathon Petroleum +9.08%, Hess +8.57%, Chevron +7.45%, ExxonMobil +6.20%, Apa +5.90%, BP +5.86%, Occidental Petroleum +5.52%, ConocoPhillips +5.34%, Phillips 66 +5.31%, Shell +5.30%, Baker Hughes +4.99%, Energy Fuels +1.83%, and Halliburton +1.50%.

Materials and Mining stocks had a positive performance this week, with the Materials sector up +2.72%. Over the past seven days, Mosaic +13.28%, Sibanye Stillwater +11.98%, Newmont Corporation +9.99%, Freeport-McMoRan +9.90%, Albemarle +9.17%, Yara International +3.97%, CF Industries +0.72%, and Nucor +0.15%.

European Stock Indices Price Performance

Stoxx 600 -0.33% MTD and +9.41% YTD

DAX +3.27% MTD and +16.97% YTD

CAC 40 +0.74% MTD and +10.71% YTD

IBEX 35 +0.46% MTD and +15.64% YTD

FTSE MIB +2.74% MTD and +16.17% YTD

FTSE 100 -1.17% MTD and +6.53% YTD

This week, the pan-European Stoxx Europe 600 index is +2.61%. It was +0.19% on Wednesday, closing at 555.37.

So far this month in the STOXX Europe 600, Construction & Materials is the leading sector, +4.62% MTD and +14.10% YTD, while Travel & Leisure is the weakest at -7.27% MTD and -5.88% YTD.

This week, Oil & Gas outperformed within the STOXX Europe 600 with a +6.08% gain, followed by Banks and Basic Resources at +5.20% and +3.77%, respectively. Conversely, Autos & Parts underperformed at 0.00%, followed by Chemicals and Personal & Household Goods, at +0.13% and +0.16%, respectively.

Germany's DAX index was -0.40% on Wednesday, closing at 23,288.06. It was +2.70% for the week. France's CAC 40 index was +0.70% on Wednesday, closing at 8,171.47. It was +2.28% over the past week.

The UK's FTSE 100 index is +1.94% over the past week to 8,706.66. It was +0.02% on Wednesday.

Within the Stoxx Europe 600 on Wednesday, Basic Resources underperformed, with Rio Tinto in focus after recommending shareholders vote against Palliser's resolution, a recommendation that contrasts with advice from ISS to vote in favour. In the Forestry & Paper subsector, Stora Enso has launched a new consumer board line, with the goal of achieving EBITDA breakeven by the end of 2025.

The Industrial Goods & Services sector was also in the spotlight, particularly due to Industrie De Nora reporting FY 2024 earnings of €88.8 million, which exceeded FactSet estimates. Deutz saw its share price rise following the approval of Germany’s constitutional amendment and budget plan. Conversely, Siemens Aktiengesellschaft announced efficiency plans that will affect 5,600 jobs; it was downgraded by RBC Capital Markets. Within Industrial Transportation, Stadler Rail reported a FY 2024 net income of CHF38.4 million, falling short of expectations.

The Aerospace & Defence sector remains strong, supported by increased defence spending in Germany and the broader eurozone. The Energy sector also outperformed on Wednesday, with focus on Vitol's acquisition of Eni assets for $1.65 billion.

The Health Care sector weakened, with attention focused on Haleon, as Pfizer sold 618 million shares in its final stake sale. BioVersys reported progress in a tuberculosis trial.

Other Global Stock Indices Price Performance

MSCI World Index -3.49% MTD and -0.95% YTD

Hang Seng +7.98% MTD and +23.49% YTD

This week, the Hang Seng Index was +4.96% and the MSCI World Index was +0.81%.

Currencies

EUR +5.09% MTD and +5.31% YTD to $1.0903.

GBP +3.36% MTD and +3.93% YTD to $1.2999.

The euro was +0.14% against the USD over the past week, while the British pound was +0.28% against the dollar. The Dollar Index is -0.11% so far this week and -4.62% YTD.

