Will investors continue to fill up on equities?

- Markets in November

- The economic picture

- Global market indices

- Commodity sector news

- Currencies

- Cryptocurrencies

- Fixed Income

- What to think about in December

- Key events in December

Markets in November

Equities markets have been in positive territory in November as investors focused on the US economy’s strong economic growth and the Fed continuing to signal progress in achieving a ‘soft landing’. The S&P 500 is +5.14% MTD, the Dow is +7.42% MTD, while the Nasdaq 100 is +5.19% MTD. The NYSE is +5.05% MTD.

European equity markets were mostly positive in November, with the STOXX 600 poised to end the month slightly higher. However, there are growing concerns that sluggish economic growth and uncertainty surrounding US President-elect Donald Trump could lead to problems for stocks into 2025.

In the bond market, yields rose in the US and the UK following on from the US election and the UK budget. The Trump presidency with Republican majorities in the Senate and House brought the spectre of tariffs and rising inflation to the fore. Markets reacted positively to Trump’s suggested nominee for Treasury secretary, Scott Bessent, who currently runs macro hedge fund Key Square Group, on the belief that he may have a more gradualist approach to tariffs. It is hoped by many investors that he may be a more moderating force in the cabinet relative to other cabinet nominees including Jamieson Greer, nominated as US trade representative, Kevin Hassett, nominated as director of the National Economic Council, Howard Lutnick for Commerce secretary, Marco Rubio nominated as secretary of State, and Michael Waltz, nominated as national security adviser.

The economic picture

The US economy continues to expand. GDP increased at a 2.8% annualised pace in Q3 driven by consumer spending which advanced 3.5%, the most this year. The labour market is also holding up with jobless claims continuing to come in below consensus forecasts in November. Latest initial jobless claims came in at 213,000 although continuing claims increased to 1.9 million. Market participants will be looking closely at the November non-farm payroll numbers, due to be released on 6 December, for further indications as to the possible trajectory of Fed moves. Inflation also seems to be on track with the October Personal Consumption Expenditure Price Index (PCE Index), the Fed’s favourite inflation gauge, coming in at 0.2% m/o/m and 2.3% y/o/y, both in line with expectations. Core inflation came in at 0.3% on a monthly basis and 2.8% y/o/y, also as forecast. Consumer spending remained sold though slightly down from September’s figures. Expenditures rose 0.4% on the month, as forecast, while personal income surged 0.6%, well above the 0.3% estimate. The Flash Composite PMI in November increased to 55.3 from October’s 54.1, the highest level since April 2022. Higher activity reflected rising demand, with new orders picking up sharply to register the strongest upturn in business inflows since May 2022. The Flash Services PMI jumped to 57.0 from October’s 55.0, a 32-month high. However, the manufacturing sector remains in contractionary territory, with the Flash US Manufacturing PMI coming in at 48.8. Although a 4-month high, it was only slightly up from October’s 48.5. Nevertheless, consumers are feeling more confident. The Conference Board's consumer confidence index increased in November to 111.7, up 2.1 points from 109.6 in October. The Present Situation Index—based on consumers’ assessment of current business and labor market conditions, increased by 4.8 points to 140.9. The Expectations Index, based on consumers’ short-term outlook for income, business, and labour market conditions— ticked up 0.4 points to 92.3, well above the threshold of 80 that usually signals a recession ahead. According to Dana M. Peterson, Chief Economist at The Conference Board, November’s increase was mainly driven by more positive consumer assessments of the present situation, particularly regarding the labour market. Compared to October, consumers were also substantially more optimistic about future job availability, which reached its highest level in almost three years. Meanwhile, consumers’ expectations about future business conditions were unchanged and they were slightly less positive about future income.

