Global market indices

US Stock Indices Price Performance

Nasdaq 100 +1.78% MTD and +3.38% YTD

Dow Jones Industrial Average +0.59% MTD and -0.06% YTD

NYSE +0.52% MTD and +4.14% YTD

S&P 500 +1.00% MTD and +1.52% YTD

The S&P 500 is +1.00% over the past week, with 8 of the 11 sectors up MTD. The Equally Weighted version of the S&P 500 is +0.56% over this past week and +1.15% YTD.

The S&P 500 Information Technology is the leading sector so far this month, +2.62% MTD and +0.72% YTD, while Utilities is the weakest sector at -1.30% MTD and +6.27% YTD.

Over this past week, Information Technology outperformed within the S&P 500 at +2.78%, followed by Materials and Communication Services at +1.93% and +1.72%, respectively. Conversely, Consumer Discretionary underperformed at -0.14%, followed by Energy and Financials at +0.33% and +0.39%, respectively.

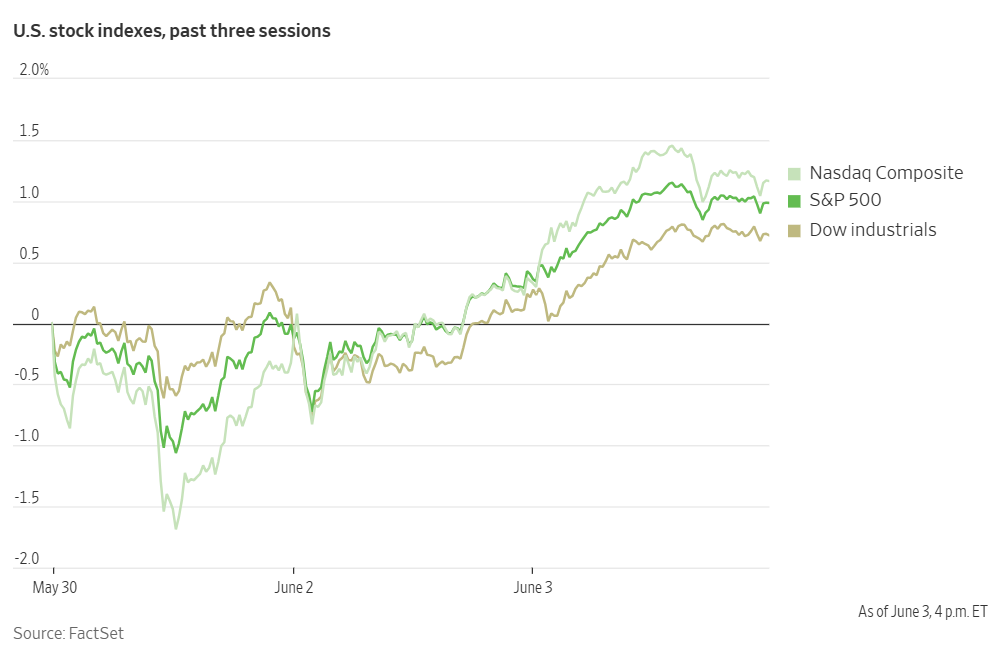

US equities experienced a mixed performance on Wednesday during a choppy yet largely uneventful trading session. The S&P 500 managed to secure its third consecutive gain, now standing 19.8% higher than its closing low on 8th April, following ‘Liberation Day’. While the Nasdaq rose by +0.32%, the Dow Jones Industrial Average slipped by -0.22%, and the S&P 500 saw a modest increase of +0.01%.

The equal-weight version of the S&P 500 was -0.26% on Wednesday, underperforming its cap-weighted counterpart by 0.27 percentage points.

In corporate news, Dollar Tree warned investors that its second-quarter profit could be down as much as 50% from a year ago as it deals with tariff-related costs. It forecast its earnings to rebound in the third and fourth quarters as it expects being able to "mitigate most of the incremental margin pressure from higher tariffs and other input costs" for the whole year.

Wells Fargo finally had a Federal Reserve asset cap removed after seven years that was imposed over its “fake accounts” scandal. The removal will allow it to increase lending and expand its businesses. The bank had paid more than $5 bn in penalties to regulators and class action claimants over the scandal.

CrowdStrike Holdings said in a filing Wednesday that it had received requests for information from the US Department of Justice and the Securities and Exchange Commission “relating to the company’s recognition of revenue and reporting of ARR for transactions with certain customers.” The cybersecurity firm is cooperating with the inquiry.