Following the FOMC’s widely expected decision on Wednesday to maintain the benchmark interest rate, the US dollar relinquished some of its earlier gains against the euro. This movement occurred despite the Fed's indication that policymakers anticipate reducing borrowing costs by only half a percentage point by the end of the current year. Fed officials maintained the same median forecast as three months prior, even as their outlook incorporated slower economic growth and higher inflation.

In his remarks on Wednesday, Fed Chair Jerome Powell characterised the current level of uncertainty as ‘unusually elevated.’ He described the challenges facing Fed officials in formulating new economic projections amidst the recent wave of policy initiatives from the US administration.

While the US dollar has stabilised in recent trading sessions, its near-term trajectory is likely to be influenced by the strength of forthcoming economic data releases.

The euro was -0.39% on Wednesday, to trade at $1.0903, having earlier reached an intraday low of $1.0860. The dollar index rose +0.22% to 103.47.

The British pound remained relatively stable on Wednesday, registering a marginal decrease of -0.02% to trade at $1.2999 against the US dollar.

The US dollar weakened against the Japanese yen, falling by -0.38% to ¥148.70. This followed BoJ's decision earlier on Wednesday to keep its interest rates unchanged. The widely expected decision by the BoJ underscored policymakers' preference to allow more time to assess how increasing global economic risks stemming from higher US tariffs might affect Japan's economic recovery.

The dollar has appreciated by +0.32% against the yen over the past week, but depreciated by -1.26% thus far this month.

Note: As of 5:00 pm EST 19 March 2025

Fixed Income

US 10-year yield +1.7 bps MTD and -33.9 bps YTD to 4.237%.

German 10-year yield +39.6 bps MTD and +43.8 bps YTD to 2.807%.

UK 10-year yield +15.7 bps MTD and +7.4 bps YTD to 4.642%.

Following the FOMC's announcement Wednesday, US Treasury yields declined as policymakers signaled their continued expectation of reducing borrowing costs by half a percentage point by the end of the year. This indication countered some market expectations that this projection might be revised downward to a single 25-basis-point cut.

The US Treasury 10-year bond yield is -7.8 bps over the past week and on Wednesday it was -5.3 bps lower to 4.237%. On the short end of the curve, the yield on the 2-year Treasury note was relatively unchanged, +0.2 bps, this week to 3.993%. It was -5.5 bps on Wednesday. On the longer end of the curve, the 30-year yield was -8.1 bps lower on the week and settled at 4.552%, after falling by -3.4 bps on Wednesday.