In the eurozone, markets are fully expecting a further 25 bps cut at December's meeting while also pricing in a 50% chance of a 50 bps cut. Eurozone inflation rose in October to 2.0%, up from 1.7% in September. Core inflation, excluding volatile items such as food, energy, alcohol, and tobacco, remained at 2.7% in October. Services inflation rose to 4.0% from September’s 3.9%. According to FactSet estimates, eurozone headline inflation in November, due to be reported on Friday, 29th November, ahead of the 12 December ECB meeting, is forecast to be 2.4% higher than November 2023 levels, while core inflation, is expected to stay stable at 2.9% year on year in November, in line with October’s reading. On the growth front, the eurozone Flash Composite PMI came in at 48.1, down from October’s 50.0 and a 10-month low. The Flash Eurozone Services PMI was also at a 10 month low, at 49.2, down from October’s 51.6, a 10-month low. The Flash Eurozone Manufacturing PMI was also lower, at 45.2 from October’s 46.0. The poor growth figures have fed concerns about the prospects for the eurozone and the euro. Markets are already worried about the collapse of Germany’s government and the early elections in February, the increasing chance of a collapse in the French government, and the threatened trade tariffs from the next Trump administration. It is also worrying that the French bond market may be on the brink as the premium investors demand to hold 10-year French government bonds over German bonds has reached the highest level since 2012. The potential fall of the current government could drive it higher.

In the UK inflation rose in October with the headline rate rising by 2.3% in the 12 months to October 2024, up from 1.7% in September. On a monthly basis, inflation rose by 0.6% in October 2024. Core CPI (excluding energy, food, alcohol and tobacco) rose by 3.3% in the 12 months to October 2024, up from 3.2% in September; the CPI goods annual rate rose from negative 1.4% to negative 0.3%, while the CPI services annual rate rose from 4.9% to 5.0%. The UK economy itself appears to be stagnating. The Flash Composite PMI fell into contractionary territory in November, falling to 49.9, down from October’s 51.8 and a 13-month low. The survey suggested that a loss of confidence was driven partly by the payroll tax increase on businesses announced in the 30 October budget. Firms’ expectations for activity in the year ahead were the most pessimistic since late 2022. The Flash Services PMI also dropped to 50.0, down from October’s 52.0 and also a 13-month low. The Flash Manufacturing PMI continued to fall and reached a 9-month low, hitting 48.6 and down from October’s 49.9. However, consumer confidence is actually increasing, with the GfK Consumer Confidence Index for November up by 3 points to -18, marking its first improvement in three months. This gain may be attributed to the BoE’s second rate cut earlier this month, bringing the interest rate to 4.75% in November, while wage growth continued to outpace inflation.

Global market indices

US:

S&P 500 +4.10% QTD and +25.76% YTD

Nasdaq 100 +4.30% QTD and +24.35% YTD

Dow Jones Industrial Average +5.98% QTD and +19.03% YTD

NYSE Composite +3.55% QTD and +19.92% YTD

The Equally Weighted version of the S&P 500 posted a +5.95% gain this month, its performance is +18.22% YTD, 7.54 percentage points lower than the benchmark.

The S&P 500 Consumer Discretionary sector is the top performer this month at +11.99% MTD, and +24.80% YTD, while Health Care underperformed at -0.13% MTD, and +7.48% YTD.

The S&P 500 concluded its longest winning streak in months, retreating from a record high as investors closed the final full trading session of a robust November for US equities.

On Wednesday, Wall Street's benchmark index finished 0.4% below its peak closing level from the previous day, marking its first decline in eight sessions. This concluded a seven-day winning streak, matching a similar run in September but falling short of the eight-session streak in mid-August. The Nasdaq Composite experienced a 0.6% decline, while the Russell 2000, focused on small-cap stocks, edged 0.1% higher.

With US markets closed for the Thanksgiving holiday today and operating for a half-day on Friday, concluding November's trading, technology groups were among the notable underperformers. Dell Technologies and HP both retreated more than 12% following the release of their Q3 results on Tuesday afternoon. Other technology companies, including Autodesk, Hewlett Packard Enterprise, CrowdStrike, and Oracle, experienced declines exceeding 4%.