Mega caps: The Magnificent Seven had a mostly positive performance this week, with Meta Platforms +6.65%, Nvidia +5.27%, Apple +1.44%, Microsoft +1.42%, and Amazon +0.74%, while Alphabet -2.50%, and Tesla -6.96%.

Energy stocks had a slightly positive performance this week, with the Energy sector itself +0.33%. WTI and Brent prices are +1.41% and -0.11%, respectively, this week. Over this past week Energy Fuels +6.25%, APA +3.34%, Hess +1.82%, Baker Hughes +1.66%, ConocoPhillips +1.62%, Shell +1.58%, Occidental Petroleum +1.09%, Chevron +0.99%, ExxonMobil +0.19%, and BP +0.08%, while Phillips 66 -0.26%, Halliburton -0.35%, and Marathon Petroleum -1.05%.

Materials and Mining stocks had a mostly positive performance this week, with the Materials sector +1.93%. Over the past seven days, Nucor +11.96%, Newmont Corporation +5.26%, Freeport-McMoRan +5.07%, Albemarle +3.84%, Mosaic +2.53%, and CF Industries +0.11%, while Yara International -1.35%, and Sibanye Stillwater -2.95%.

European Stock Indices Price Performance

Stoxx 600 +0.43% MTD and +8.55% YTD

DAX +1.16% MTD and +21.49% YTD

CAC 40 +0.68% MTD and +5.74% YTD

IBEX 35 -0.36% MTD and +21.62% YTD

FTSE MIB -0.03% MTD and +17.22% YTD

FTSE 100 +0.33% MTD and +7.69% YTD

This week, the pan-European Stoxx Europe 600 index is +0.38%. It was +0.47% on Wednesday, closing at 551.02.

So far this month in the STOXX Europe 600, Oil & Gas is the leading sector, +1.52% MTD and +5.21% YTD, while Autos & Parts is the weakest at -1.83% MTD and -4.14% YTD.

This week, Health Care outperformed within the STOXX Europe 600, at +1.60%, followed by Oil & Gas and Insurance at +1.25% and +1.01%, respectively. Conversely, Autos & Parts underperformed at -2.57%, followed by Construction Materials and Retail, at -0.82% and -0.57%, respectively.

Germany's DAX index was +0.77% on Wednesday, closing at 24,276.48. It was +0.99% for the week. France's CAC 40 index was +0.53% on Wednesday, closing at 7,804.67. It was +0.21% over the past week.

The UK's FTSE 100 index was +0.86% over the past week to 8,801.29. It was +0.16% on Wednesday.

In Wednesday's trading session, in the STOXX Europe 600 index, the Technology and Basic Resources sectors were higher, primarily driven by the implementation of new tariffs on steel and aluminium. Industrial Goods & Services outperformed other sectors. In this sector, Airbus was a focal point due to reports of securing new orders from Chinese airlines. Saab AB announced that the Royal Thai Air Force has confirmed its selection of Saab's Gripen E/F aircraft. Atlas Copco shares increased following its acquisition of Itsab, a Swedish distributor of compressors and power equipment.

The Construction & Materials sector also demonstrated strong performance, particularly driven by a takeover bid for PwC Sverige. Excluding this specific event, the sector's overall performance was modest, with consistent gains observed from Acciona, and Geberit, fuelled by optimism regarding infrastructure development and stable margins. Sika AG made a strategic investment in Giatec Scientific. Furthermore, Assa Abloy acquired Allegion.

The Health Care sector rose, propelled by momentum in the biotechnology space. Camurus and Eli Lilly and Company entered into a collaboration and licence agreement for long-acting FluidCrystal incretins. Bayer’s and Valneva’s shares were also higher following encouraging pipeline commentary.

In contrast, the Retail sector declined, even though WH Smith rallied on strong travel retail performance. This was offset by B&M European Value Retail, which fell after its earnings report due to margin concerns.

Financial Services edged higher, spearheaded by asset managers Ninety One and Mandatum on the back of growth in their assets under management. However, banks underperformed, as did the Autos & Parts sector. The Real Estate and Energy sectors also experienced declines.

