Is the service sector feeling the heat?

What to look out for today

Companies reporting on Wednesday, 6 May: Albemarle, Apollo Global Management, CF INdustries, CVS Health, DoorDash, Fastenal, Marriott International, NRG Energy, Kraft Heinz, Walt Disney, Uber Technologies, Warner Bros Discovery

Key data to move markets today

EU: French, German, Italian and Eurozone HCOB Services and Composite PMIs, Eurozone PPI and speeches by ECB Chief Economist Philip Lane and Executive Board Member Piero Cipollone

USA: ADP Employment Change and speeches by Chicago Fed President Austan Golsbee and St Louis Fed President Alberto Musalem

JAPAN: BoJ Monetary Policy Meeting Minutes and Labour Cash Earnings

Global Macro Updates

April ISM Services meet expectations; new orders down, prices unchanged. The April ISM Services Index registered at 53.6, slightly below the consensus estimate of 53.7 and down from March’s reading of 54.0. The new orders index declined m/o/m to 53.5 from 60.6, yet remained in expansion territory. Meanwhile, the supplier deliveries index increased to 56.8 from 56.2.

The employment index improved to 48.0 from 45.2, though it continued to indicate contraction for the second consecutive month. The prices index was unchanged at 70.7, maintaining its highest level since October 2022.

Respondent feedback reflected a slightly negative outlook. While resilience was observed in the services, healthcare and infrastructure sectors, these gains were offset by weak housing demand, postponed capital expenditures and persistent cost pressures. Additionally, geopolitical factors contributed to heightened caution and extended recovery timelines.

Additionally, the final April S&P Services PMI was reported at 51.0, falling short of the consensus forecast of 52.1, but up from March’s figure of 49.8. The report highlighted the first decrease in demand since April 2024, driven by Middle East tensions and inflationary pressures. Nevertheless, activity, employment and business confidence all showed modest gains, while input costs and selling prices continued to rise significantly.

Elsewhere, new home sales for March totalled 682,000, exceeding the consensus estimate of 655,000 and February’s figure of 635,000. Single-family home sales reached 635,000, representing an 8.9% increase from January. The median new home price in March declined to $387,400, marking a 5.3% decrease m/o/m.