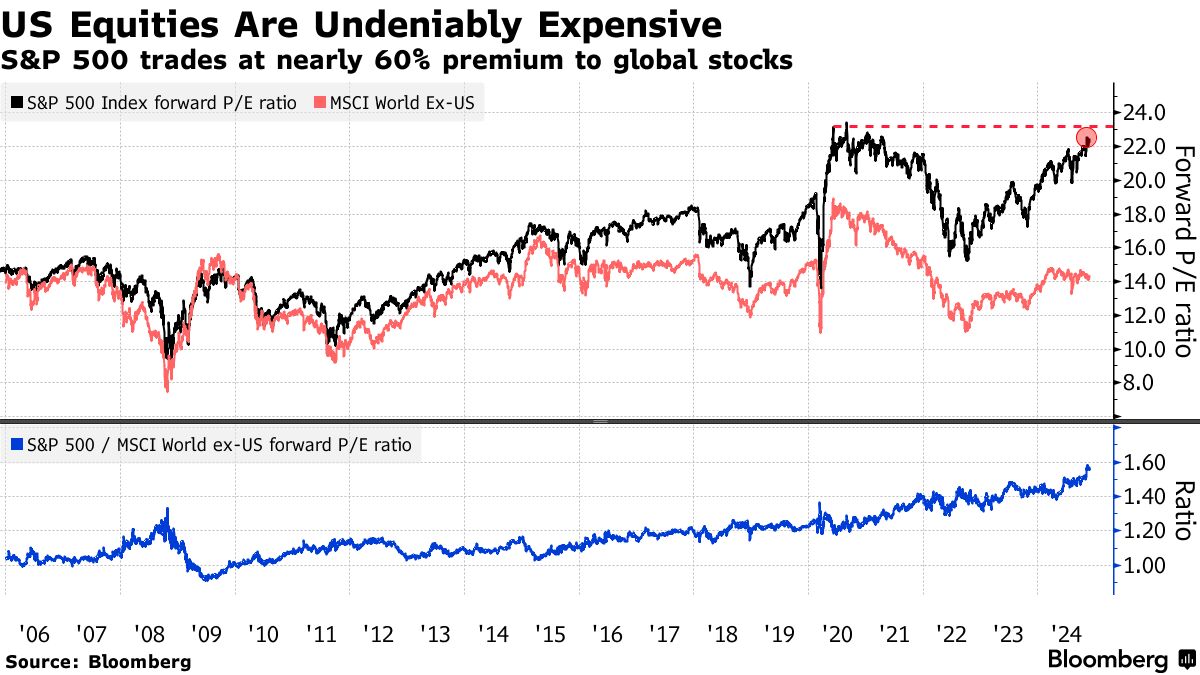

Fueled by technology stocks and the artificial intelligence boom, US stocks have continued to outperform international counterparts this year, supported by a resilient economy. The S&P 500 has surged over 25% in 2024, achieving multiple record highs and significantly outpacing the MSCI World Ex-USA Index. This has led to a widening valuation gap, with US stocks now trading at a record 60% premium to international peers based on forward P/E ratios.

Despite the stock market pausing after the S&P 500 reached its 52nd record high of the year, seasonal trends suggest this momentum may persist. LPL Financial data indicates that since 1950, the S&P 500 has averaged a 1.8% gain from Thanksgiving through year-end, finishing higher approximately 70% of the time. Furthermore, when the index shows year-to-date gains heading into the holiday, the average gain to year-end increases to 2.1%, with positive results occurring in 75% of instances.

In corporate news, and a significant development for ESG enthusiasts, BlackRock, Vanguard, and State Street face a lawsuit filed by a group of states led by Texas. The lawsuit alleges that these firms violated antitrust laws by inflating electricity prices through their investment practices, marking the most high-profile legal challenge against the sector to date.

Autodesk CEO Andrew Anagnost announced the company's focus on cost reduction within its sales and marketing departments. This strategic move follows pressure from activist investor Starboard Value.