According to LSEG I/B/E/S data, first quarter earnings are expected to increase 2.4% from Q1 2024. Excluding the Energy sector, earnings are expected to increase 7.9%. First quarter revenue is expected to increase 2.3% from Q1 2024. Excluding the Energy sector, revenues are

expected to increase 4.3%. Of the 280 companies in the STOXX 600 that have reported earnings to date for Q1 2025, 58.9% reported results exceeding analyst estimates. In a typical quarter 54% beat analyst EPS estimates. Of the 340 companies in the STOXX 600 that have reported revenue to date for Q1 2025, 55.0% reported revenue exceeding analyst estimates. In a typical quarter 58% beat analyst revenue estimates.

During the week of 9th June, two companies are expected to report quarterly earnings.

Financials is the sector with most companies reporting above estimates at 75%, while Basic Materials with a surprise factor of 11%, is the sector that beat earnings expectations by the highest surprise factor. In the Consumer-Cyclicals sector, 60% of companies have reported below estimates. Additionally, its earnings surprise factor was the lowest at -10%. The STOXX 600 surprise factor is 6.4%, which is above the long-term (since 2012) average surprise factor of 5.8%. The forward four-quarter price-to-earnings ratio (P/E) for the STOXX 600 sits at 14.3x, matching the 10-year average of 14.3x.

Other Global Stock Indices Price Performance

MSCI World Index +0.80% MTD and +5.04% YTD

Hang Seng +1.56% MTD and +17.92% YTD

This week, the Hang Seng Index was +1.70% . The MSCI World Index was +1.27%.

Currencies

EUR +0.62% MTD and +10.29% YTD to $1.1417.

GBP +0.65% MTD and +8.30% YTD to $1.3547.

On Wednesday the dollar index depreciated -0.35% to 98.82. The Dollar Index is -1.06% this week and -0.63% so far MTD. It has declined -8.91% YTD.

The US dollar index declined on Wednesday following a disappointing ADP report on job growth and an unexpected contraction in the US services sector during May. These developments have heightened expectations for potential interest rate cuts by the Fed.

Market attention now shifts to today's jobless claims data and tomorrow's comprehensive US employment report, alongside ongoing trade discussions.

The euro +0.37% against the dollar, reaching $1.1417, but did not surpass Tuesday's high of $1.1451. Gains were somewhat limited by cautious market positioning ahead of the ECB's policy decision scheduled for today. The euro registered a weekly increase of +1.10% against the US dollar.

The British pound settled +0.22% higher to $1.3547, steadily approaching its year-to-date high of 1.3593, benefiting from a combination of a weaker dollar and better-than-expected economic data from the UK. Britain's services sector experienced a modest return to growth last month after contracting in April. On Wednesday it was flat against the euro at 84.11 pence. For the week, the British pound gained +0.62% versus the US dollar.

The Japanese yen strengthened against the dollar by +0.83% to ¥142.75. Should the dollar continue to weaken, the Japanese currency could test its May low of ¥142.11. The Japanese currency is +0.90% MTD and +9.19% YTD.

Note: As of 5:00 pm EDT 4 June 2025

Cryptocurrencies

Bitcoin +0.31% MTD and +12.42% YTD to $104,966.56.

Ethereum +1.97% MTD and -21.56% YTD to $2,619.85.

Bitcoin is -2.39% and Ethereum -0.98% over the past 7 days. On Wednesday Bitcoin was -0.48% to $104,966.56 and Ethereum +1.08% to $2,619.85.

Bitcoin prices seem to be moving on technical momentum as investors consolidate their positions around increasing expectations of Fed rate cuts given softening US economic data, falling yields, and renewed institutional inflows. Meanwhile, Ethereum has been benefitting over the internal restructure at the Ethereum Foundation, which appears to have created growing interest over upcoming protocol upgrades.

The drop in crypto prices this week comes as JPMorgan Chase plans, according to a Bloomberg news report, to let trading and wealth-management clients use some cryptocurrency-linked assets as collateral for loans. It is reported that the firm will start providing financing against crypto exchange-traded funds, beginning with BlackRock Inc.’s iShares Bitcoin Trust. This could open the door to more crypto-backed lending on Wall Street and become another support to the adoption of Bitcoin and other cryptocurrencies. Another potential catalyst emerged on 3 June when Yorkville America Digital filed a Truth Social-branded Bitcoin ETF through NYSE Arca, backed by the Trump Media & Technology Group. If approved, the ETF would track Bitcoin’s price. The SEC’s final decision is expected by 29 January 2026. As noted by cryptonews.com the move aligns Bitcoin with a high-profile political platform but may raise concerns about governance and conflicts of interest.