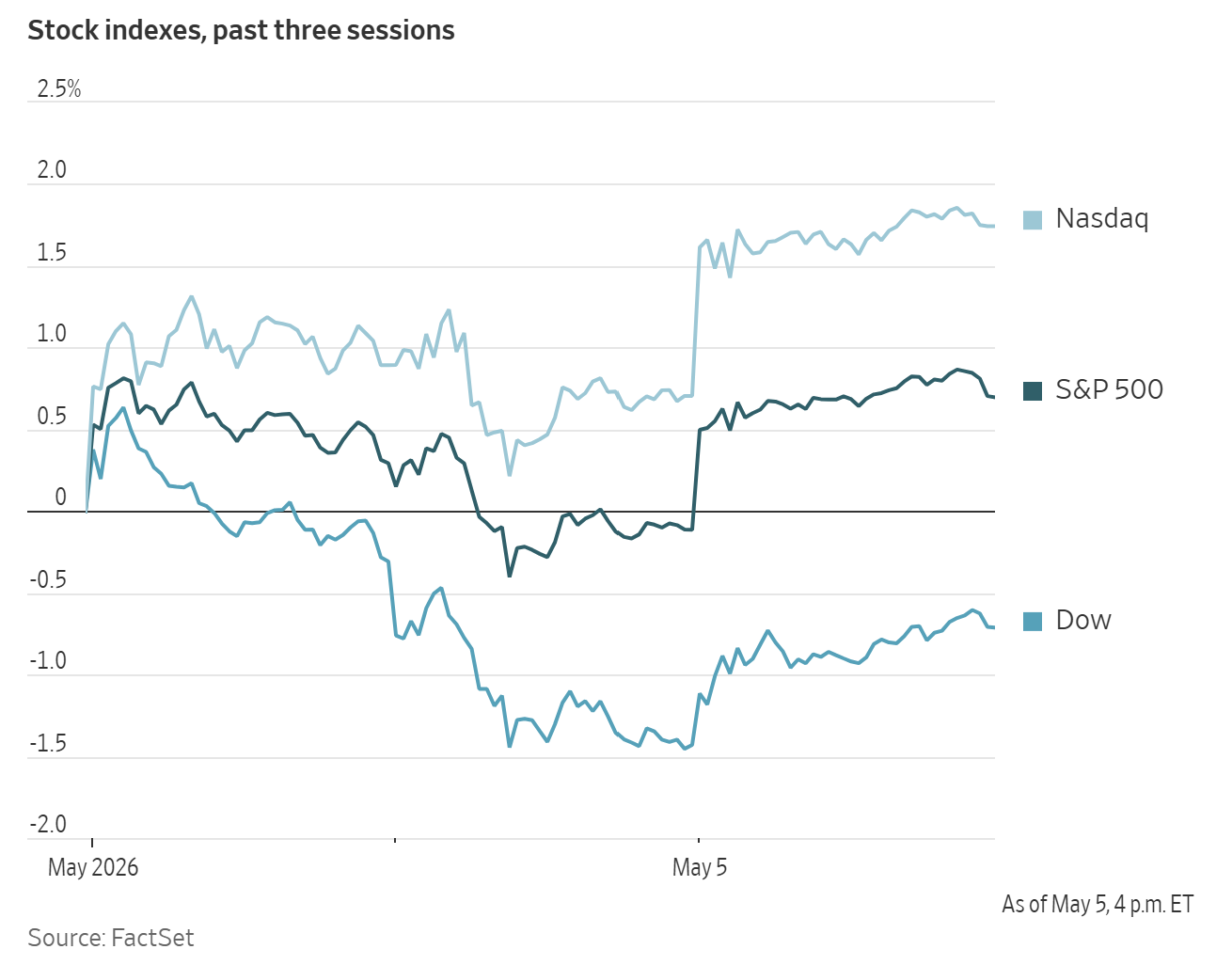

US Stock Indices

Dow Jones Industrial Average +0.73%

Nasdaq 100 +1.31%

S&P 500 +0.81%, with all sectors of the S&P 500 up

On Tuesday, investor enthusiasm for the memory-chip market propelled both the Nasdaq Composite and S&P 500 to record highs, reinforcing the strongest performance for the PHLX Semiconductor Index since the dot-com era.

The semiconductor index has surged +53.70% since the end of March, marking its best 25-day performance since March 2000. Semiconductor manufacturers are striving to meet rapidly increasing demand for specialised devices essential to powering advancements in AI.

Shares of Sandisk, Micron, and Qualcomm each advanced by more than ten percent, contributing to a +1.03% rise in the Nasdaq Composite, which is heavily weighted toward technology stocks.

The S&P 500 was +0.81%, with all eleven sectors of the S&P 500 closing higher, led by Materials and Information Technology. The Dow Jones Industrial Average rose +0.73%, or 356.35 points. Additionally, the Russell 2000 index of small-cap stocks climbed +1.75% to a record level of 2,845.00.

In corporate news, Intel and Samsung shares rose following a Bloomberg news report indicating that Apple is considering partnering with both companies to manufacture the primary chips for its devices in the US.

Separately, Coinbase announced plans to reduce its workforce by approximately 14%, citing the necessity of managing expenses amid market volatility and the rapid evolution of artificial intelligence technologies.

S&P 500 Best performing sector

Materials +1.67%, with DuPont +8.43%, Smurfit Westrock +4.06% and Freeport-McMoRan +3.80%

S&P 500 Worst performing sector

Financials +0.01%, with Fiserv -8.80%, PayPal Holdings -7.74% and Global Payments -3.25%

Mega Caps

Alphabet +1.22%, Amazon +0.54%, Apple +2.64%, Meta Platforms -0.90%, Microsoft -0.54%, Nvidia -1.03% and Tesla -0.81%

Information Technology

Best performer: Intel +12.92%

Worst performer: Palantir Technologies -6.93%

Materials and Mining

Best performer: DuPont +8.43%

Worst performer: Ball -6.27%

Corporate Earnings Reports

Posted on Tuesday, 5 May from The Pulse, our real-time AI-driven news tool. Available exclusively on the EXANTE Web Platform

AMD reported Q1 FY26 revenue of $10.3 bn, beating consensus of $9.85 bn - $9.89 bn, with adjusted EPS of $1.37 vs $1.28-$1.29 expected. Data Centre revenue hit $5.8 bn, up 57% y/o/y and exceeding estimates of $5.6 bn. Q2 guidance set at $10.90 bn - $11.50 bn vs $10.52 bn consensus, with adjusted gross margin ~56% and operating margin 14% up 4pp y/o/y. Management raised server CPU TAM outlook to >35% annual growth reaching $120 bn by 2030, driven by EPYC CPUs, Instinct GPUs, and AI inference demand. CEO Lisa Su commented, "We delivered an outstanding first quarter, driven by accelerating demand for AI infrastructure, with Data Centre now the primary driver of our revenue and earnings growth."

Occidental Petroleum reported Q1 2026 earnings with adjusted EPS of $1.06 beating estimates of $0.64, revenue of $5.1 bn missing $5.6 bn consensus, and adjusted net income of $1.07 bn exceeding $600.3 mn expectations. Average global production reached 1,426 MBOED. The company reaffirmed FY CAPEX guidance at $5.5-5.9 bn and adjusted FY production outlook to 1,410-1,460 MBOED from prior 1,420-1,480 MBOED. Occidental Petroleum named a new CEO.

