Corporate Earnings News

Global market indices

Currencies

Cryptocurrencies

Fixed Income

Commodity sector news

Key data to move markets this week

Global macro updates

Corporate Earnings News

Corporate earnings calendar 18th July - 25th July 2024

Thursday: Netflix, Novartis, Abbott Laboratories, Blackstone, Taiwan Semiconductor Manufacturing, Intuitive Surgical, Marsh & McLennan, Cintas, D.R. Horton, PPG Industries, KB Financial, Domino’s Pizza, Snap-On, KeyCorp

Friday: American Express, SLB

Monday: Verizon

Tuesday: Alphabet, Microsoft, Tesla, Coca-Cola, General Electric Company, General Motors, Philip Morris International, Spotify, Visa

Wednesday: AT&T, IBM, Waste Management, Chipotle Mexican Grill, Ford Motor, Hilton Worldwide, Teledyne Technologies, Universal Music Group

Thursday: Amazon, AstraZeneca, Nestle, Hermes International, Union Pacific, Honeywell, Unilever, Sanofi, Starbucks, Stellantis, British American Tobacco, Keurig Dr Pepper, Dow, Baker Hughes, Martin Marietta Materials, Roku, Cemex, Hasbro

Global market indices

US Stock Indices Price Performance

Nasdaq 100 +3.64% MTD +21.23% YTD

Dow Jones Industrial Average +4.69% MTD +8.66% YTD

NYSE +3.81% MTD +11.03% YTD

S&P 500 +2.34% MTD +17.16% YTD

The S&P 500 -0.81% over the past week, with 10 of the 11 sectors having exhibited positive performance MTD. The Equally Weighted version of the S&P 500 posted a weekly +3.51%, its performance is +4.04% MTD +8.27% YTD.

The S&P 500 Financials is the leading sector this month so far, up +6.58% MTD +16.44% YTD, while the Communication Services sector has exhibited the weakest performance at -2.21% MTD +23.30% YTD.

This week the Real Estate sector outperformed within the S&P 500 with a +5.70% gain, followed by the Financials and Energy sectors at +4.64% and +4.33%, respectively. Conversely, the Communication Services sector underperformed, experiencing a -5.62% decline.

On Wednesday, US equity markets experienced a significant rotation, with the S&P 500 declining -1.4%. A significant fall in shares of the Magnificent Seven contributed to the Nasdaq's -2.8% decline, its largest single-day decrease since December 2022. Conversely, the Dow Jones Industrial Average achieved a fresh high, advancing +0.6%, while the Russell 2000 index of smaller companies contracted by -1.1%. Wall Street's "fear gauge," the VIX, reached its highest level since early May.

This activity underscores the pronounced rotation that has characterised investor behaviour over the past week. It marked the first instance since 1999 in which the Dow Jones Industrial Average recorded a gain while the S&P 500 fell by more than 1%, according to Dow Jones Market Data.

It appears that investors are now assessing the potential for further declines in big tech following a stellar performance that propelled the Nasdaq up nearly +20% YTD. We are seeing reduced positions in this year's top performers and shifted investments towards smaller, undervalued companies, anticipating their potential to benefit from lower interest rates, a prospect bolstered by encouraging inflation data.

Additional concerns centre on the possibility of increased US trade restrictions on semiconductor manufacturers, irrespective of the outcome of the November presidential election. This has contributed to a -7.1% decline in the iShares Semiconductor ETF, its most significant decline since March 2020.

Simultaneously, investors have sought refuge in sectors perceived as undervalued, with the SPDR Portfolio S&P 500 Value ETF reaching a record high after nine consecutive sessions of gains. Energy, financial, and real estate companies also demonstrated positive performance at Wednesday’s close.

US stocks

Mega caps: A negative week for the ‘Magnificent Seven’ due to rotation away from the AI trade, and into small and mid-cap companies, as well as more defensive sectors. Alphabet -5.31%, Amazon -5.94%, Apple -1.76%, Meta Platforms -13.60%, Microsoft -4.88%, Nvidia -12.54%, and Tesla -5.61%.