Note: As of 5:00 pm EDT 4 June 2025

Fixed Income

US 10-year yield -4.4 bps MTD and -21.7 bps YTD to 4.359%.

German 10-year yield -1.3 bps MTD and +15.8 bps YTD to 2.527%.

UK 10-year yield -4.0 bps MTD and +4.3 bps YTD to 4.611%.

On Wednesday, US Treasury yields experienced a decline, driven by weaker-than-anticipated labour market data and an unexpected contraction in the services sector. This was despite growing controversy around the US President’s tax bill. On Wednesday the nonpartisan Congressional Budget Office (CBO) estimated the bill, which would extend President Trump's 2017 tax cuts and increase spending for the military and border security, will add about $2.4 trillion to the existing $36.2 trillion US debt. Another nonpartisan forecaster, the Committee for a Responsible Federal Budget, also said on Wednesday that when taking interest payments into account the bill's cost could rise to $3 trillion over a decade or to $5 trillion if temporary tax cuts were made permanent.

The ADP National Employment Report said private payrolls increased by only 37,000 jobs last month. This figure fell significantly short of the economist’s estimate of 110,000, and followed a downwardly revised gain of 60,000 jobs in April, contributing to the initial drop in yields.

Yields further extended their decline after the Institute for Supply Management (ISM) reported that its non-manufacturing Purchasing Managers' Index (PMI) unexpectedly fell to 49.9 last month. This was below economists' estimate of 52.0 and marked the first reading below the 50 threshold—which signifies contraction in the services sector—since June 2024. Additionally, the ISM's measure of prices paid for services inputs rose to 68.7, the highest level since November 2022, up from 65.1 in April.

The yield on the 10-year US Treasury note fell -11.1 bps to 4.359%, after reaching 4.349%, its lowest point since 9th May. This put it on track for its fourth decline in five sessions. The yield on the 30-year bond also shed -11.3 bps, settling at 4.989%. The two-year US Treasury yield, which typically mirrors interest rate expectations, declined by -8.0 bps to 3.883%, after hitting a session low of 3.858%, its lowest since 9th May.

For the week, the yield on the 10-year Treasury note was -12.0 bps. The yield on the 30-year Treasury bond was -6.2 bps. On the short end of the maturity spectrum, the two-year Treasury yield, which is typically more sensitive to near-term interest rate expectations, is -2.3 bps this week.

Fed funds futures traders are now pricing in a 4.4% probability of a June cut, up from 2.2% last week, according to CME Group's FedWatch Tool. A rate cut at September’s Fed meeting now is seen as the next most likely, with a 77.1% probability. Traders are currently pricing in 55.9 bps of cuts by the end of the year, higher than last week’s 45.3 bps.

In the UK, on Wednesday the 10-year gilt -3.6 bps to 4.611%. The UK 10-year yield is -10.0 bps over the past 7 days.

Eurozone bond yields rose modestly on Wednesday, extending the slight rise from the previous day. This uptick comes as favourable inflation data reinforces expectations for an interest rate cut from the ECB, even as fiscal concerns persist.

On Tuesday, eurozone CPI inflation fell to 1.9% last month from 2.2% in April. This marks the first time inflation has hit or fallen below the ECB's 2.0% target since October. The ECB has already cut interest rates seven times since June of last year, and markets are now almost fully pricing in another rate cut at Thursday's meeting.

For the remainder of the year, money market traders are anticipating approximately 55 bps of easing, suggesting about one more quarter-point cut after the expected move this week.

Germany's 10-year yield was last up +0.4 bps at 2.527%. On Tuesday, it had reached its lowest point since 8th May, at 2.485%. Germany's policy-sensitive two-year yield rose by +0.7 bps to 1.805%, remaining within its recent narrow range. Conversely, on the longer end of the maturity spectrum, Germany's 30-year yield was down -1.6 bps on Wednesday, at 2.996%.

Germany's cabinet approved its initial tax relief package on Wednesday, valued at €46 billion through 2029.

The collapse of the Netherlands' government on Tuesday had little immediate impact on Dutch government bond markets. However, investors are now bracing for months of political uncertainty in one of the few remaining triple-A rated sovereign nations.

For the week, the German 10-year yield was -1.7 bps. Germany's two-year bond yield is -0.5 bps, and on the longer end of the curve, Germany's 30-year yield is -3.4 bps this week.

The spread between US 10-year Treasuries and German Bunds is now 183.2 bps, 10.3 bps lower than last week’s 193.5 bps.