PayPal reported Q1 revenue $8.35 bn vs est $8.05 bn, adj. EPS $1.34 vs est $1.27, TPV $464 bn vs est $447 bn, transaction margin 45.6% in line with est, ending accounts 439 mn vs est 440 mn. Q2 EPS guidance $1.27 below est $1.33. On 29 April new CEO Enrique Lores announced separating Venmo into a standalone business unit by reorganising reporting lines.

Pfizer reported Q1 2026 adjusted EPS of $0.75, beating Wall Street consensus of $0.72, and revenue of $14.45 bn vs $13.8-$13.84 bn estimates. The company reaffirmed its full-year 2026 guidance for adjusted EPS of $2.80-$3.00 and revenue of $59.5 - $62.5 bn, with newer products showing growth. Bristol-Myers Squibb announced its alliance with Pfizer is partnering with Mark Cuban Cost Plus Drug Company to offer Eliquis.

Super Micro Computer reported Q3 adjusted EPS of $0.84, beating estimates of $0.63, while revenue came in at $10.24 bn, missing $12.45 bn consensus. Adjusted gross margin was 10.1%, exceeding 6.75% expected. Q4 guidance calls for adjusted EPS of $0.65 to $0.79 versus $0.57 est and net sales of $11.0 bn to $12.5 bn vs $11.16B est. FY net sales guided at $38.9 bn to $40.4 bn, previously at least $40 bn. CEO stated Supermicro's transformation into a total datacenter infrastructure provider is accelerating with margin recovery and rapid DCBBS business growth.

DigitalOcean reported Q1 2026 earnings with revenue of $258 mn beating $250 mn consensus, EPS $0.44 vs $0.26 est. EBITDA $105 mn vs $91 mn est, and ARR $1.03 bn vs $994 mn est. AI Customer ARR reached $170M, up 221% YoY. FY2026 guidance raised to revenue $1.14B vs $1.09B est and EPS $1.10 vs $0.97 est. FY2027 revenue growth guided to 50% vs 31% est. Company expanded credit facility to $413M.

MicroStrategy reported Q1 2026 earnings with EPS of -$38.2 missing consensus of -$18. Revenue of $124.3 mn vs estimates of $120-125 mn, a $12.5 bn loss, Bitcoin holdings unchanged at 818,334 BTC,valued at $64 bn, and cash equivalents of $2.21 bn below $3.42 bn expected. During the call, Michael Saylor indicated the company may sell some Bitcoin holdings to fund dividend payments. Michael Saylor stated: “We will probably sell some bitcoin to pay a dividend just to inoculate the market and send the message that we did it.”

Lumentum Holdings reported Q3 revenue of $808 mn vs estimates of $810 mn. EPS of $2.37 versus $2.27, operating profit of $261 mn vs $246 mn and gross margin of 48% versus 45%. Q4 guidance includes revenue of $985 mn vs $916 mn estimates. EPS of $2.95 vs $2.75 and operating margin of 36% vs 32%.

Astera Labs reported Q1 revenue of $308 mn vs consensus $292 mn. EPS $0.61 versus $0.55, operating income $112 mn versus $101mn estimated and gross margin 76% vs 70% estimated. Q2 guidance includes revenue $360 mn vs $310 mn estimated, EPS $0.69 versus $0.55, operating income $133 mn versus $104 mn and gross margin 73% vs 72% estimated.

European Stock Indices

CAC 40 +1.08%

DAX +1.71%

FTSE 100 -1.40%

Commodities

Gold spot +0.84% to $4,556.04 an ounce

Silver spot -0.53% to $72.33 an ounce

West Texas Intermediate -2.35% to $102.67 a barrel

Brent crude -2.93% to $110.50 a barrel

Gold prices rebounded on Tuesday primarily driven by bargain hunting following Monday’s sharp sell-off amid ongoing geopolitical tensions in the Middle East.

Spot gold advanced +0.84% to $4,556.04 per ounce, following its lowest point since March 31 on Monday.

In contrast, spot silver declined -0.53% to $72.33 per ounce.

Global oil prices retreated on Tuesday, a day after the US initiated operations to reopen the Strait of Hormuz for shipping. However, ongoing exchanges between the US and Iran tempered the extent of the price decline.

Brent crude futures eased by $3.34, or -2.93%, to $110.50 per barrel. US WTI crude fell $2.47, or -2.35%, to $102.67.

Iran continued its attacks against the United Arab Emirates overnight and into Tuesday. US Defence Secretary Hegseth stated that a secure route remains available through the Strait and affirmed that the ceasefire with Iran is still in effect. When questioned about potential actions by Iran that could break the ceasefire, the US President responded, ‘we'll see.’