Furthermore, the US Federal Trade Commission has initiated an investigation into Uber Technologies. The inquiry aims to determine whether the company's flagship subscription service has violated consumer protection laws.

Europe:

Stoxx 600 -3.43% QTD and +5.42% YTD

DAX -0.33% QTD and +14.98% YTD

CAC 40 -6.45% QTD and -5.30% YTD

FTSE 100 +0.46% QTD and +7.00% YTD

IBEX 35 -2.51% QTD and +14.62% YTD

FTSE MIB -3.03% QTD and +9.02% YTD

In Europe, the Equally Weighted version of the Stoxx 600 is up +0.27% in November, and its performance is +3.99% YTD, 1.43 percentage points below the benchmark.

The Stoxx 600 Financial Services is the leading sector this month, up +4.81% MTD +15.62% YTD, while Autos & Parts has exhibited the weakest performance at -5.26% MTD and -16.64% YTD.

Global:

MSCI World Index +1.81% QTD and +19.60% YTD

Hang Seng -7.17% QTD and +6.17% YTD

Mega cap stocks had a mostly positive performance in November with Alphabet -1.10%, Amazon +10.38%, Apple +3.99%, Meta Platforms +0.29%, Microsoft +4.09%, Nvidia +1.94%, and Tesla +33.24%.

Energy stocks experienced a positive performance this month, with the Energy sector +5.92% MTD and +12.74% YTD. Halliburton +14.92%, Baker Hughes Company +14.52%, Energy Fuels +13.67%, Phillips 66 +9.46%, Chevron +8.93%, Marathon Petroleum +6.80%, ExxonMobil +0.75%, and Occidental Petroleum +0.42%, while Shell -1.57%, ConocoPhillips -1.96%, and Apa Corp -4.58%.

Materials and Mining stocks had a slightly positive performance this month. The Materials sector is +0.95% MTD and +9.65% YTD. Gold is -3.59% MTD +28.00% YTD, while copper prices are -5.71% MTD. Albemarle +13.99%, Nucor Corporation +9.12%, while Freeport-McMoRan -2.80%, Mosaic -3.85%, Yara International -5.38%, Newmont Mining -7.48%, Sibanye Stillwater -9.67%, and Celanese Corporation -42.12%.

Commodities

Oil prices had a disappointing November with WTI -1.12% MTD and Brent -0.60% MTD. This was primarily driven by ongoing concerns of subdued Chinese demand and a contraction in the geopolitical risk premia due to de-escalating tensions in the Middle East following expectations and the announcement of a cease fire between Hezbollah and Israel.

Gold has rallied this year, +28.00% YTD. Gold prices experienced a moderate recovery on Wednesday, rebounding from an over one-week low recorded in the previous session. This upward movement was primarily driven by a weaker US dollar. However, the initial gains were somewhat tempered following the release of economic data indicating inflation remaining above the 2% target. This suggests that the Federal Reserve may exercise caution regarding further interest rate reductions.

Spot gold prices settled at $2,638.03 per ounce, reflecting a +0.21% increase. It is important to note that US markets will be closed on Thursday in observance of the Thanksgiving holiday. In the preceding trading session, gold prices had reached their lowest point since 18th November.

Oil prices remained relatively stable on Wednesday, despite a significant and unexpected increase in US gasoline inventories.

This stability followed a decline in both oil benchmarks on Tuesday, triggered by a ceasefire agreement between Israel and the Iranian-backed Hezbollah group in Lebanon. The agreement, brokered by the US and France, took effect on Wednesday.

However, oil prices found support amidst reports that OPEC+ is considering a further delay to the planned oil output increase scheduled for January.

OPEC+, responsible for approximately half of global oil production, had intended to gradually ease production cuts throughout 2024 and 2025. However, this plan has been cast into doubt due to weaker global demand and increased production from non-OPEC+ countries. A final decision on the matter is expected at the group's 5th December meeting.

