Are markets operating with blinders on?

Corporate Earnings Calendar

Global market indices

Currencies

Fixed Income

Commodity sector news

Key data to move markets

Corporate Earning Calendar

20 February - 26 February 2025

Thursday: Alibaba Group Holding, Walmart, Block, Booking Holdings, Newmont, Rivian Automotive, Unity Software, Southern Co., Consolidated Edison, Naturgy Energy

Monday: Berkshire Hathaway, Riot Platforms, Zoom Video Communications, Domino’s Pizza, Diamondback Energy

Tuesday: AMC Entertainment, Home Depot, Keurig Dr Pepper, Intuit, Lemonade, Lucid Group

Wednesday: NVIDIA, Marathon Digital, Salesforce, Snowflake, Synopsys, Teladoc

Global market indices

US Stock Indices Price Performance

Nasdaq 100 +2.96% MTD and +5.25% YTD

Dow Jones Industrial Average +0.03% MTD and +4.73% YTD

NYSE +1.15% MTD and +5.92% YTD

S&P 500 +1.72% MTD and +4.46% YTD

The S&P 500 is +1.52% over the past week, with all of the 11 sectors up MTD. The Equally Weighted version of the S&P 500 is +1.68% this week. Its performance is +0.78% MTD and +4.21% YTD.

The S&P 500 Information Technology sector is the leading sector so far this month, up +5.36% MTD and +2.27% YTD, while Consumer Discretionary is the weakest at -3.78% MTD and +0.45% YTD.

This week, Energy outperformed within the S&P 500 at +3.00%, followed by Information Technology and Financials at +2.85% and +1.68%, respectively. Conversely, Communication Services underperformed at +0.22%, followed by Health Care and Industrials, at +0.27% and +0.66%, respectively.

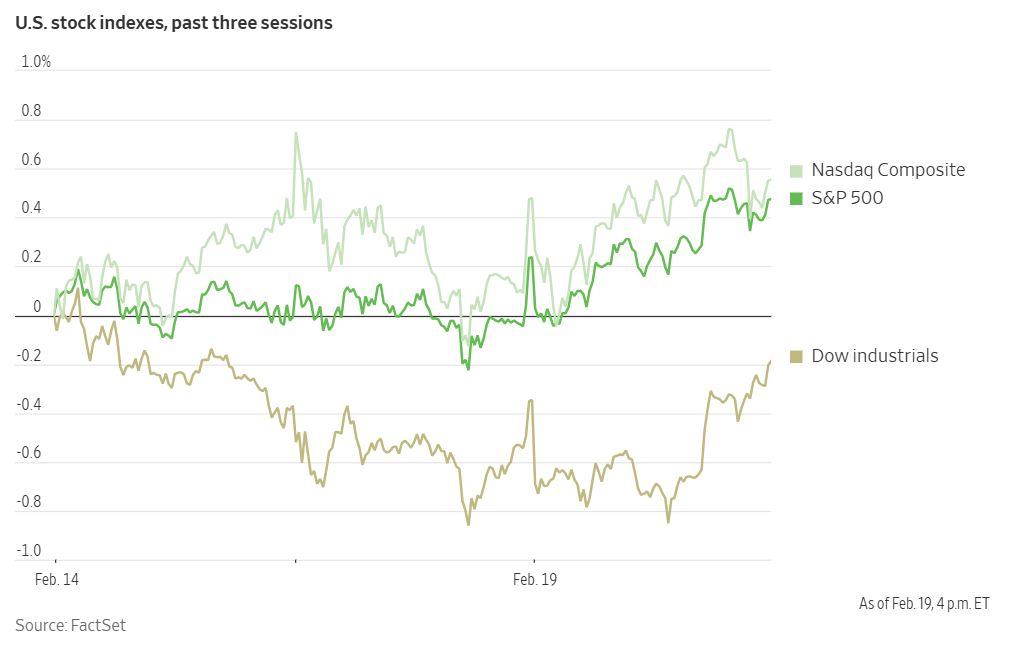

US stocks advanced marginally on Wednesday, reversing earlier losses as investors considered FOMC meeting minutes, new housing data, and recent tariff announcements from the US President.