On Wednesday, Italy's 10-year yield remained steady at 3.489%, after falling to its lowest since 28th February at 3.475% on Tuesday. The spread between Italy's 10-year yield compared to Germany's Bund yield stands at 96.2 bps, 2.4 bps lower than last week’s 98.6 bps spread. Italian bond yields, a benchmark for the eurozone periphery, are -4.1 bps this week.

Commodities

Gold spot +2.63% MTD and +28.31% YTD to $3,375.49 per ounce.

Silver spot +6.04% MTD and +18.56% YTD to $34.96 per ounce.

West Texas Intermediate crude +3.21% MTD and -12.47% YTD to $62.74 a barrel.

Brent crude +1.49% MTD and -13.04% YTD to $64.85 a barrel.

Gold prices are +2.63% this week. Gold prices edged up again on Wednesday, supported by a softer US dollar and weaker-than-expected economic data from the US, as investors navigated heightened economic and political uncertainty.

Spot gold climbed +0.47% on Wednesday to reach $3,375.49 per ounce, having risen by as much as 1% earlier in the day. The US dollar index registered a -0.35% decline, making gold more affordable for international buyers holding other currencies.

Gold had reached an unprecedented high of $3,500.05 in April and is still +28.31% YTD.

This week, WTI and Brent are +1.41% and -0.11%, respectively. Oil prices ended Wednesday’s trading session nearly one percentage point lower, influenced by a larger-than-expected build in US gasoline and diesel inventories. This increase in fuel supplies comes as OPEC+ plans further output increases. Escalating trade tensions continue to obscure the outlook for energy demand.

Brent crude futures settled down 74 cents, a -1.13% decrease, closing at $64.85 a barrel. Similarly, US WTI crude fell 61 cents, or -0.96%, to settle at $62.74.

Investor sentiment was also dampened by plans from OPEC+ producers to boost output by 411,000 barrels per day (bpd) in July. On Tuesday both benchmarks had increased by less than one percentage point to a two-week high, driven by concerns over potential supply disruptions and expectations that Iran, an OPEC member, might reject a US nuclear deal proposal crucial for easing sanctions.

Russia reported a 35% decline in its May oil and gas revenue. This significant reduction could make Moscow more resistant to further OPEC+ output hikes, as such actions typically exert downward pressure on crude prices.

Geopolitical tensions also continued to escalate. Russian President Vladimir Putin reportedly communicated to President Donald Trump the necessity of responding to high-profile Ukrainian drone attacks on Russia's nuclear-capable bomber fleet and a deadly bridge bombing, which Moscow attributes to Kyiv.

Canadian production operations that had been shut down due to wildfires began to restart on Wednesday. Canadian Natural Resources announced the resumption of operations at its Jackfish 1 oil sands site in northern Alberta, after assessing that regional wildfires were at a safe distance. Wildfires in Canada had reduced the country's oil output by approximately 344,000 bpd.

EIA weekly report. Last week, US crude oil stockpiles decreased as refineries boosted production in anticipation of the summer driving season. This was offset by an increase in fuel inventories, which rose due to weaker demand, according to data released Wednesday by the Energy Information Administration (EIA).

Crude inventories fell by 4.3 million barrels, settling at 436.1 million barrels in the week ending 30th May. This drop coincided with a significant increase in refinery activity; crude runs rose by 670,000 bpd, pushing utilisation rates up by 3.2 percentage points to 93.4% of total capacity.

Despite the start of the summer driving season, typically a period of higher fuel consumption following the Memorial Day holiday weekend, gasoline stocks increased by 5.2 million barrels to 228.3 million barrels. This rise was attributed to a decline in gasoline supplied (a key indicator of demand), which fell by 1.2 million bpd to 8.3 million bpd. The unexpected fall in demand has raised some concerns.

In addition to gasoline, distillate stockpiles, encompassing diesel and heating oil, also saw an increase, rising by 4.2 million barrels to reach 107.6 million barrels last week. Meanwhile, crude stocks at Cushing, Oklahoma, a major delivery hub, edged up by 576,000 barrels, and net US crude imports increased by 389,000 bpd.

Note: As of 5:00 pm EDT 4 June 2025

Key data to move markets

EUROPE

Thursday: German Factory Orders, Eurozone PPI, and ECB Monetary Policy Statement and Press Conference.

Friday: German Industrial Production, German Trade Balance, a speech by ECB President Christine Lagarde, and Eurozone Employment Change, GDP, and Retail Sales.