Adding further complexity to the market dynamics, sources revealed to Reuters on Tuesday that crude oil would not be excluded from the 25% tariffs that the former US president has threatened to impose on all imports from Mexico and Canada. Oil industry analysts and traders have cautioned that this action could lead to higher oil prices for US refiners, ultimately squeezing profit margins and increasing fuel costs for consumers.

EIA reports surprise gasoline build, crude drawdown ahead of Thanksgiving holiday. US gasoline inventories unexpectedly increased last week leading into the Thanksgiving holiday, while crude oil stockpiles experienced a larger-than-anticipated decline. This decrease in crude oil inventories was driven by a significant drop in imports, with supplies from Mexico reaching a record low, according to the Energy Information Administration's (EIA) Wednesday report.

Gasoline stocks rose by 3.3 million barrels for the week ending 22nd November, reaching a total of 212.2 million barrels. This build in gasoline inventories is particularly noteworthy given the anticipated record travel volumes for Thanksgiving, which typically drives increased demand. The American Automobile Association (AAA) projections indicate record-breaking road travel, suggesting that gasoline demand should have been robust. However, gasoline supplied, a proxy for demand, only marginally increased to 8.51 million barrels per day (bpd) from 8.42 million bpd the previous week.

Conversely, crude oil inventories declined by 1.8 million barrels, bringing the total to 428.4 million barrels. This decline was primarily attributed to a reduction in net US crude imports, which fell by 1.9 million bpd to 1.4 million bpd. This decrease in imports was largely due to a 1.6 million bpd slump in imports to 6.1 million bpd, while exports rose by 285,000 bpd to 4.7 million bpd.

Several factors contributed to the decline in crude oil imports. Crude deliveries to the Gulf Coast registered their smallest week-on-week increase since July 2020. Imports from Mexico experienced a significant drop of 617,000 bpd, the largest decline since July 2020, reaching a record low of 151,000 bpd since data collection began in June 2010. This decline aligns with reports that Mexican state-run oil company Pemex's crude oil and condensate production decreased year-on-year in October, reaching its lowest point this year, while its local refineries processed a larger proportion of its output.

In addition to the import dynamics, crude stocks at the Cushing, Oklahoma, delivery hub decreased by 909,000 barrels. Refinery crude runs increased by 67,000 bpd, and refinery utilization rates rose by 0.3 percentage points to 90.5% of total capacity.

Finally, distillate stockpiles, which include diesel and heating oil, increased by 400,000 barrels to 114.7 million barrels, as reported by the EIA.

Currencies

The dollar continued to strengthen in November as yields rose on the strength of the US economy and expectations that the new Trump administration would impose tariffs that will result in higher inflation, leaving the Fed with no room to continue the rate cutting cycle. The dollar index has risen over the month; it is +1.99% MTD +4.64% YTD.

The GBP is -1.38% MTD and -0.55% YTD against the USD. The EUR is -2.63% MTD and -4.30% YTD against the USD.

The US dollar fell against other major currencies on Wednesday on thin pre-US holiday trading, with the US dollar index -0.91% to 106.40, its lowest since 13th November, a 1.9% decline from its two-year high reached last Friday.

This decline extended the unwinding of the dollar’s recent rally. Trading activity remained muted, with many market participants refraining from building or holding positions ahead of the extended Thanksgiving weekend, which coincides with the month-end. US markets will be closed on Thursday, with early closures on Friday.

Revised data confirmed that GDP grew at an annualised rate of 2.8% in Q3, in line with expectations and unchanged from the prior estimate. However, this data provided limited support for the Fed to justify another rate cut in December.

Similarly, consumer spending data offered little encouragement. Progress in reducing inflation appeared to have stalled, even as the economy maintained robust growth momentum in the early part of Q4. The Commerce Department reported that the personal consumption PCE index rose 0.2% in October, matching September’s gain. On an annual basis, the PCE price index increased by 2.3%, up from a 2.1% rise in September. Core inflation also remains above target at 2.8%.

