Is tech euphoria ignoring consumer fragility?

Key data to move markets today

JAPAN: National CPI

EU: German GDP, German GfK Consumer Confidence, Eurozone EcoFin Meeting, Eurogroup Meeting, Eurozone Negotiated Wage Rates, German IFO Business Climate, Current Assessment and Expectations Surveys and a speech by ECB Chief Economist Philip Lane

UK: GfK Consumer Confidence and Retail Sales

US: Michigan Consumer Expectations Index, Michigan Consumer Sentiment Index, UoM 1 and 5-year Inflation Expectations, Fed Chair Kevin Warsh swearing in ceremony and a speech by Fed Governor Christopher Waller

Global Macro Updates

US activity diverges as price pressures re‑accelerate. US data for May point to a widening divergence between a buoyant manufacturing sector and a slowing services economy, set against a renewed flare‑up in price pressures. The flash S&P Global Manufacturing PMI rose to 55.3 from 54.5 in April, beating the 53.8 consensus and marking a 48‑month high. The Services PMI slipped to 50.9 from 51.0, undershooting expectations of 51.8 and signalling only marginal expansion. However, factory strength continues to rely partly on precautionary stock‑building, as order growth, especially for exports, remains constrained by Middle East–related uncertainty.

Supply‑side frictions intensified, with war‑related disruptions driving the sharpest supplier delays since August 2022. Input costs and selling prices rose to their highest levels since mid‑2022, led by energy and goods inflation and amplified by tariffs and inventory rebuilding. The sectoral split is also evident in the labour market: services firms are accelerating job cuts in response to weaker demand and rising costs, whereas manufacturing reported its strongest hiring pace in 11 months as order books improved.

Broader activity indicators sent mixed signals. Initial jobless claims remained low at 209,000, with the four‑week average easing to 202,500 and continuing claims at 1.782 million, underscoring ongoing labour‑market resilience. By contrast, the Philadelphia Fed manufacturing index fell sharply to -0.4 from 26.7, its weakest since late 2025, with new orders dropping to -1.7 and shipments to 4.9, even as the prices‑paid index moderated to 47.9 from 59.3 and prices‑received fell to 26.3 from 33.5. Housing data came in firmer: April housing starts printed 1.465 million (down 2.8% m/o/m but above the 1.410 million consensus), while building permits rose 5.8% m/o/m to 1.442 million, suggesting construction remains a relative bright spot despite higher rates.

Eurozone and UK signal synchronised slowdown. Eurozone and UK business surveys for May point to a sharp deterioration in economic momentum as geopolitical shocks increasingly disrupt supply chains, raise input costs and weaken corporate confidence. The S&P Global Flash Eurozone Composite PMI for May dropped to 47.5, its lowest level in 31 months, undershooting expectations of 51.6. It reinforces that the economic fallout from the Iran war is intensifying rather than stabilising. France remains the focal point of weakness in the eurozone. Its composite PMI plunged to 43.5, a post‑pandemic low, as both manufacturing and services deteriorated on the back of surging energy costs and rising economic anxiety. Germany offered only marginal relief; despite a small uptick to 48.6, its composite PMI stayed in contractionary territory, accompanied by falling new orders and the fastest job shedding in over eighteen months.

Inflationary pressures re‑accelerated across the bloc, with input costs rising at the quickest pace in three and a half years and selling prices reaching a 38‑month high. Supplier delays have lengthened to their worst levels since 2022, suggesting further upward pressure to inflation. The data present a policy dilemma for the ECB, which is expected to raise rates in June despite rapidly weakening activity.

In the UK, the S&P Global Flash UK Composite PMI fell sharply to 48.5, signalling the first GDP contraction in over a year. Services drove the decline with the sector’s PMI reaching 47.9, hit by softer investment, delayed travel spending and heightened political uncertainty. Manufacturing gained some support from precautionary stockpiling, accelerating to a 3-month high of 52.4, though this is unlikely to persist. Price pressures remain elevated and business optimism has fallen to a one‑year low, reinforcing expectations that the BoE will maintain a cautious policy stance next month.