Saturday: Speeches by ECB President Christine Lagarde and ECB Executive Board member Isabel Schnabel.

Monday: Sentix Investor Confidence Survey.

UK

Thursday:.A speech by BoE External Member Megan Greene.

Saturday: A speech by BoE External Member Megan Greene.

Monday: BRC Like-for-like Retail Sales.

Tuesday: Average Earnings, Claimant Count Change, Claimant Count Rate, Employment Change, and ILO Unemployment Rate.

USA

Thursday: Initial and Continuing Jobless Claims, Nonfarm Productivity, Unit Labour Costs, and speeches by Fed Governor Adriana Kugler, Philadelphia Fed President Patrick Harker, and Kansas City Fed President Jeff Schmid.

Friday: Nonfarm Payrolls, Average Hourly Earnings, Labour Force Participation Rate, U6 Unemployment Rate, and Unemployment Rate.

Tuesday: NFIB Business Optimism Index.

Wednesday: CPI, Core CPI, and Monthly Budget Statement.

CHINA

Monday: CPI, PPI, Exports, Imports, and Trade Balance.

JAPAN

Sunday: Current Account and GDP.

Global Macro Updates

Tariff negotiations and its economic impact. US President Donald Trump announced last Friday that US steel and aluminium tariffs would be doubled to 50% and would take effect on 4 June. The doubling of tariffs comes after a federal court struck down some of the US administration’s other tariffs, stating that it was essentially illegal for the US President to try to put these in place under an emergency law. The tariffs on metals were not subject to that ruling. Although discussion with EU negotiators are, according to US trade representative Jamieson Greer, very constructive and indicate a willingness by the EU to work with the US to find a concrete way forward to achieve reciprocal trade’, this move has the potential to further strain the US’ relations with its fellow G7 members during the G7 Summit due to take place in Canada 15 - 17 June. In addition, despite there have been suggestions of a call between Washington and Beijing this week to further discuss the tariffs, President Donald Trump calling Chinese Premier Xi Jinping "VERY TOUGH, AND EXTREMELY HARD TO MAKE A DEAL WITH" in a late-night social media post, may have only inflamed tensions. US moves to restrict access to chipmakers and revoke Chinese students visas along with a continuing disagreement over rare earth metals and their export to the US, may mean that the further negotiations may be stalled, leaving investors and businesses uncertain about what will happen after the 90 day delay to the prior rounds of tariffs comes into effect.

As to the latest tariffs' direct impact on the US economy, they are likely to weigh heavily on the US aluminium market due to the lack of domestic capacity. The US imports roughly half of its aluminium, with Canada the biggest supplier, accounting for 58% of imports. The US also relies on Mexico and Canada for around 90% of its aluminium scrap imports. The US is already experiencing signs of a weakening economy with hiring slowing and services activity contracting. The latest ADP report showed private payrolls rose just 37,000 last month. This was the second month in a row when the figures were well below expectations. It was also the lowest level in two years, indicating that the labour market is starting to stall. This appears to be supported by other data out this week; ISM Services figures released on Wednesday dropped 1.7 points in May to 49.9 — below the 50 level that separates expansion and contraction. As noted by Bloomberg news, the services survey showed both the steepest contraction in new orders and the highest prices-paid index since late 2022, denoting a more pronounced impact on demand and inflation due to higher US duties on imports. In addition, the latest Federal Reserve’s Beige Book, released on Wednesday morning, indicated that economic activity has declined slightly over the past six weeks. All Districts reported elevated levels of economic and policy uncertainty, which have led to hesitancy and a cautious approach to business and household decisions. Hiring activity was mostly flat as business owners put off expansion plans due to elevated policy uncertainty and tariff-related cost pressures. Investors will be looking closely to Friday’s nonfarm payroll report for further indications of labour market softening.

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

Dieser Artikel wird Ihnen lediglich zu Informationszwecken zur Verfügung gestellt und er sollte nicht als Angebot oder Aufforderung zur Abgabe eines Kauf- oder Verkaufsangebots eines Investments oder einer damit zusammenhängenden Dienstleistung betrachtet werden, auf die hier möglicherweise Bezug genommen wurde. Der Handel mit Finanzprodukten birgt erhebliche Verlustrisiken und ist möglicherweise nicht für alle Anleger geeignet. Die Wertentwicklung in der Vergangenheit ist kein verlässlicher Indikator für die künftige Wertentwicklung.