Energy stocks reflected a positive performance this week, as the Energy sector itself was +4.33%, enhancing the sector’s YTD performance to +11.46%. Apa Corp (US) +11.99%, Halliburton +10.12%, Baker Hughes +6.86%, ExxonMobil +5.11%, Phillips 66 +5.05%, Chevron +3.93%,ConocoPhillips +3.15%, Occidental Petroleum +2.83%, and Marathon Petroleum +2.08%, while Shell -1.22%.

Shell: First gas achieved at Jerun gas field in Malaysia. SapuraOMV Upstream, the operator of the Jerun field in Malaysia, has formally announced the commencement of gas production. Shell, through its Malaysian subsidiary Sarawak Shell Berhad, holds a 30% equity stake in the field and finalised its investment decision for the development in 2021.

Situated approximately 160 kilometres (km) northwest of Bintulu and 190 km northwest of Miri in Sarawak, Malaysia, the Jerun field features an integrated central processing platform. Gas will be exported via a newly constructed 80-km pipeline to the E11RB production hub, facilitating onward delivery to customers in Bintulu, including Malaysia LNG. The Jerun platform is engineered for a peak production capacity of 550 million cubic feet of gas per day, along with 15,000 barrels of condensate per day. Jerun is operated by SapuraOMV Upstream (40%) in partnership with Sarawak Shell Berhad (30%) and PETRONAS Carigali (30%).

Materials and Mining stocks had a positive week, as the materials sector was +3.85%, elevating the sector’s YTD performance to +7.23%. Mosaic +14.09%, Nucor +6.94%, Newmont Corporation +6.18%, CF Industries +4.47%, Yara International +3.06%, while Freeport-McMoRan -5.99%, Albemarle -2.93%, and Sibanye Stillwater -2.44%.

CF Industries collaborating on low-carbon ammonia fertiliser with POET. CF Industries, and POET, the world's largest biofuel producer, have announced a collaborative pilot project aimed at utilising low-carbon ammonia fertiliser to decrease the carbon footprint of corn production and ethanol. This initiative aligns with the anticipated surge in demand for lower-carbon intensity ethanol, driven by increasingly stringent low-carbon fuel standards.

While ammonia is widely used as a fertiliser in US corn production, its conventional production process is a significant source of emissions. By employing low-carbon ammonia in corn cultivation, the carbon intensity of ethanol can be reduced by up to 10%. The companies plan to initiate the first applications of low-carbon ammonia in the fall of 2024, with subsequent applications in the spring of 2025, aiming for the first harvest in the fall of 2025.

European Stock Indices Price Performance

Stoxx 600 +0.67% MTD +7.48% YTD

DAX +1.11% MTD +10.06% YTD

CAC 40 +1.22% MTD +0.37% YTD

IBEX 35 +1.48% MTD +9.93% YTD

FTSE MIB +3.70% MTD +13.27% YTD

FTSE 100 +0.29% MTD +5.87% YTD

This week, the pan-European Stoxx Europe 600 index declined -0.31%, closing at 514.83.

Germany's DAX index was +0.16% and closed at 18,437.30. France's CAC 40 index was -0.04%, closing at 7,570.81.

The UK's FTSE 100 index declined to 8,187.46, reflecting a -0.07% loss for the week.

In Wednesday's trading session, the Technology sector experienced the most significant decline, primarily due to reports that the US is considering imposing stringent trade restrictions if companies like ASML continue providing China with access to advanced semiconductor technology. ASML's Q2 earnings, while exceeding estimates, revealed Q3 revenue guidance below expectations, further contributing to its losses.

The Retail sector also faced substantial losses, particularly among high-end and luxury brands. This was prompted by a series of profit warnings and underwhelming Q2 results, which highlighted softening demand in China as a detriment to profitability. Mergers and acquisitions within the sector also garnered attention, as EssilorLuxottica announced the acquisition of US streetwear brand Supreme for $1.5 bn in cash.