US Stock Indices

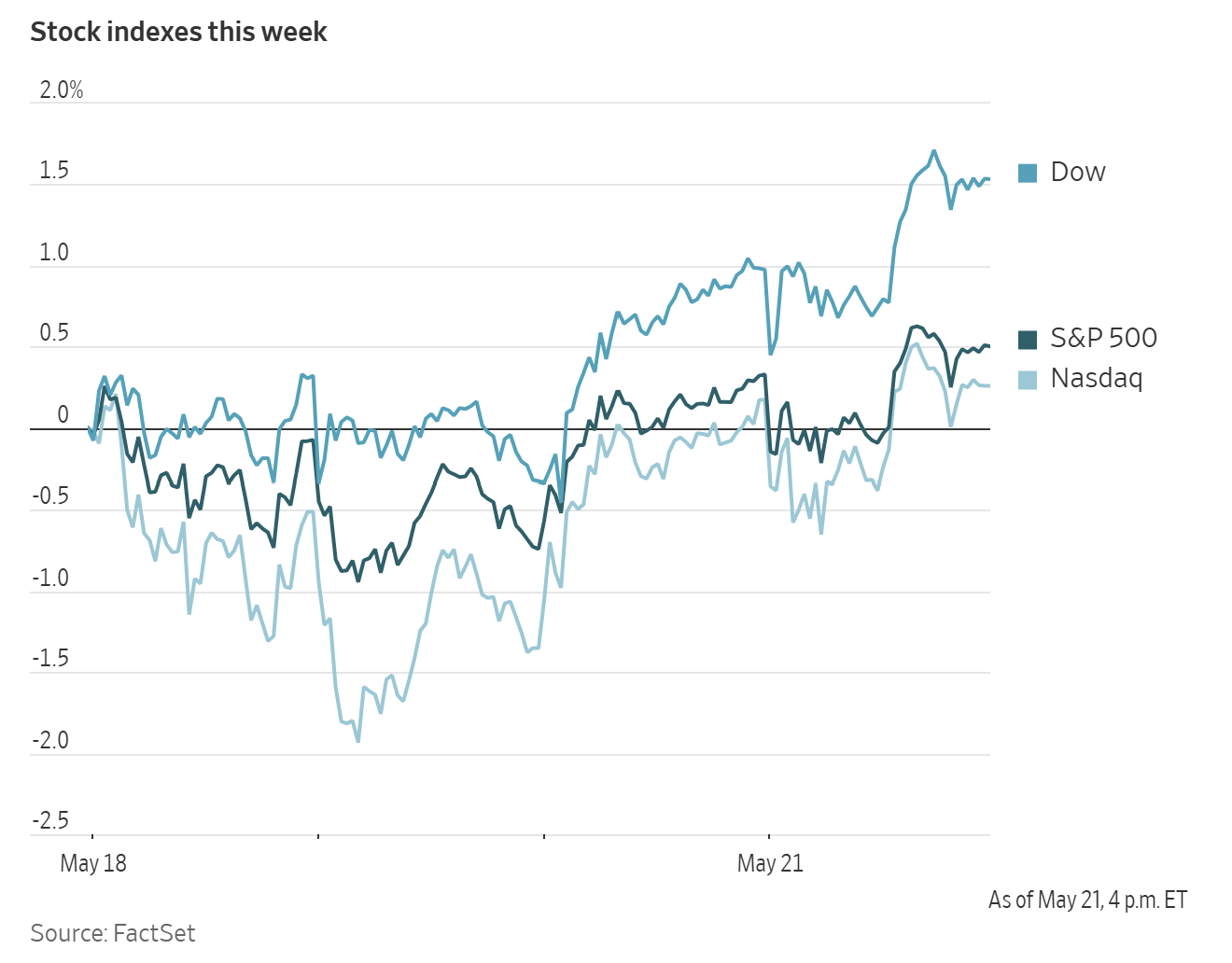

Dow Jones Industrial Average +0.55%

Nasdaq 100 +0.20%

S&P 500 +0.17%, with 8 of the 11 sectors of the S&P 500 up

Space exploration and quantum computing have emerged as the latest focal points for investor enthusiasm, offering a narrative that contrasts sharply with concerns over US consumer weakness and the uncertain trajectory of Washington - Tehran diplomacy.