Equities experienced renewed upward momentum towards the close of trading. The S&P 500 Index finished +0.2%, establishing a new record close—its third in 2025. The Dow Jones Industrial Average rose +0.2%, and the Nasdaq Composite was +0.07%.

In company news, Apple introduced a new entry-level smartphone, the iPhone 16e, priced at $599, intended to stimulate growth after a subdued holiday period.

Nikola filed for bankruptcy, concluding a protracted downturn for the once-prominent electric-vehicle firm that encountered diminished sales and leadership transitions following a fraud scandal.

Carvana anticipates continued retail vehicle sales and earnings growth this year after a record Q4 that exceeded Wall Street forecasts.

Elliott Investment Management is pursuing board seats at oil refiner Phillips 66, the latest action in a sustained campaign urging the company to divest assets, enhance operational performance, and strengthen board oversight.

Mega caps: The Magnificent Seven had a mostly positive performance this week with Tesla +7.15%, Nvidia +6.17%, Apple +3.38%, Microsoft +1.40%, and Alphabet +0.90%, while Meta Platforms -2.98%, and Amazon -1.00%.

Energy stocks demonstrated a mostly positive performance this week, with the Energy sector itself +3.00% due to supply concerns following drone attacks on Russian production platforms and despite a buildup of US crude stockpiles. WTI and Brent prices are this week, +1.36% and +1.52%, respectively. Over the week Occidental Petroleum +6.61%, Apa +5.45%, Marathon Petroleum +4.98%, Phillips 66 +3.93%, Hess +3.09%, Halliburton +2.96%, ExxonMobil +2.75%, Chevron +1.50%, ConocoPhillips +1.19%, and Baker Hughes +1.03%, while BP -1.16%, Shell -0.57%, and Energy Fuels -3.35%.

Materials and Mining stocks had a mostly positive performance this week, with the Materials sector +1.43%. Albemarle +9.23%, Nucor +4.66%, Mosaic +3.79%, CF Industries +3.24%, Freeport-McMoRan +1.61%, Yara International +1.61%, and Newmont Corporation +1.28%, while Sibanye Stillwater -7.99%.

European Stock Indices Price Performance

Stoxx 600 +2.33% MTD and +8.76% YTD

DAX +3.23% MTD and +12.68% YTD

CAC 40 +2.02% MTD and +9.89% YTD

IBEX 35 +4.53% MTD and +11.51% YTD

FTSE MIB +5.14% MTD and +12.17% YTD

FTSE 100 +0.44% MTD and +6.60% YTD

This week, the pan-European Stoxx Europe 600 index was +0.79%. It was -0.91% on Wednesday, closing at 552.10.

So far this month in the STOXX Europe 600, Banks is the leading sector, +7.40% MTD and +17.61% YTD, while Travel & Leisure is the weakest at -2.66% MTD and -0.04% YTD.

This week, Autos & Parts outperformed within the STOXX Europe 600 with a +4.53% gain, followed by Industrial Goods & Services and Food & Beverage at +3.84% and +2.21%, respectively. Conversely, Personal & Household Goods underperformed at -2.00%, followed by Retail and Travel & Leisure, at -1.73% and -1.71%, respectively.

Germany's DAX index was -1.80% on Wednesday, closing at 22,433.63. It was +1.29% for the week. France's CAC 40 index was -1.17% on Wednesday, closing at 8,110.54. It was +0.85% for the week.

The UK's FTSE 100 index was -1.08% this week to 8,712.53. It was -0.62% on Wednesday.

On Wednesday, the Stoxx Europe 600 performance experienced a pronounced decline in cyclical sectors, with Construction & Materials, Basic Resources, and Chemicals emerging as the weakest segments.