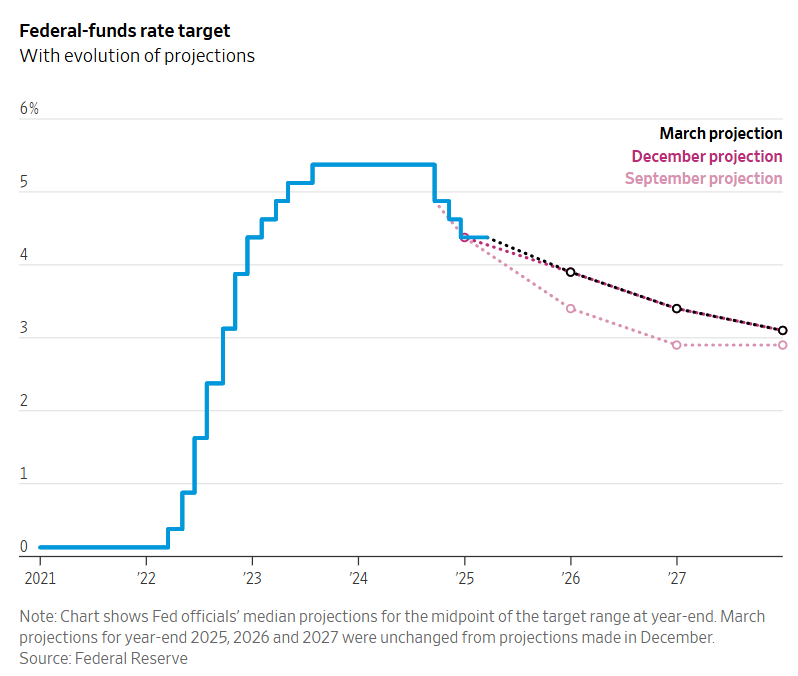

As widely anticipated, the FOMC maintained the federal funds rate at its current level. Concurrently, Fed officials revised their inflation outlook for the current year upwards. However, they also adjusted their economic growth forecast downwards, anticipating a slight increase in the unemployment rate by the end of the year. While the median interest rate projection remained unchanged, a greater number of policymakers revised their individual forecasts to reflect fewer expected rate reductions. The updated economic projections revealed that 11 out of 19 policymakers anticipate at least two rate cuts by the Fed this year, representing a narrower majority compared to the 15 officials who had projected at least two cuts in December.

During the press conference, Fed Chair Jerome Powell said it was too early to tell if the Fed would dismiss the inflationary impact of US tariffs. He further noted the inherent difficulty in quantifying the extent to which any increases in goods prices could be attributed to tariffs.

The prevailing uncertainty surrounding the implementation and economic consequences of tariffs has negatively impacted consumer confidence and contributed to declines in stock market valuations. This environment has, in turn, bolstered demand for the relative safety of Treasuries in recent weeks, driving yields down to their lowest levels in months.

The probability for a Fed 25 bps rate reduction at its 7th May meeting on Wednesday stood at 20.5% according to the CME Group's FedWatch Tool. Traders are currently pricing in 57.1 bps of cuts by the Fed this year, above projections of 69.8 bps last week, down from Tuesday’s 59.1 bps.

On Wednesday eurozone yields were slightly down as market attention gravitated towards the FOMC policy meeting and the potential implications of US tariff threats. This refocus on the US came a day after Germany's Bundestag approved a substantial increase in public expenditure. The approval was a significant development for conservative leader Friedrich Merz and signalled a departure from decades of fiscal conservatism in an effort to stimulate economic growth.

ECB policymaker Olli Rehn commented on Tuesday that trade tensions with the US are expected to have an immediate adverse effect on eurozone economic growth, while any positive impact from increased defence spending is likely to materialise only over the medium term.

Eurostat released revised data on Wednesday indicating that eurozone inflation in February was lower than initially estimated. The y/o/y inflation rate was revised downwards to 2.3%, compared to the flash estimate of 2.4%. This was primarily due to a revision in German inflation figures.

Current market pricing suggests the ECB's deposit rate to be approximately 2% by December. Furthermore, traders are assigning around a 55% probability of a 25 bps interest rate cut at the ECB's meeting on 17th April.

Germany's 10-year government bond yields were -0.6 bps at 2.807% on Wednesday, down -7.5 bps this week. Germany's two-year bond yield, which is particularly sensitive to anticipated ECB rate expectations, was -2.6 bps this week to 2.198%%. On the longer end of the curve, Germany's 30-year yield fell -7.7 bps this week to 3.088%.

The spread between US 10-year Treasuries and German Bunds is now 143.0 bps, just 0.3 bps lower than last week’s 143.3 bps.

Italian bond yields, a benchmark for the eurozone periphery, fell -9.1 bps this week to 3.907%. Consequently, the yield spread between Italian and German bonds narrowed slightly by -1.6 bps to 111.0 bps from 111.6 bps last week. Italy's 10-year bond yield was -2.9 bps on Wednesday. The spread between French and German 10-year bond yields was 1.3 lower bps wider this week, reaching 67.0 bps from 68.3 bps last week.

The UK 10-year yield was -3.9 bps over the past 7 days. On Wednesday 10-year British gilt yields were -0.5 bps to 4.642%.

Commodities

Gold spot +6.20% MTD and +15.47% YTD to $3,035.90 per ounce.