On Thursday IBM shares rose +12.43% as the Trump administration agreed to provide $1 billion to IBM to support the construction of a foundry for quantum computing chips, as part of a broader effort to strengthen US leadership in this emerging industry. This helped drive the Dow Jones Industrial Average to its first record close since 10 February. In contrast, Walmart was the weakest performer in the blue-chip index, falling -7.27% after the retailer projected Q2 earnings slightly below expectations and indicated that elevated gasoline prices were placing pressure on some consumers.

The Nasdaq Composite was +0.09%, or 22.74 points to 26,293.10 on Thursday. The S&P 500 was +0.17%, or 12.75 points to 7,445.72. The Dow Jones was +0.55%, or 276.31 points, to 50,285.66.

In corporate news, Take-Two Interactive Software announced that Grand Theft Auto VI will be released on 19 November, a title widely expected to rank among the largest launches in video game history.

Estee Lauder and Spanish company Puig Brands have terminated discussions on a multibillion-dollar transaction that would have created one of the world’s largest beauty businesses.

To keep pace with the increasing demand for AI infrastructure, AMD is preparing a substantial investment, exceeding $10 billion, in Taiwan's semiconductor industry.

S&P 500 Best performing sector

Utilities +1.03%, with Vistra +3.53%, NRG Energy +2.19% and PPL +2.06%

S&P 500 Worst performing sector

Consumer Staples -1.63%, with Walmart -7.27%, Conagra Brands -2.76% and Kroger -2.34%

Mega Caps

Alphabet -1.37%, Amazon +1.30%, Apple +0.91%, Meta Platforms +0.38%, Microsoft -1.97%, Nvidia -1.77% and Tesla +0.14%

Information Technology

Best performer: Enphase Energy +17.29%

Worst performer: Intuit -20.02%

Materials and Mining

Best performer: Eastman Chemical +3.60%

Worst performer: LyondellBasell Industries -1.71%

Corporate Earnings Reports

Posted on Thursday, 21 May from The Pulse, our real-time AI-driven news tool. Available exclusively on the EXANTE Web Platform

Deere & Company reported Q2 2026 earnings. EPS reached $6.55 versus $5.10 expected and net income totaled $1.77bn versus $1.54bn expected. Production and Precision AG net sales came in at $4.50bn versus $4.66bn expected while Construction and Forestry net sales were $3.79bn versus $3.44bn expected. Small Ag and Turf net sales totaled $3.49bn versus $3.42bn expected. The company maintained full-year net income guidance of $4.5bn to $5.08bn versus $4.79bn expected and recorded a $272mn recovery for refund claims related to IEEPA tariffs. Deere CEO said our performance in the current market environment demonstrates the strength of our diversified portfolio. As we address ongoing challenges within global agricultural markets.

NIO reported earnings before the open achieving its second consecutive triple beat after multiple years of shortfalls. BofA reiterated its Neutral rating while raising the price target to $6.80 citing improving margins and a stronger model pipeline as key drivers of potential earnings upside.

Webull reported Q1 2026 revenue of $159.9mn up +36% y/y with GAAP EPS of ($0.04) and adjusted EPS of $0.03. Customer assets reached a record $24bn growing +90% y/y. Net deposits increased over +91% y/y. Registered users rose to 27.6mn up +15% y/y and funded accounts grew to 5.1mn up +8% y/y. Equity notional volume surged +104% y/y to $261bn while options volume climbed +31% y/y to 159mn and DARTs grew +42% y/y to 1.3mn. FINRA approved self and correspondent clearing capabilities expansion was secured across all European Economic Area countries, the app launched in Germany and AI-enabled research tools were rolled out. Chief Executive Anthony Denier said he is proud to report a strong start to the second year as a public company with meaningful progress in enhancing the platform.

Zoom reported first quarter results with revenue of $1.24bn, up +5.5% y/y. GAAP EPS came in at $1.42 and adjusted EPS at $1.55. AI Companion paid users grew +184% y/y while My Notes reached 1.5mn licensed users in four months. Zoom Customer Experience posted high double-digit growth, customers above $100k annual revenue rose +8.2% and enterprise net dollar expansion improved to 99%. GAAP operating margin expanded +450bps y/y. The company raised its stock repurchase authorization by an additional $1.0bn with total cash, cash equivalents and marketable securities reaching $7.7bn. CEO Eric Yuan stated that customers are increasingly adopting Zoom as an AI-first system of action.