This trend unfolded amid indications from the US President regarding potential tariffs of approximately 25% on imports of automobiles, semiconductors, and pharmaceuticals, with a formal announcement anticipated as soon as 2nd April. Within the Basic Resources sector, Glencore disclosed a reduction in FY profitability, primarily attributed to the challenging environment of depressed prices for several of its core commodities. The company also signalled a commitment to shareholder returns with the reintroduction of a share repurchase programme, projected to return $2.2 billion in capital.

The Aerospace & Defence sector provided support to the Industrial Goods & Services sector, underpinned by robust earnings reports. British Airways announced a FY underlying EPS of 68.5 pence, exceeding the consensus forecast of 66.8 pence and accompanied by a record order backlog. Additionally, MTU Aero Engines revised its financial outlook upward for 2025, based on a more conservative exchange rate assumption for the euro against the US dollar. The strength within this sector is also further reinforced by ongoing dialogue surrounding a potential resolution to the conflict in Ukraine, with a prospective strategic repositioning of the US from the region, potentially stimulating increased defence spending amongst European nations.

The Energy sector outperformed, benefiting from higher crude oil prices and media reports suggesting BP is evaluating the divestiture of its lubricants unit, valued at approximately $10 billion, as part of a strategic portfolio assessment. The Utilities sector was also higher, driven by its perceived characteristic as bond proxies. In corporate news, Engie attracted attention with its announced intention to divest its assets in Kuwait and Bahrain, including equity stakes in gas and desalination infrastructure, to ACWA Power.

Other Global Stock Indices Price Performance

MSCI World Index +1.83% MTD and +5.37% YTD

Hang Seng +11.16% MTD and +12.06% YTD

This week, the Hang Seng Index was +2.82%, while the MSCI World Index was +1.52%.

Currencies

EUR +0.65% MTD and +0.73% YTD to $1.0425.

GBP +1.56% MTD and +0.61% YTD to $1.2579

The euro was +0.39% against the USD over the past week, while the British pound was +1.08% against the dollar. The Dollar Index is -0.80% so far this week, -1.24% MTD and -1.35% YTD.

Safe-haven currencies, predominantly the US dollar and the yen, were up on Wednesday due to the ongoing ceasefire discussions in the Russia-Ukraine conflict and indications that US levies on automobiles could be implemented as early as 2nd April, the day after cabinet members are scheduled to present reports outlining options for a range of import duties.

Overall on Wednesday the US dollar strengthened against currencies typically favoured by investors when risk appetite is elevated. This included the euro, sterling, the Australian and Canadian dollars, and currencies within emerging markets, such as the Mexican peso.

The euro ended -0.25% against the dollar on Wednesday, trading at $1.0425. The euro has proven particularly sensitive to developments concerning Russia and Ukraine, exhibiting gains last week amid optimism regarding conflict resolution, and subsequent declines in response to indicators of renewed tension.

The dollar index was 107.12, marking a +0.12% increase after a -1.2% decrease the previous week.

Sterling ended Wednesday -0.43% to $1.2579. The UK Office for National Statistics reported on Wednesday that January CPI came in at 3.0%, above forecasts of a 2.8% rise. Services inflation, an indicator previously highlighted by the BoE as a potential impediment, was 5.0%, up from December’s 4.4%, but below an expected 5.2% increase.

Against the euro, the pound remained stable at 82.86 pence, maintaining levels observed prior to the inflation report's release.

In afternoon trading, the dollar was -0.43%, reaching ¥151.38 following the release of minutes from the January FOMC meeting. These minutes revealed that initial policy proposals from the White House had generated concerns regarding elevated inflation, and reaffirmed a continued stance of pausing interest rate reductions. In addition, data indicating a -8.4% drop in US single-family homebuilding during January, to a seasonally adjusted annual rate of 993,000 units, hurt the dollar. This contraction was attributed to disruptions caused by snowstorms and freezing temperatures.

Note: As of 5:00 pm EST 19 February 2025

Fixed Income

US 10-year yield +1.9 bps MTD and -3.8 bps YTD to 4.538%.

German 10-year yield +3.7 bps MTD and +19.1 bps YTD to 2.560%.