Conversely, Adidas demonstrated relative outperformance after raising its annual profit target for the second time in three months, supported by better-than-expected Q2 results. However, the Automobiles & Parts and Industrial Goods & Services sectors faced pressure, particularly following Daimler Truck Holding’s preliminary Q2 earnings, which revealed a significant EBIT miss and an ongoing review of its full-year guidance.

In the Healthcare sector, Roche Holding shares gained traction after disclosing promising early-stage study results for its experimental weight-loss pill, positioning the company as a late entrant in the race to develop obesity drugs.

Defensive sectors such as Telecom, Food & Beverage, and Utilities emerged as the top performers amid a flight to safety. Utilities were further bolstered by Spain's announcement of a new $2.5 billion plan to support green hydrogen and renewable industries.

European corporate deleveraging: A catalyst for increased dividends, buybacks, and M&A? A recent Bloomberg report suggests that Europe's largest corporations have the capacity to increase dividend payouts, expand share buyback programs, and engage in mergers and acquisitions (M&A) activity due to a significant reduction in financial leverage. Citing data compiled by Bloomberg Intelligence, the net debt-to-EBITDA ratio for Euro Stoxx 50 companies is projected to decline to 0.76x, marking its lowest level since 2008 and representing just over half of the ratio from four years ago.

This improvement in balance sheets, attributed to increased cash flow generation, could be utilised for dividends or share buybacks. Strategists have noted that European firms increasingly favour buybacks as a means of returning cash to shareholders, a trend that has bolstered major European equity markets. Goldman Sachs research indicates that financial and energy companies account for half of the overall buyback activity. Some analysts speculate that the preference for buybacks over dividends stems from their greater flexibility.

Bloomberg's analysis predicts that European buybacks will exceed €50 billion, surpassing the initial estimate of €35 billion at the start of the year, although still below last year's €72 billion. Despite this, some sell-side analysts have suggested the potential for a record-breaking year, though French companies may underperform in this regard due to prevailing political uncertainty.

Other Global Stock Indices Price Performance

MSCI World Index +2.21% MTD +14.97% YTD

Hang Seng +0.12% MTD +4.06% YTD

This week, the Hang Seng Index increased by +1.54%, while the MSCI World Index contracted by -0.51%.

Currencies

EUR +2.17% MTD -0.88% YTD to $1.0936

GBP +2.87% MTD +2.17% YTD to $1.3008

The euro was +1.01% against the USD over the past week, while the British Pound was +1.26%. The Dollar Index is -1.24% this week, -2.00% MTD, and +2.38% YTD.

The euro, reaching a four-month peak in Wednesday’s session, rose +0.35% to $1.0936.

Additionally, on Wednesday, the Japanese yen reached a six-week high, prompting speculation of official intervention. The yen rose 1.38% to reach ¥156.16 per dollar on Wednesday. Data from the BoJ's money market operations suggested potential intervention by authorities, with nearly ¥6 trillion possibly purchased in the previous week. Market participants noted that the recent yen movements bore the characteristics of further intervention or, at minimum, reflected markets being unsettled by such a prospect.

The magnitude of the yen’s appreciation likely caught traders off-guard, prompting a reassessment or unwinding of positions. Notably, net short positions on the yen were near a 17-year high last week. The yen remains the weakest performing G10 currency against the dollar this year, having depreciated by more than 9%.