Silver spot +9.44% MTD and +17.88% YTD to $34.43 per ounce.

West Texas Intermediate crude -3.95% MTD and -7.69% YTD to $67.19 a barrel.

Brent crude -2.98% MTD and -5.06% YTD to $70.90 a barrel.

Gold prices are +3.50% this week, reaching record highs and remaining above the psychologically important $3000 mark. Gold is +15.47% YTD. On Wednesday spot gold rose +0.03% to $3,035.90 per ounce. Concurrently, US gold futures settled +0.55% higher, at $3,057.50.

On Wednesday, gold prices were supported by remarks from Fed Chair Jerome Powell and the FOMC's decision to maintain interest rates at their current level The rise in gold was further supported by the Fed's indication of a potential reduction in borrowing costs by half a percentage point before the end of year.

This week, WTI and Brent are -0.74% and -0.11%, respectively. On Wednesday, oil prices fell slightly following the release of US government data indicating a reduction in fuel inventories. However, the Fed's decision to maintain interest rates at their current level served to moderate these gains.

On Wednesday Brent crude futures settled at $70.90 per barrel, marking a $0.45, or +0.64%, increase. WTI crude futures rose by $0.49, or +0.73%, to $67.19 per barrel.

Market participants are increasingly focusing on geopolitical risks in relation to the ongoing ceasefire negotiations between Russia and Ukraine as well as the Middle East as Israel and the US have initiated actions in Gaza and Yemen, respectively. In addition, Russia and Ukraine exchanged accusations of violating a newly established agreement to prevent attacks on energy infrastructure. These developments occurred shortly after a telephone conversation between the US President and Russia's Vladimir Putin.

EIA weekly: US crude oil imports decline amid tariff effects, inventories rise. Following the imposition of tariffs by the US President's administration on imported crude oil from Canada, US crude imports from Canada fell to their lowest level in two years. This contributed to lower overall net US crude imports.

Nevertheless, according to the Energy Information Administration (EIA), US crude inventories rose by 1.7 million barrels to reach 437 million barrels last week, as domestic crude production remained near a record high of 13.6 million barrels per day (bpd).

The US President had previously implemented tariffs on imported crude oil from both Canada and Mexico. However, exemptions were subsequently granted to producers able to demonstrate compliance with the USMCA.

Crude imports from Canada fell by 541,000 bpd to 3.1 million bpd during the week ending 14th March, marking the lowest level since March 2023. Over the same period, net US crude imports declined by 1.44 million bpd to 741,000 bpd, the lowest since October 2023.

Refinery utilisation rates saw a marginal increase of 0.4 percentage points over the week. However, the East Coast experienced a significant drop in utilisation rates, falling to 53.8%, the lowest level observed since July 2020. This decline is attributed to a major turnaround underway at Phillips 66's 258,500 bpd refinery located in Linden, New Jersey. Overall refinery crude runs decreased by 45,000 bpd, as reported by the EIA. Crude stocks at the Cushing, Oklahoma, delivery hub also fell, down 1 million barrels, according to the EIA.

In terms of refined products, US gasoline stocks decreased by approximately 530,000 barrels to 240.6 million barrels during the week. Distillate stocks, including diesel and heating oil, fell 2.8 million barrels to 114.8 million barrels, EIA data showed.

Total product supplied, a measure often used as a proxy for demand, decreased to 19.4 million barrels per day. However, the product supplied of distillates saw an increase, reaching 4 million barrels per day.

Note: As of 5:00 pm EST 19 March 2025

Key data to move markets

EUROPE

Thursday: German PPI, EU Leaders Summit, ECB Economic Bulletin and speeches by ECB President Christine Lagarde and Chief Economist Philip Lane.

Friday: EU Leaders Summit and Eurozone Consumer Confidence.

Monday: French HCOB Composite, Manufacturing and Services PMIs, German HCOB Composite, Manufacturing and Services PMIs, Eurozone Composite, Manufacturing and Services PMIs,

Tuesday: German IFO Business Climate, Current Assessment and Expectations Surveys,

Wednesday: Spanish GDP.