Workday reported first quarter results with subscription revenue of $2.354 billion, up 14%, professional services revenue of $188 million, and total revenue of $2.542 billion, up 13%. The 12-month subscription revenue backlog, or cRPO, reached $8.81 billion, growing 15.5%, driven by continued customer expansion and AI solutions. Workday CEO stated that the company had a great Q1 making clear that Workday is ready for this AI moment with a strong core business and working AI strategy.

Take-Two Interactive Software reported Q4 2026 earnings. The company reaffirmed that Grand Theft Auto VI is scheduled to launch on November 19, with marketing expected to begin this summer. It projects net bookings of $8 billion to $8.2 billion, largely driven by GTA 6, while noting higher costs related to development, mobile releases, and marketing. The firm highlighted a pipeline of around 30 upcoming games. It plans to launch 6 titles during fiscal 2027 in addition to GTA VI and expects to release 22 titles throughout fiscal 2028 and 2029.

Copart reported Q3 FY2026 results with revenue up +2.1% y/y to $1.2bn, gross profit up +3.7% y/y to $572.6mn, net income fell -1.0% y/y to $402.4mn, and diluted EPS rose +2.4% y/y to $0.43.

Ross Stores reported first quarter earnings after the close. The results surpassed expectations with broad-based strength across the business. Ross Stores CEO stated we achieved outstanding sales and earnings results in the first quarter. Momentum was solid throughout the quarter with customer traffic as the primary driver of the strong sales trend.

European Stock Indices

CAC 40 -0.39%

DAX -0.53%

FTSE 100 +0.11%

Commodities

Gold spot +0.02% to $4,544.10 an ounce

Silver spot +1.09% to $76.70 an ounce

West Texas Intermediate -1.09% to $98.00 a barrel

Brent crude -0.53% to $104.92 a barrel

Gold prices were relatively unchanged on Thursday.

Spot gold was up +0.02% at $4,544.10 per ounce, after falling one percent earlier in the session.

Spot silver prices advanced +1.09% at $76.70 per ounce.

Oil prices were volatile on Thursday and ultimately settled slightly lower, as uncertainty surrounding prospects for resolving the conflict with Iran weighed on the market.

In a volatile session on Thursday, Brent crude futures settled at $104.92 per barrel, down $0.56, or -0.53%, while US WTI crude futures closed at $98.00 per barrel, down $1.08, or -1.09%. Both contracts finished at their lowest levels in nearly two weeks.

Earlier in the session, prices had risen by as much as four percent after Reuters reported that Iran's supreme leader had issued a directive that undermined hopes for a swift resolution to the conflict, before reversing course later in the day.

The Reuters report, which cited two senior Iranian sources, indicated that Tehran is adopting a firmer position on a key US demand. The directive from Supreme Leader Ayatollah Mojtaba Khamenei could further complicate negotiations.

Later on Thursday, Trump said the US would eventually recover Iran's stockpile of highly enriched uranium, which Washington believes is intended for use in a nuclear weapon.

These developments followed Iran’s announcement a day earlier of a new 'Persian Gulf Strait Authority,' which would oversee a 'controlled maritime zone' in the Strait of Hormuz.

Oil price gains accelerated after US Secretary of State Marco Rubio said that a proposed tolling system in the strait would render a diplomatic agreement unfeasible. Prices later pared those gains after he added that Pakistani officials, acting as mediators, would travel to Iran for talks.

Iran warned against further attacks and announced measures to reinforce its control over the strait, which remains largely closed.

Reuters, citing OPEC+ delegate sources, reported that the group is likely to approve a combined quota increase of 188,000 barrels per day (bpd) among the OPEC-7 when it meets on 7 June.

International Energy Agency Executive Director Fatih Birol said on Thursday that the onset of peak summer fuel demand, combined with the absence of new oil exports from the Middle East and declining inventories, could push the oil market into the 'red zone' in July and August.

Multiple reports, data releases and analyst assessments pointed to accelerating draws in global crude and refined-product inventories as the market moves toward peak summer demand.

Sultan Al Jaber, Chief Executive Officer of Abu Dhabi National Oil Company (ADNOC), said that even if the Middle East conflict were to end immediately, full oil flows through the Strait of Hormuz would not resume before Q1 or Q2 of 2027.