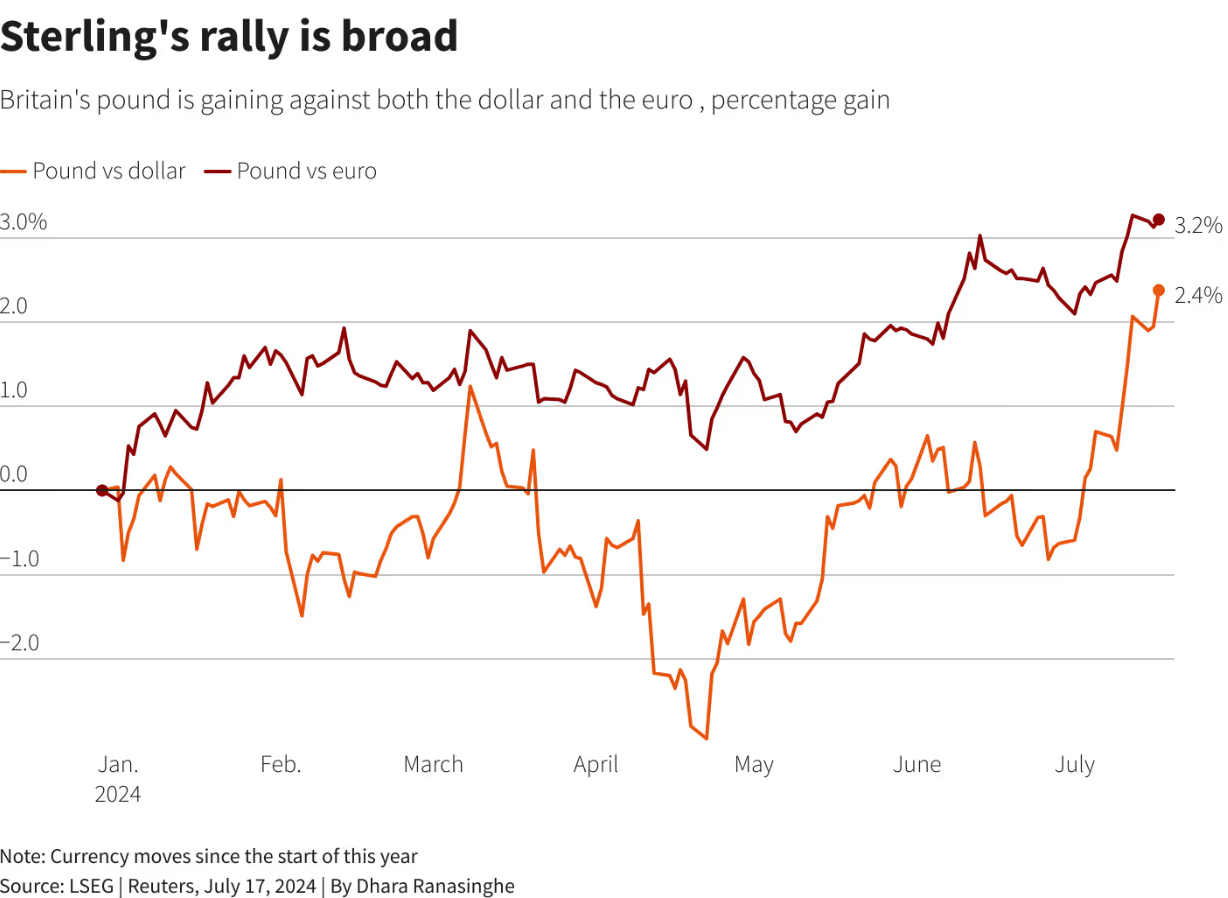

Sterling soars to one-year high amidst global interest rate shifts. The British pound climbed +0.28% to $1.3008, reaching a one-year high on Wednesday, propelled by investors seeking higher returns amidst a global decline in interest rates.

UK inflation services inflation held steady at 5.7% for the second straight month, leading traders to reassess expectations of an August rate cut and pushing the pound above $1.30 for the first time since July 2023.

In contrast to the euro and even the dollar, the pound has remained resilient to domestic political fluctuations. Instead, it has benefited from a new government, which is expected to bring some degree of stability.

On Wednesday, King Charles outlined Prime Minister Keir Starmer's economic revitalisation plans, emphasising new housing and infrastructure projects.

Economic growth in Britain has also shown signs of improvement. On Tuesday, the IMF revised its UK growth forecast upwards to 0.7% for the current year, exceeding its April projection of 0.5%.