UK

Thursday: Average Earnings, Claimant Count Change, Claimant Count Rate, ILO Unemployment, BoE Interest Rate Decision, BoE Minutes, BoE Monetary Policy Report and BoE Press Conference.

Friday:.GfK Consumer Confidence.

Monday: S&P Global/CIPS Composite, Manufacturing and Services PMIs, Bank of England Quarterly Bulletin, and a speech by BoE Governor Andrew Bailey.

Wednesday: CPI, PPI, and RPI.

US

Thursday: Initial and Continuing Jobless Claims, Philadelphia Fed Manufacturing Survey, and Existing Home Sales Change.

Friday: A speech by New York Fed President John Williams.

Monday: S&P Global Composite, Manufacturing and Services PMIs.

Tuesday: Housing Price Index, Consumer Confidence, New Home Sales Change, and a speech by New York Fed President John Williams.

Wednesday: Durable Goods and Nondefence Capital Goods.

CHINA

Thursday: PBoC Interest Rate Decision.

JAPAN

Thursday:National Consumer Price Index.

Monday: BoJ Monetary Policy Meeting Minutes.

Global Macro Updates

The Fed’s cut to the growth outlook. At its meeting ending Wednesday, the Fed, as widely expected, kept rates at its target range of 4.25% to 4.5%. The Fed’s decision to hold interest rates extends a pause that has been in place since January. However, policymakers said they still see two rate cuts in 2025. The Fed also revealed its latest economic projections which showed officials now expect GDP to expand by 1.7% this year, down from its December projection of 2.1%. It also now forecasts inflation to be 2.7%, up from December’s forecast of 2.5%. During the press conference following the announcement, Fed Chair Jerome Powell said that a “good part” of the central bank’s higher inflation expectation and its new outlook for the economy comes from sweeping tariffs that President Trump is trying to impose. He also noted that progress on inflation was “probably delayed for the time being”. He did insist that although many market economists are anticipating a recession,a severe downturn in the economy still isn’t likely.

The Fed also announced that it was slowing the pace of its quantitative tightening programme, lowering the amount of US Treasury debt it allows to roll off its balance sheet each month from $25bn to $5bn beginning in April.

The tide is turning for Europe. Germany's outgoing parliament on Tuesday approved a substantial €500 billion infrastructure fund, coupled with reforms to the debt brake mechanism. While the Bundestag passed this measure with a vote of 513 to 207, the Bundesrat vote scheduled for tomorrow remains a potential hurdle, with the support of Bavaria deemed crucial. Analysts have cautioned that these spending initiatives, while ambitious, may not guarantee sustained economic growth without the implementation of structural reforms. This implies that they may only provide a short-term boost unless complemented by measures enhancing competitiveness.

Furthermore, the incoming Bundestag will encounter challenges in executing this plan. The CDU/CSU and SPD already possess distinctly different policy priorities, which could lead to internal disagreements within the new governing coalition. Moreover, even with the inclusion of the Green party, a grand coalition would lack the necessary two-thirds majority in the new Bundestag, scheduled to convene its first session on 25th March. The far-right Alternative for Germany (AfD) and the far-left Die Linke increased their representation, collectively holding over 210 seats. Fitch Ratings has issued a warning that Germany's AAA sovereign credit rating could face downward pressure if the increased spending is not adequately balanced with fiscal consolidation measures.

Despite the aforementioned political backdrop, EU equities are projected to maintain growth potential, even in the face of potential tariff headwinds. Both Barclays and Goldman Sachs have highlighted improving prospects for European equities. Goldman Sachs recently revised its EPS growth forecast for the Stoxx Europe 600 upwards to 4% for 2025 and 6% for 2026 - 2027. Barclays anticipates a 4% growth rate for 2025 and an even stronger 8% for 2026. Both banks target a year-end level the Stoxx Europe 600 index at 580, with EPS growth as the primary driver rather than multiple expansion.