The dollar's weakness boosted the euro, which rose +0.85% to $1.0571, marking its highest level in a week. It was -0.05% against Sterling to 0.8338 pence. Similarly, the British pound strengthened against the US dollar, gaining +0.91% to $1.2678.

The Japanese yen outperformed, buoyed by expectations of a potential December rate hike in Japan and end-of-month position adjustments. The dollar fell -1.33% against the yen, reaching a five-week low of ¥150.91.

Cryptocurrencies

Bitcoin +36.75% MTD and +129.14% YTD to $96,215.00.

Ethereum +46.30% MTD and +61.50% YTD to $3,683.60

Bitcoin came within $300 of the magical $100,000 mark this month, on 22nd November before dropping about $9,000 over the subsequent four days. The crypto market has surged about $1 Trillion overall following Donald Trump’s election which also saw a group of pro-crypto lawmakers being elected to Congress. Trump's team is currently discussing the possibility of creating a White House position dedicated to digital asset policy. This would be the first time such a role has been established in the US. During his campaign Trump vowed to make America “the Bitcoin superpower of the world” and create a “Bitcoin strategic reserve.” With the resignation of Securities and Exchange Commission chair Gary Gensler, long viewed as a nemesis to crypto supporters, and crypto supporters emerging as leading candidates to run the SEC and the Commodities Futures Trading Commission, sentiment has been rising among investors. They are betting that prices will continue to rise based on increasing governmental and institutional investor demand, particularly in the Spot Bitcoin ETF market. About $6.9 billion has poured into US Spot Bitcoin ETFs in the period following Trump’s election win, according to data compiled by Bloomberg. The 12 ETFs have total assets of roughly $100 billion.

Note: As of 6:00 pm EST 27 November 2024

Fixed Income

US 10-year yield +51.0 basis points QTD +38.3 basis points YTD to 4.264%.

German 10-year yield +2.9 basis points QTD +15.5 basis points YTD to 2.164%.

UK 10-year yield +31.8 basis points QTD +75.8 basis points YTD to 4.297%.

US Treasury 10-year bond yields are +38.3 basis points (bps) YTD and -2.6 bps over the past month.

The CME's FedWatch Tool gives a 70% probability of a 25 bps cut at the Fed’s December meeting. Swap traders are pricing in a total of about 16.2 bps worth of reductions for the remainder of the year.

The benchmark German 10-year yield is -22.6 bps in November at 2.164%, while the UK 10-year yield is -13.4 bps at 4.297%. The spread between US 10-year Treasuries and German Bunds increased by 20.0 bps from 190.0 bps at the end of October to 210.0 bps now.

Italian bond yields, a benchmark for the eurozone periphery, are -25.6 bps this month to 3.412%. Consequently, the spread between Italian and German 10-year yields increased by 1.5 bps to 124.8 bps from 123.3 bps in October.

US Treasury yields declined on Wednesday as investors sought the safety of government bonds amidst discouraging consumer sentiment surveys from Europe. Concerns about US inflation temporarily subsided as recently released economic data aligned with market expectations.

An updated estimate of US GDP growth for Q3 confirmed a 2.8% annualised rate, unchanged from the previous estimate. However, there was a slight downward revision to consumer spending. The Labor Department reported an increase in continuing unemployment claims to 1.9 million, indicating persistent challenges for those seeking new employment.

These developments contributed to a decline in Treasury yields across the maturity spectrum. The 10-year yield fell -3.7 bps to 4.264%, its lowest level since 1st November. The 2-year yield dropped over -4.0 bps to 4.21%, a more than two-week low. Longer-term, the 30-year yield reached 4.419%, its lowest point since 7th November.

Investor appetite for US debt remained strong, as evidenced by a successful auction of $44 billion in seven-year notes. The high yield of 4.183% was below the market rate at the bidding deadline, suggesting robust demand. This followed similarly successful auctions of two- and five-year notes earlier in the week.