UK 10-year yield +3.0 bps MTD and +4.4 bps YTD to 4.613%.

US Treasury 10-year bond yields are +9.1 bps over the past week.

Treasury yields declined on Wednesday following the release of minutes from the last FOMC meeting. The minutes indicated that policymakers had engaged in discussions regarding the potential advisability of decelerating or temporarily halting the reduction of the Fed's balance sheet holdings.

Since June 2022, as part of its quantitative tightening programme, the Fed has been allowing bonds to mature and roll off its balance sheet without reinvestment. Slowing or pausing this programme is expected to be beneficial for Treasury securities. Increased reinvestment by the Fed in US government bonds could potentially decrease the volume of debt that the Treasury Department is required to issue.

Federal Reserve officials highlighted the challenge of obtaining a clear assessment of market liquidity due to the government reaching its statutory limit for outstanding debt in January. The Treasury Department has been using so-called extraordinary measures to pay the federal government’s expenses and to prevent a default on its obligations.

Furthermore, initial policy proposals emanating from the White House also generated concerns within the Fed regarding the potential for increased inflation. Policymakers noted during the 28th - 29th January meeting that businesses had indicated a general expectation to increase prices in order to offset the expenses associated with import tariffs.

The yield on the US 10-year Treasury note was -1.8 bps during the trading day, reaching 4.538%. On the short end of the curve, the yield on the 2-year Treasury note was -2.3 bps, settling at 4.274%.

Fed Funds futures indicate that traders are currently pricing in 37 bps of monetary policy easing by the end of the year. This pricing suggests an approximate 50% probability of a second 25 bps reduction in the federal funds rate.

On Wednesday, prior to the public release of the FOMC meeting minutes, the Treasury Department encountered subdued demand for a $16 billion offering of 20-year bonds. These bonds were sold at a high yield of 4.830%, approximately 1 bps higher than their trading level preceding the auction. The resulting bid-to-cover ratio was 2.43x, the lowest level since November. Furthermore, the Treasury Department is scheduled to offer $9 billion in 30-year Treasury Inflation-Protected Securities (TIPS) today.

The German 10-year yield was +7.9 bps over the past week, while the UK 10-year yield was +3.0 bps over the past 7 days. The spread between US 10-year Treasuries and German Bunds is 197.8 bps, 17.0 bps narrower than last week.

Italian bond yields, a benchmark for the eurozone periphery, were +7.6 bps this week to 3.638%. Consequently, the spread between Italian and German 10-year yields is 107.8 bps, 0.3 narrower than last week.

Germany's 10-year bond yield was +6.0 bps on Wednesday, reaching 2.560%, the highest level since 29th January. Germany's two-year bond yield, which is particularly sensitive to anticipated ECB rate expectations, was +4.0 bps at 2.170%. German benchmark yields have collectively risen by approximately +7.9 bps this week. These rises were due to potential increases in sovereign borrowing in relation to increased defence spending by EU governments. Further contributing to this sentiment, the President of the European Commission (EC), Ursula von der Leyen, stated on Friday that the EC would propose exempting defence expenditure from established EU limitations on government spending. There were also suggestions by ECB Governing Council member Isabel Schnabel in an interview with the Financial Times of a possible pause in interest rate reductions.

Money market participants have reduced their expectations for further ECB rate reductions by approximately 4 bps, and are now forecasting around 72 bps of cumulative rate cuts by the end of December.