A core factor driving Sterling’s recent appreciation is the expectation that British interest rates will remain elevated for a longer duration compared to other regions. The BoE and the Fed are among the few central banks yet to initiate rate cuts, although recent signals suggest September as a potential starting point for US rate reductions. However, the new government has suggested that there would be a significant increase in the country’s minimum wage. This increase in costs for businesses may make sticky services inflation even stickier and could make it harder for the Bank of England to cut rates. This would also affect employment and would dampen longer-term growth.

The pound's rally has been widespread, even pushing the euro to a two-year low of 83.93 pence on Wednesday. Year-to-date, the pound has appreciated by 2.3% against the dollar, leading major currencies, while the euro remains down 1%.

Following on from Wednesday’s CPI release, market expectations for a BoE rate cut at its 1st August meeting have diminished, with less than a 40% probability of a rate cut, compared to around 50% on Tuesday.

UK interest rates are projected to end the year around 4.75%, down from the current 5.25%. This would still exceed US rates, which are anticipated to range between 4.50% and 4.75%, and eurozone rates, which are priced at roughly 3.30%.

Cryptocurrencies

Bitcoin +7.99% MTD +55.15% YTD to $65,149.00.

Ethereum +2.20% MTD +50.23% YTD to $3,449.30.

Bitcoin and Ethereum have been in positive territory over the past week, gaining +12.81% and +11.20%, respectively. Both have benefited from signals that the Fed is getting closer to initiating rate cuts in September. Bitcoin surged following the assassination attempt on former President and Republican nominee Donald Trump. He appears to be a supporter of cryptocurrencies, having attended crypto conferences and his campaign has also accepted donations in cryptocurrency.

The competition for potential Ether ETF assets has intensified, even prior to the official launch of these funds. Major issuers such as BlackRock, Fidelity, Invesco, and Bitwise recently filed paperwork with the Securities and Exchange Commission, outlining their proposed fees for their respective Ether ETFs, which would directly hold the second-largest cryptocurrency. These filings were submitted in anticipation of the funds' potential launch on 23 July pending final regulatory approval.

BlackRock announced a 0.25% fee for its upcoming product, with a reduction for the initial 12 months or until $2.5 billion in assets are accumulated. Fidelity also disclosed a 0.25% fee, waived through the end of the year without any asset limit. Crypto-native firms 21Shares and Bitwise proposed fees of 0.21% and 0.2%, respectively, with additional incentives included.

The proposed fees range from as low as 0.19% by Franklin Templeton to 2.5% by Grayscale, which aims to convert an existing fund into an Ether ETF while potentially launching another version with a lower expense ratio.

Seven of the ten forthcoming ETFs are offering fee waivers, with some waiving fees entirely for durations ranging from six to ten months. This demonstrates the anticipated competitiveness among issuers and the impending battle for asset accumulation.

Many of these issuers had previously undergone a similar process with their Bitcoin ETFs, which launched earlier this year. These Bitcoin ETFs garnered significant attention upon their debut in January and have collectively attracted a net inflow of $16.5 billion, according to data compiled by Bloomberg.

Note: As of 5:00 pm EDT 17 July 2024

Fixed Income

US 10-year yield -24.1 basis points MTD +28.0 basis points YTD to 4.161%.

German 10-year yield -7.8 basis points MTD +41.4 basis points YTD to 2.408%.

UK 10-year yield -9.8 basis points MTD +54.0 basis points YTD to 4.069%.

US Treasury 10-year bond yields -13.2 basis points (bps) this week, reaching 4.161%.

US Treasury yields reached a four-month low on Wednesday, following statements from Federal Reserve officials indicating progress in curbing inflation towards their 2% target. This development has increased the likelihood of a first interest rate cut in September.

The yield on 10-year Treasury notes decreased by -0.2 bps to 4.161%, marking the lowest level since 13th March. Similarly, the yield on 2-year Treasury notes declined by -1.6 bps to 4.430%.

The Treasury Department experienced strong demand for a $13 billion sale of 20-year bonds on Wednesday, with a high yield of 4.466%, closely aligned with pre-auction trading levels. The bid-to-cover ratio reached 2.68x.