In a separate development, Ukraine struck Russia’s Syzran oil refinery overnight, a facility owned by Rosneft. Ukrainian military officials said it was the eleventh Russian refinery targeted this month.

Note: As of 4 pm EDT 21 May 2026

Currencies

EUR -0.05% to $1.1618

GBP -0.06% to $1.3427

Bitcoin -0.09% to $77,610.76

Ethereum -0.06% to $2,133.72

The dollar index edged higher on Thursday after reaching a six-week high earlier in the session, as doubts persisted that a diplomatic breakthrough was imminent.

The dollar index rose +0.07% on the day to 99.20, while the euro declined -0.05% to $1.1618.

Sterling fell -0.34% to $1.3473.

The Japanese yen weakened -0.05% against the dollar to ¥158.95 per dollar.

BoJ board member Junko Koeda said the central bank should raise interest rates at an ‘appropriate pace,’ as price pressures stemming from the Middle East conflict could push underlying inflation above its 2% target, reinforcing the case for a rate increase as early as June.

Separately, the BoJ’s survey of investors indicated that some participants had called for a pause in its bond tapering plan, as sharp market volatility overshadowed a review of its quantitative tightening strategy scheduled for next month.

Fixed Income

US 10-year Bond -1.9 basis points to 4.573%

German 10-year Bund +0.4 basis points to 3.100%

UK 10-year gilt -2.7 basis points to 4.966%

US Treasury yields declined on Thursday following reports that Washington and Tehran were nearing a final draft of a peace agreement.

The yield on the 10-year Treasury note fell -1.9 bps on the day to 4.573%. On Tuesday, it had climbed to 4.687%, its highest level since January 2025.

The yield on the 30-year Treasury bond declined -3.5 bps to 5.093%. It briefly reached 5.197% on Tuesday, its highest level since July 2007, before the global financial crisis.

The two-year Treasury note yield, which typically tracks expectations for Federal Reserve interest rates, rose +2.4 bps to 4.092%. The US Treasury yield curve, measured by the spread between the two-year and 10-year Treasury yields, stood at 48.1 bps.

The Treasury Department sold $19 billion of 10-year Treasury Inflation-Protected Securities (TIPS) on Thursday. The auction recorded a bid-to-cover ratio of 2.53x, above the previous auction’s 2.38x.

Indirect bidders, including governments, fund managers and insurance companies, accounted for roughly 61.0% of the sale, while direct bidders represented 27.5%. The yield on the 10-year TIPS rose +1.1 bps to 2.144%.

According to CME Group's FedWatch Tool, Fed funds futures traders are pricing 20.5 bps of rate hikes in 2026, higher than the 11.2 bps priced in a week ago. Fed funds futures traders are now pricing in a 3.2% probability of a 25 bps rate hike at June’s FOMC meeting, compared to a 2.1% probability of a rate cut last week.

Eurozone government bond prices declined on Thursday.

Germany’s two-year Schatz yield, sensitive to shifts in rate and inflation expectations, rose +3.4 bps to 2.693%. At the longer end of the curve, the 30-year yield fell -0.8 bps to 3.621%.

Government bonds have sold off sharply this week as investors priced in the likelihood that energy prices would remain elevated for longer, thereby fuelling inflation and increasing average borrowing costs.

One-year eurozone inflation swaps traded at 3.67%, above the European Central Bank’s 2% target and not far below the late-April peak of 3.98%.

The yield on the 10-year German Bund rose +3.1 bps to 3.100%, while the yield on the 10-year Italian BTP increased +1.6 bps to 3.850%. The spread between the two stood at 75.0 bps, up 1.2 bps from Wednesday’s 73.8 bps.

Note: As of 4 pm EDT 21 May 2026

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

Tento článek je poskytován pouze pro informační účely a neměl by být považován za nabídku nebo výzvu k nákupu nebo prodeji jakýchkoli investic nebo souvisejících služeb, jejichž odkazy se v něm můžou vyskytovat. Obchodování s finančními nástroji je spojeno se značným rizikem ztráty a nemusí být vhodné pro všechny investory. Dřívější produktivita není spolehlivým ukazatelem budoucí produktivity.

Přihlásit se k odběru přehledů trhu

Přihlásit se k odběru

přehledů

trhu

Předplaťte si nyní

Založeno profesionály. Pro profesionály.