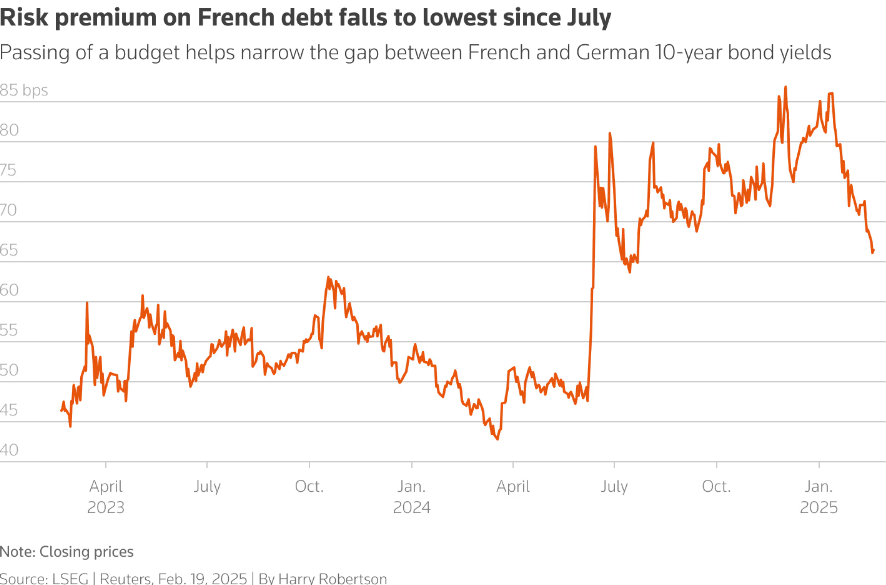

Italy's 10-year bond yield was +9.1 bps at 3.638%, its most significant single-day increase since mid-December. The spread between French and German 10-year bond yields widened by 1.2 bps, reaching 67.5 bps, after having touched 65.80 bps on Tuesday, its narrowest point since July. The recent parliamentary passage of a budget earlier this month has diminished investor apprehension due to France's public deficit outlook.

Decreases in Italian and French bond spreads have been observed as investors speculate on increased issuance of joint EU debt to finance military expenditure.

Commodities

Gold spot +3.80% MTD and +11.04% YTD to $2,932.45 per ounce.

Silver spot +2.96% MTD and +13.60% YTD to $32.71 per ounce.

West Texas Intermediate crude -1.35% MTD and -0.80% YTD to $72.18 a barrel.

Brent crude +0.20% MTD and +1.58% YTD to $76.13 a barrel.

Gold prices are +0.99% this week. Gold prices fell on Wednesday, receding from a record peak attained earlier in the trading session. This decline was primarily attributed to US dollar strengthening and persistent investor unease regarding recent tariff pronouncements.

Spot gold prices were -0.08%, reaching $2,932.45 per ounce. Earlier in the session, it reached an unprecedented high of $2,946.85 per ounce. In the US futures market, gold contracts settled -0.40% to $2,936.10.

This week, WTI and Brent are +1.36% and +1.52%, respectively. Oil prices remained elevated near a one-week high on Wednesday, influenced by concerns regarding potential supply disruptions in both Russia and the US. Market participants also awaited further clarity regarding sanctions as Washington endeavors to negotiate an accord to resolve the conflict in Ukraine.

Brent crude futures were up 36 cents, or +0.48%, to settle at $76.13 per barrel. WTI rose by 43 cents, or +0.60%, to settle at $72.18 per barrel. These levels represented the highest closing values for both crude benchmarks since 11th February.

Market participants are trying to determine the comprehensive impact of both announced and implemented sanctions on Russia. Furthermore, drone attacks targeting Russian oil infrastructure are contributing to a reduction in supply availability. Russian authorities indicated that Caspian Pipeline Consortium (CPC) oil flows, a significant route for crude exports from Kazakhstan, were reduced by between 30% and 40% on Tuesday following a Ukrainian drone attack on a pumping station. A reduction of 30% would represent an estimated loss of 380,000 barrels per day from overall market supply.

In the US, inclement weather conditions posed a threat to oil supply, with the North Dakota Pipeline Authority estimating that production within the state could decline by as much as 150,000 barrels per day.

Furthermore, speculation has arisen that OPEC+ may consider delaying their planned supply increase scheduled for April.

Tariffs announced by the White House could also exert downward pressure on oil prices by increasing the cost of consumer goods, potentially weakening the global economy and consequently reducing fuel demand. Concerns regarding demand from Europe and China are also contributing to moderating price increases.