Additionally, the Treasury is scheduled to auction $19 billion in 10-year TIPS on Thursday.

The German 10-year yield was -11.3 bps this week, while the UK 10-year yield was -5.4 bps this week. The spread between US 10-year Treasuries and German Bunds currently stands at 173.8 bps, -1.9 bps from last week.

Italian bond yields, a benchmark for the eurozone periphery, were -15.0 bps this week to 3.717%. Consequently, the spread between Italian and German 10-year yields contracted -3.7 bps to 129.4 bps from 133.1 bps last week.

Eurozone bond yields remained stable on Wednesday, poised for their most substantial weekly decline in a month, ahead of today’s ECB meeting. The yield on the German 10-year bond remained unchanged at 2.425%, having previously reached its lowest point in three weeks earlier in the day.

France's 10-year bond yield was down -1.5 bps at 3.078%, however, on a weekly basis, it dropped -11.4 bps from 3.192. The spread between French and German yields fell to its lowest since 13th June at 65.5 bps.

Commodities

Gold spot +5.79% MTD +19.39% YTD to $2,462.40 per ounce.

Silver spot +2.76% MTD +26.12% YTD to $30.38 per ounce.

West Texas Intermediate crude -2.68% MTD +12.13% YTD to $80.61 a barrel.

Brent crude+0.09% MTD +10.44% YTD to $85.08 a barrel.

Spot gold prices are +3.80% this week. Gold prices reached an all-time high on Wednesday, propelled by increasing optimism for an interest rate reduction by the Fed in September and a weakening US dollar, which collectively stimulated demand.

However, spot gold subsequently experienced a modest decline of approximately -0.6%, attributed to profit-taking following its record-breaking high of $2,482.29 earlier in the session.

The US Dollar Index depreciated by approximately -0.5%.

WTI is -3.33% this week, while Brent is flat. Oil prices were approximately +2% on Wednesday, driven by a larger-than-anticipated weekly decline in US crude inventories and a weakening US dollar, which offset concerns over slower economic growth in China.

On Tuesday, both Brent and West Texas Intermediate (WTI) crude oil benchmarks had closed at their lowest levels since mid-June. The price differential between Brent and WTI narrowed to approximately $3.65 per barrel, the smallest margin since October 2023. This reduced spread diminishes the incentive for energy companies to transport crude oil to the US for export purposes.

According to the US Energy Information Administration, energy companies withdrew 4.9 million barrels of crude oil from storage during the week ending 12th July. This figure exceeded the 4.4 million barrel drop reported by the American Petroleum Institute.

In US refining news, both diesel and crack spreads, indicators of refining profit margins, reached their lowest levels since December 2021 and January 2024, respectively.

The depreciation of the US Dollar Index, which fell to a 17-week low, also contributed to the upward pressure on oil prices.

Note: As of 5:00 pm EDT 17 July 2024

Key data to move markets this week

EUROPE

Thursday: ECB Main Refinancing Operations Rate, Rate on Deposit Facility, Monetary Policy Statement, and Press Conference, and Eurogroup Meeting.

Friday: German PPI.

Monday: Deutsche Bundesbank Monthly Report, German Retail Sales, and Eurogroup meeting.

Tuesday: Eurozone Consumer Confidence Indicator and Eurogroup meeting.

Wednesday: Eurozone HCOB Composite, Manufacturing and Services PMIs, German HCOB Composite, Manufacturing and Services PMIs, French HCOB Composite, Manufacturing and Services PMIs, and German Gfk Consumer Confidence.

Thursday: German IFO Business Climate, Current Assessment and Expectations Surveys, and Eurogroup Meeting.

UK

Thursday: Employment Change, ILO Unemployment Change, Average Earnings, Claimant Count Change, and GfK Consumer Confidence.

Friday: Retail Sales.

Wednesday: S&P Global/CIPS Composite, Manufacturing and Services PMIs.

US

Thursday: Initial and Continuing Jobless Claims, Philadelphia Fed Manufacturing Survey, Existing Homes Sales, and speeches by San Francisco Fed President Mary Daly, Dallas Fed President Lorie Logan, and Fed Governor Michelle Bowman.