European bond yields also retreated on Wednesday. Data released on Wednesday revealed a steeper-than-anticipated decline in German consumer sentiment and a five-month low in French consumer confidence. Germany's 10-year Bund yield fell -2.7 bps to 2.164%. Current market expectations indicate a 25 bps reduction in the ECB's key interest rate in December, with a 25% probability assigned to a larger 50 bps cut.

Italy's 10-year yield experienced a more significant decline of -4.7 bps to 3.412%, narrowing the spread between German and Italian 10-year yields by 2.0 bps to 124.8 basis points.

In the UK, gilt yields fell to their lowest levels since the 30th October budget announcement by finance minister Rachel Reeves, mirroring the downward trend in German Bunds. Five- and 10-year gilt yields each decreased by over -5.0 bps to 4.168% and 4.297%, respectively.

Financial markets currently assign a 19% probability to a quarter-point rate cut by the BoE at its upcoming 19th December meeting. Market pricing suggests expectations for three quarter-point rate cuts between now and the end of next year, largely unchanged from the previous day.

Note: Data as of 6:00 pm EST 27 November 2024

What to think about in December 2024

With the US election over, much of the focus for markets has been on whether President-elect Trump will really impose across the board tariffs with Canada, Mexico and China specifically targeted, or if these are only “negotiation tactics”. For China, the threat of tariffs, with a suggested 10% above the 60% already mentioned in his campaign, could have serious implications for the world’s second largest economy as it seeks to wrangle its economy out of deflation and weak domestic growth.

China's economic balancing act: domestic policy and global trade tensions in 2025. The Chinese economy faced substantial headwinds in 2024, prompting policymakers to initiate more aggressive easing measures in late September. However, the results of the US election signal potential further challenges arising from anticipated increases in US tariffs. Navigating these headwinds, while simultaneously stabilising domestic consumption and the property market as well as managing renewed US-China trade tensions, will be paramount for Chinese policymakers in 2025.

This easing cycle diverges from historical trends in China, where policy responses were often triggered by precipitous declines in exports and primarily focused on infrastructure and property construction. Current forecasts suggest relative stability in exports, continued contraction in property investment, and resilience in consumption, particularly in the goods sector. Growth in government consumption and investment is poised to accelerate as the resolution of local government debt alleviates financing pressures and facilitates fiscal expansion, which in turn, should boost domestic demand. Policymakers have left room to scale up or adjust the measures if needed.

Two primary factors contribute to China's subdued inflationary environment. Structural impediments, including the protracted housing market downturn and persistent industrial overcapacity, weigh on price levels. Furthermore, the restoration of consumer confidence and the revitalisation of labour markets and wage growth are likely to be gradual processes.

The range of potential economic outcomes for China in the coming year is considerable, given domestic policy uncertainties and elevated trade-related risks.

Although Chinese exporters may continue to expand their presence in emerging markets, the anticipated imposition of significantly higher US tariffs is likely to induce a marked deceleration in overall export growth. In 2023 Chinese exports to the US were, according to estimates from S&P Global, worth approximately $100 billion. Consequently, the contribution of exports to real GDP growth may contract materially. This presents Chinese policymakers with a critical juncture: implement a robust policy response to mitigate these challenges or accept a considerably lower trajectory for headline real GDP growth.

EUR/USD December seasonality offers brief respite amid bearish 2025 outlook. Despite a roughly 7% decline over the past two months, the EUR/USD exchange rate has recently rebounded from its 2023 lows, introducing nuance into the near-term outlook. Historical seasonal patterns suggest the potential for near-term strength in December, traditionally the euro's strongest month. Analysts also point to technically oversold conditions and the notion that recent negative economic data has already been priced into the currency.

However, underlying fundamentals paint a more bearish picture for the euro over the longer term. Major banks project further weakness against the US dollar into 2025, with several forecasting a move towards parity, according to Bloomberg. This bearish outlook is driven by diverging monetary policy expectations. Markets anticipate 150 bps of interest rate cuts from the ECB compared to 75 bps from the Fed by the end of 2025. Additionally, concerns persist about the potential for trade policies under a second Trump administration to disproportionately impact the export-dependent eurozone.