Separately, market participants are awaiting the release of US oil inventory data from the US Energy Information Administration (EIA) later today. These reports are scheduled to be released one day later than usual on account of the Presidents' Day holiday on Monday.

Note: As of 5:15 pm EST 19 February 2025

Key data to move markets

EUROPE

Thursday: German PPI, Eurozone Consumer Confidence and a speech by Bundesbank President Joachim Nagel.

Friday: Eurozone HCOB Composite, Manufacturing, and Services PMIs, German HCOB Composite, Manufacturing and Services PMIs, French HCOB Composite, Manufacturing and Services PMIs, Italian CPI, and a speech by ECB Chief Economist Philip Lane.

Sunday: German Federal Election.

Monday: German IFO Business Climate, Current Assessment and Expectations Surveys, Eurozone Harmonised Index of Consumer Prices, and Bundesbank Monthly Report.

Tuesday: German GDP.

Wednesday: German Gfk Consumer Confidence.

UK

Friday: Gfk Consumer Confidence, Retail Sales, and S&P Global/CIPS Composite, Services and Manufacturing PMIs.

Monday: A speech by BoE FOMC member Swati Dhingra.

Tuesday: A speech by BoE Chief Economist Huw Pill.

Wednesday: A speech by BoE FOMC member Swati Dhingra.

US

Thursday: Initial and Continuing Jobless Claims, Philadelphia Fed Manufacturing Survey, and speeches by Chicago Fed President Austan Goolsbee, St. Louis Fed President Alberto Musalem, Fed Vice Chair for Supervision Michael Barr, and Fed Governor Adriana Kugler.

Friday: S&P Global Composite, Manufacturing and Services PMIs, Existing Home Sales Change, Michigan Consumer Sentiment Index, UoM 5-year Consumer Inflation Expectations, and speeches by San Francisco Fed President Mary Daly and Fed Vice Chair Philip Jefferson.

Tuesday: Housing Price Index and Consumer Confidence.

Wednesday: New Home Sales Change and a speech by Atlanta Fed President Raphael Bostic.

CHINA

Thursday: PBoC Interest Rate Decision

JAPAN

Thursday: National Consumer Price Index.

Global Macro Updates

The cost of security: Europe's defence expansion. Increased defense spending plans across Europe are contributing to a rise in long-term borrowing costs, as investors anticipate a surge in sovereign debt issuance. The Financial Times reported that nations such as Germany and the UK have experienced yield increases, attributed to expectations of heightened debt supply. The article further noted that the White House's encouragement for Europe to augment its security funding has amplified this trend, resulting in the steepest yield curves observed in two years.

Analysts forecast that persistent deficits and inflationary pressures will continue to exert upward pressure on borrowing costs. Furthermore, the EU's recent decision to relax fiscal regulations pertaining to defence expenditure is compounding concerns regarding debt-to-GDP ratios, prompting considerations of potential joint debt issuance among EU member states. In a separate Financial Times article, it was reported that the EU is contemplating reallocating €93 billion in unutilised pandemic recovery funds to strengthen its defence sector, amidst a possible strategic disengagement by the US in security matters. European Commission President Ursula von der Leyen has highlighted this financing option, indicating that the EU's defence requirements could potentially reach €500 billion over the forthcoming decade.

German election on Sunday, a major influence going forward. Adding to the dynamic and multifaceted nature of the situation, Politico has provided analysis of the German election preceding Sunday's vote. Mr. Merz and Mr. Scholz participated in a final head-to-head debate Wednesday evening. Politico emphasised that while CDU/CSU lead candidate Mr. Merz is currently favored to assume the chancellorship, inherent uncertainties persist. Mr. Merz has articulated that his preferred outcome would involve only one coalition partner; however, this scenario is contingent upon smaller parties underperforming in the election. He has explicitly excluded the far-right AfD as a potential coalition partner, thereby narrowing the viable options to the SPD and the Greens.