Friday: Speeches by New York Fed President John Williams and Atlanta Fed President Raphael Bostic.

Monday: Chicago Fed National Activity Index.

Tuesday: Existing Home Sales.

Wednesday: S&P Global Composite, Manufacturing and Services PMIs, and New Home Sales.

Thursday: GDP, Personal Consumption Expenditures (PCE) Prices, Core PCE, Initial and Continuing Jobless Claims, Durable Goods Orders, and Nondefense Capital Goods Orders ex Aircraft.

JAPAN

Thursday: National CPI, and National Core CPI.

Thursday: Tokyo Consumer Price Index (CPI), Tokyo Core CPI.

CHINA

Monday: PBoC Interest Rate Decision.

Global Macro Updates

Fedspeak suggests closer to potential rate cut as inflation shows signs of easing. Federal Reserve Governor Waller stated on Wednesday that while he would prefer to see more evidence of inflation progressing towards the 2% target, he believes the Fed is nearing the point where an interest rate cut would be justified. Waller also noted that the upside risk to unemployment is higher than it has been in an extended period.

New York Fed President John Williams, a voting member of the Federal Open Market Committee (FOMC), indicated that inflation data suggest the Fed is approaching the desired disinflationary trend. However, Williams expressed a need for further assurance that inflation is sustainably moving towards the 2% target.

Richmond Fed President Thomas Barkin, also a voting member of the FOMC, said he wanted to "proceed deliberately" on interest-rate moves because it was not clear how much the current level of interest rates was slowing the economy.

Although officials, including Fed Chair Jerome Powell earlier this week, refrained from explicitly stating that a July rate cut is under consideration, financial markets are currently pricing in a 100% probability of a rate cut by September, following last week's data indicating a cooling of both inflation and the labour market.

BoE rate cut prospects dwindle as UK inflation defies expectations. UK inflation remained largely unchanged in June, exceeding estimates. The Consumer Price Index (CPI) held steady at 2.0% y/o/y, surpassing the consensus forecast of 1.9%, while core inflation stood at 3.5%, slightly above the 3.4% projection. Services prices remained at 5.7%, above the 5.6% consensus. Restaurants and hotels contributed most significantly to upward pressure, while clothing and footwear exerted downward pressure. These figures align with anecdotal reports suggesting that sporting and cultural events might sustain inflation in June and July.

The persistence of underlying inflation follows the IMF’s warning on Tuesday that the BoE interest rate cuts could be hindered by stubbornly high inflation, particularly in the services sector. Additionally, faster-than-expected economic growth and surveys indicating firm wage growth amid renewed hiring are complicating the disinflation process. The BoE had previously anticipated inflation to ease between April and July before rising again to stabilise around 2.5% by year-end and subsequently falling back to target in 2025.

Market expectations for a BoE rate cut in August have diminished, with the probability now reduced to 25%, down from 50% prior to the inflation update.

Details from the BoE's June policy meeting hinted at a growing number of policymakers leaning towards a rate cut, following the 5-2 vote to maintain the current stance. Nevertheless, recent comments from BoE officials have been cautious, with Chief Economist Pill and MPC members Haskel and Mann expressing concerns about services prices and persistently high wages. Only long-standing dove Dhingra has emphasised that the economy is not expanding sufficiently to reignite inflationary pressures.

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

Dieser Artikel wird Ihnen lediglich zu Informationszwecken zur Verfügung gestellt und er sollte nicht als Angebot oder Aufforderung zur Abgabe eines Kauf- oder Verkaufsangebots eines Investments oder einer damit zusammenhängenden Dienstleistung betrachtet werden, auf die hier möglicherweise Bezug genommen wurde. Der Handel mit Finanzprodukten birgt erhebliche Verlustrisiken und ist möglicherweise nicht für alle Anleger geeignet. Die Wertentwicklung in der Vergangenheit ist kein verlässlicher Indikator für die künftige Wertentwicklung.