The anticipated policy mix under a potential Trump presidency, including tariffs and tax cuts, could fuel further appreciation of the US dollar. However, some analysts suggest that the greenback's recent gains may necessitate a period of consolidation before further advances.

Despite the prevailing bearish sentiment, analysts highlight the risk of renewed EUR/USD strength should the exchange rate rise above the April 2024 low point around 1.0600. This level is seen as a key technical threshold, and a break above it could trigger further upward momentum.

Key events in December 2024

The potential policy and geopolitical risks for investors that could negatively affect corporate earnings, stock market performance, currency valuations, sovereign and corporate bond markets and cryptocurrencies include:

1 December Legislative elections, Romania. The coalition government of the leftist Social Democrats (PSD) and the centre-right Liberals (PNL) will likely fall short of securing an outright majority in parliament in December. Therefore, a coalition with a third party will likely be necessary to form a majority government.

1 December South Africa G20 Presidency. South Africa takes over the G-20 presidency for a year from Brazil. South Africa’s President, Cyril Ramaphosa, has said that the country will use its G20 presidency to focus on advancing inclusive economic growth, food security and artificial intelligence.

5 December OPEC+ joint ministerial monitoring committee meeting (JMMC). OPEC+ members will discuss delaying the output increases that were due to begin in January. The group had aimed to gradually unwind production cuts in 2025, but weak Chinese demand and increasing supply from non-OPEC+ producers have kept prices lower than desired.

7-8 December Doha Forum, Qatar. The 2024 summit has the theme of “The Innovation Imperative.” The forum will focus on more open, collaborative, and cross-sectoral models of innovation.

12 December European Central Bank Monetary Policy Meeting. The ECB is widely expected to cut rates by another 25 bps at this meeting, with the odds of a 50 bps cut rising to over 50% due to concerns around euro area weakness. There appears to be intensifying debate about how the ECB should react to a deterioration in the eurozone economy as inflation may be approaching the 2% target more rapidly than previously foreseen. In addition, ECB policymakers have warned that US tariffs could have a detrimental effect on Europe, potentially sparking a recession and a period of deflation in the medium term. Although about 146 bps of cuts are forecast for 2025, policymakers are likely to take a gradual approach to avoid taking rates below the so-called neutral threshold.

17-18 December US Federal Reserve Monetary Policy Meeting. With the US economy continuing to grow at a good pace, the labour market remaining strong and consumer demand rising, the Fed will likely take a more gradualist approach to future rate cuts. However, much will depend on November’s NFP numbers, due on 6 December, in order to get a clearer picture of the actual situation in the labour market. Markets are largely pricing in a 25 bps cut at this meeting but future rate cuts, particularly given rising sovereign debt levels and the potential return of higher inflation if President-elect Trump does impose the suggested tariffs, may be limited.

19 December Bank of England Monetary Policy Meeting. The BoE is widely expected to cut rates again during this meeting by 25 bps but further rate cuts may be delayed given the expected increase in borrowing laid out by the Chancellor of the Exchequer during her presentation of the budget on 30 October.

19 December Bank of Japan Monetary Policy Meeting. The BoJ is increasingly expected to raise rates once again. Although BoJ Governor Ueda has repeatedly said that rate decisions will be made at each meeting and not in advance, there is political pressure on the BoJ not to raise rates as Prime Minister Shigeru Ishiba’s ruling coalition no longer enjoys a majority in parliament and will be depending on smaller parties for support for the new budget for next year which still has to be agreed. A rate hike next month may be perceived to hit businesses, households and government finances negatively and therefore may not be supported by those smaller parties.

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

本文提供給您僅供資訊參考之用,不應被視為認購或銷售此處提及任何投資或相關服務的優惠招攬或遊說。金融商品交易涉及重大損失風險,可能不適合所有投資者。過往績效不代表未來表現。

由專業人士建立。為專業人士打造。