According to The Conversation, should three or more smaller parties each fail to secure at least 5% of the vote, their unclaimed parliamentary seats would be redistributed proportionally among parties exceeding the threshold, a process which will significantly shape the composition of the future governing coalition. While all major parties are proposing increased public investment, their respective funding proposals do diverge. Sell-side analysts underscore that the primary risk to the necessary reform initiatives aimed at bolstering the German economy is a potentially fragmented parliament, raising the possibility of diminished effectiveness in policy implementation.

Bund vigilantes could welcome increased German spending. Investors are conveying a distinct message to Germany, in advance of its elections on Sunday: there exists capacity for increased sovereign borrowing.

This is important in a world where governments are facing heightened scrutiny from fixed-income investors, often referred to as "bond vigilantes," regarding excessive government spending and substantial budgetary deficits. Furthermore, advocating for increased borrowing poses a challenge within a nation that has historically prioritised fiscal prudence as a matter of national principle.

However, Germany's decades-long commitment to fiscal discipline has resulted in a comparatively modest debt burden, thereby affording the nation considerable borrowing capacity at a time when its economy is in need of stimulus measures. Contrary to expectations of investor reprisal for increased governmental borrowing, market participants would likely welcome an increase in bond issuance, given the current scarcity of prime-quality European sovereign debt instruments available for institutional fund managers.

From Germany's perspective, this may represent an opportune moment for a newly constituted government to initiate supplementary bond issuance. The nation's sovereign borrowing costs – currently approximately 2.50% for 10-year Bunds – remain the most competitive within Europe, and are projected to potentially decline further, given anticipated additional interest rate reductions by the ECB within the current year.

An expanded supply of German sovereign debt is likely to elicit robust demand from institutional investors, including pension funds, insurance corporations, and banking institutions, all of which maintain a requisite need for high-quality, long-duration assets. Germany, alongside the Netherlands and Luxembourg, are the sole member states possessing a AAA credit rating from all three major credit rating agencies.

Finally, increased German sovereign borrowing and associated governmental expenditure could exert a positive ripple effect throughout the wider EU economic landscape.

Europe redefines its security architecture amidst a potential Ukraine ceasefire. Despite ongoing US-Russia peace discussions, Europe maintains its commitment to supporting Ukraine. European defence stocks have experienced substantial gains, directly correlated with pledges of increased European defence spending. Analysts have observed a discernible shift in investor sentiment towards defence equities, now recognised as essential in the post-Ukraine invasion geopolitical landscape.

Furthermore, analysts emphasise Europe's imperative to significantly augment its defence expenditure in the context of potential strategic decoupling by the US. However, as noted by Reuters, realising these defence enhancements will require navigating considerable challenges related to fiscal sustainability, industrial production capacity, and political coordination. Additionally, the ECB faces the complex task of accommodating these fiscal expansions alongside prevailing macroeconomic conditions.

The President of the European Council, Antonio Costa, has asserted the necessity of the EU's direct involvement in negotiations with Russia regarding the resolution of the Ukraine war, in order to effectively define Europe's future security architecture.

However, Keith Kellogg, the US envoy to the talks, stated on Saturday that European nations would not ‘have a seat at the table’ in these negotiations, although their perspectives could potentially be considered. This statement followed a formal request from the US to European capitals for detailed information regarding the types of weaponry, financial resources, and peacekeeping forces they could contribute to a post-conflict Ukraine.

Officials indicated that this request also presented an opportunity for European nations to advocate for their right to exert influence over the negotiation process. Mark Rutte, NATO’s Secretary-General, emphasised that should Europe aspire to a meaningful role in these discussions, it must articulate with clarity its desired outcomes and the concrete contributions it is prepared to offer.

While every effort has been made to verify the accuracy of this information, LHCM Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

本文提供給您僅供資訊參考之用,不應被視為認購或銷售此處提及任何投資或相關服務的優惠招攬或遊說。金融商品交易涉及重大損失風險,可能不適合所有投資者。過往績效不代表未來表現。

由專業人士建立。為專業人士打造。