Contributing to this evolving sentiment, across the Atlantic, a recent survey of fund managers by Bank of America (BofA) revealed a significant shift in investment strategy, with investors implementing their most substantial reduction in US equity allocations in March, as reported by Bloomberg. This adjustment was largely attributed to concerns surrounding the American economy, fuelled by the US President's trade policy uncertainty.

The survey indicated a dramatic 40 percentage point decline in allocations to US equities, moving from a 17% overweight position in February to a net underweight of 23% in March. This m/o/m contraction in investor confidence represents the most significant decrease recorded by the survey since the onset of the Covid-19 pandemic in March 2020.

Conversely, European equities have benefitted. Allocations to eurozone stocks witnessed a substantial increase of 27 percentage points during the same month, reaching their highest level since July 2021. This was also the sharpest shift out of the US and into Europe since 1999, when BofA’s records began.

While some naysayers may point to inherent structural challenges within the European economy, an often-overlooked factor contributing to the region's past underperformance has been the consistently restrictive policy environment across fiscal, monetary, and regulatory domains over the last decade. A turning point is emerging from this perspective.

The adversarial stance adopted by the US President has seemingly spurred the eurozone into action. Fiscal policy is undergoing a loosening, extending beyond the realm of defence spending. Germany's €500 billion infrastructure package, for instance, represents an annual boost of 1% to the nation's GDP over the next decade. Monetary policy is easing, with eurozone inflation approaching the ECB’s targets this year. This is already stimulating loan growth. Finally, regulatory constraints are being eased in areas like climate change policy.

A word on European defence companies. As we mentioned in our last Alpha Vibes note focused on European and American defence companies, few sectors more accurately reflect the end of the peace dividend, geopolitical risk in Europe, and the associated incorporation of emerging technologies than the defence industry. In this light, the European defence sector has outperformed both Stoxx Europe 600 index and the S&P 500 since 20th January.

That said, investors considering allocating capital to defence companies must navigate certain complexities, notably the recent concerns articulated by the European Commission (EC) regarding design authority. A proposed €150 billion EU defence fund, aimed at supporting member states' procurement of armaments, would be primarily accessible to defence firms based within the EU and those from third countries with existing defence agreements with the Union, according to an EC proposal issued on Wednesday, as reported by the Financial Times.

The proposal also outlines the exclusion of advanced weapons systems where a third country holds ‘design authority’—defined as restrictions on the system's manufacture or the utilisation of specific components—or maintains control over its eventual operational deployment.

This stipulation would, for example, exclude the US Patriot air and missile defence platform, produced by defence contractor RTX, alongside other US weapons systems subject to limitations on their deployment imposed by the US government.

A minimum of 65% of the value of the acquired products would need to be invested within the EU, Norway, and Ukraine, with the residual amount potentially directed towards products from third countries that have ratified a security pact with the EU.

The UK has actively pursued inclusion in this initiative, particularly given its pivotal role in a European ‘coalition of the willing’ dedicated to enhancing the continent's defence capabilities. UK defence companies, including key players such as BAE Systems and Babcock International, are extensively integrated within the defence industries of EU nations like Italy and Sweden.

Should third countries such as the US, UK, and Turkey wish to participate in the proposed initiative, they would be required to establish a formal defense and security partnership with the EU.

The exclusion of the UK and Turkey is expected to create considerable difficulties for major European defence companies that maintain strong relationships with producers or suppliers in those markets, potentially exacerbating fragmentation within the European defence industry—a sector striving for greater local consolidation and reduced reliance on the US. The proposal remains subject to approval by a majority of EU member states.

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

This article is provided to you for informational purposes only and should not be regarded as an offer or solicitation of an offer to buy or sell any investments or related services that may be referenced here. Trading financial instruments involves significant risk of loss and may not be suitable for all investors. Past performance is not a reliable indicator of future performance.

Created by professionals. For professionals.