The US President also noted that Iran's public statements regarding a possible deal differ significantly from their private communications. The Saudi Ministry of Foreign Affairs issued a statement expressing concern over the ongoing military escalation in the region and emphasised the necessity of restoring free navigation through the Strait. Meanwhile, members of the UN Security Council have commenced discussions on a US and Bahrain-backed draft resolution, which could result in sanctions against Iran and potentially authorise the use of force.

According to S&P Global, global crude inventories for April decreased by approximately 200 million barrels, or 6.6 million barrels per day (bpd). The firm estimated that demand destruction due to elevated prices amounted to 5.0 million bpd in April, marking the steepest decline since the onset of COVID-19.

Chevron's CEO stated late Monday that physical shortages in oil supply are expected to emerge worldwide due to the disruption at the Strait. Diamondback Energy indicated that there is a genuine supply-demand imbalance and that the resulting price signals are prompting the company to consider increasing production.

Additionally, Ukrainian drones struck the Kirishi refinery near Russia’s Baltic coast, igniting a fire at the facility.

Note: As of 4 pm EDT 5 May 2026

Currencies

EUR +0.03% to $1.1690

GBP +0.05% to $1.3534

Bitcoin +1.44% to $81,409.54

Ethereum +0.62% to $2,375.36

On Tuesday, the US dollar experienced a modest uptick as investors assessed recent developments surrounding the conflict with Iran. The yen weakened amid subdued trading activity, following last week's suspected intervention by Tokyo that temporarily strengthened the currency.

The dollar index rose +0.02% to 98.49, building on a +0.27% gain from Monday. The euro appreciated by +0.03% to $1.1690, while the British pound advanced +0.05% to $1.3534.

The dollar ended the trading session +0.44% to ¥157.84, after reaching a session low of ¥155.69 earlier in the day.

Data from Friday indicated that Tokyo spent approximately $35 billion to support the yen last week. However, analysts remain skeptical about the effectiveness of such measures in providing sustained relief for the currency.

A sharp rally in the yen on Monday fuelled speculation of renewed intervention from Japanese authorities, particularly as officials had cautioned last week about possible actions during the Golden Week holidays.

Fixed Income

US 10-year Bond -1.3 basis points to 4.429%

German 10-year Bund -2.8 basis points to 3.064%

UK 10-year Gilt +9.3 basis points to 5.064%

On Tuesday, US Treasury yields declined across the curve due to a moderation in oil prices.

The yield on the US 10-year Treasury note decreased -1.3 bps to 4.429%, following Monday’s peak at 4.464%, its highest level since 27 March. The yield on the 30-year Treasury bond dropped -2.8 bps to 4.989%, after reaching 5.036% on Monday, which marked a high not seen since 17 July. The two-year US Treasury yield, often indicative of Fed Fund rate expectations, declined -1.2 bps to 3.950% after reaching 3.993% on Monday, its highest since 27 March.

This week, markets are set to receive several reports assessing the labour market’s health, culminating in the government’s jobs report on Friday. Consensus among economists forecasts a 62,000 increase in nonfarm payrolls.

The US yield curve, measured as the spread between the yields on two- and 10-year Treasury notes, stood at 47.9 bps.

According to CME Group's FedWatch Tool, Fed funds futures traders are pricing in 7.0 bps of rate hikes in 2026, compared to 5.4 bps of rate cuts priced in a week ago. Fed funds futures traders are now pricing in a 4.0% probability of a 25 bps rate cut at the June FOMC meeting, up from 2.6% a week ago.

Eurozone government bond yields also edged lower on Tuesday.

Germany’s 10-year bond yield declined -2.8 bps to 3.064%, following a +5.1 bps increase in the previous session. The rate-sensitive two-year German yield decreased -4.1 bps to 2.691%, just below last week’s one-month high of 2.760%. On the long end, the 30-year German yield was marginally lower, falling -0.6 bps to 3.579%.

Last week, the ECB opted to keep rates unchanged. However, policymakers debated the possibility of a rate hike and signalled that further tightening could be warranted in June.

Italy’s 10-year yield was down -6.2 bps at 3.871%. The spread against the German 10-year was at 80.7 bps, narrowing by 3.4 bps on the day.

Note: As of 4 pm EDT 5 May 2026

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

Tento článek je poskytován pouze pro informační účely a neměl by být považován za nabídku nebo výzvu k nákupu nebo prodeji jakýchkoli investic nebo souvisejících služeb, jejichž odkazy se v něm můžou vyskytovat. Obchodování s finančními nástroji je spojeno se značným rizikem ztráty a nemusí být vhodné pro všechny investory. Dřívější produktivita není spolehlivým ukazatelem budoucí produktivity.

Přihlásit se k odběru přehledů trhu

Přihlásit se k odběru

přehledů

trhu

Předplaťte si nyní

Založeno profesionály. Pro profesionály.